TL;DR:

- Reducing SaaS payment processing costs involves managing payment method, data submission, routing, and pricing models. These factors significantly impact total costs, which often range from 5 to 9 percent of revenue when accounting for all expenses.

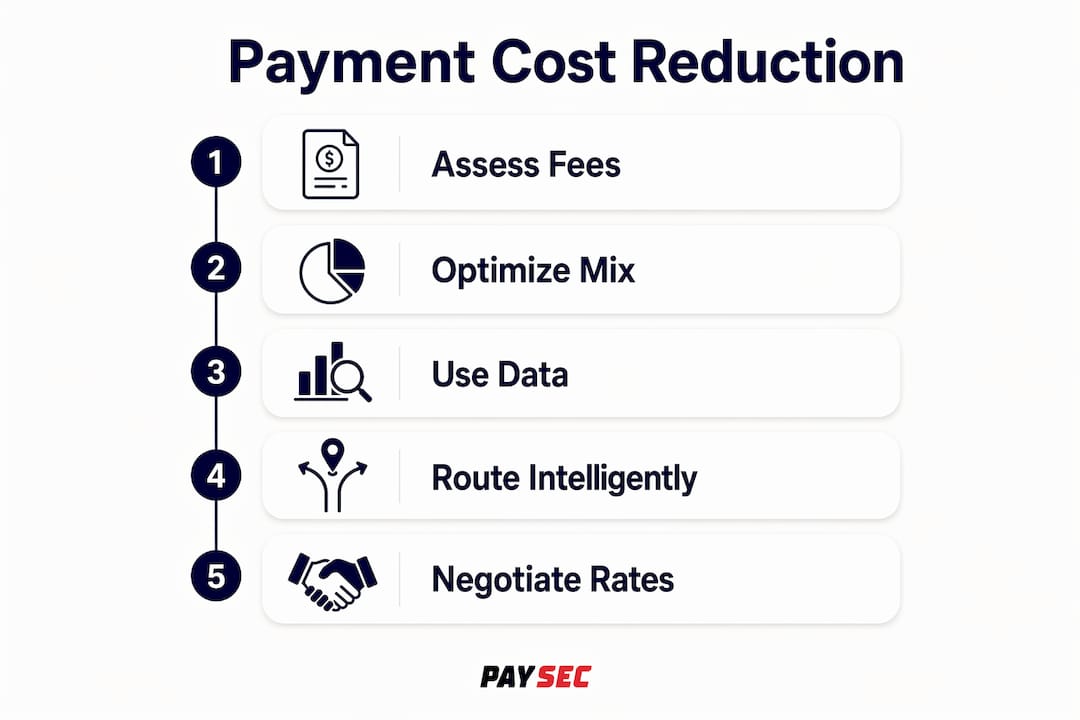

Reducing SaaS payment processing costs is defined as the systematic effort to lower the total fees a software business pays to accept, process, and settle customer payments. Standard credit card fees run 2.9% plus $0.30 per transaction, but the true payment cost for most SaaS companies lands between 5–9% of annual revenue once engineering, PCI compliance, and billing maintenance are factored in. That gap between the headline rate and the real cost is where most businesses lose money without realizing it. The strategies in this guide cover payment method mix, interchange qualification, intelligent routing, and pricing model negotiation. Each one is a concrete lever you can pull to cut payment processing expenses and protect your margins.

What are the primary contributors to SaaS payment processing costs?

Payment processing costs in SaaS extend far beyond the percentage your gateway charges per transaction. The total cost of ownership includes engineering hours spent maintaining integrations, annual PCI DSS compliance audits, fraud tooling, billing infrastructure, and the opportunity cost of developer time diverted from product work. When you add those up, a company paying 2.9% at the gateway level is often paying 5–9% of revenue in real terms.

Most finance teams track only the visible line item on their payment processor invoice. That means cost leakages from interchange downgrades, failed payment retries, and suboptimal routing go undetected for months or years. A proper payment cost analysis for SaaS starts with a full accounting of every dollar spent on the payment stack, not just the processing fee.

The three main cost buckets to audit are:

- Processing fees. These include the interchange fee (set by card networks like Visa and Mastercard), the assessment fee, and the processor markup. The markup is the only component you can negotiate directly.

- Compliance and infrastructure costs. PCI DSS Level 1 certification, fraud detection tools, tokenization services, and gateway hosting all carry real price tags that rarely appear on a single invoice.

- Engineering and operational costs. Developer time spent building, maintaining, and debugging payment integrations is a direct cost. So is the time your finance team spends reconciling payment data manually.

Vendor pricing models compound the problem. Flat-rate pricing (one blended rate for all card types) is simple but expensive. Tiered pricing groups transactions into "qualified," "mid-qualified," and "non-qualified" buckets, which processors define in their favor. Interchange-plus pricing passes the actual interchange cost through to you with a fixed markup on top. Interchange-plus is almost always the lower-cost model for merchants who actively manage their transaction mix. The catch is that you need good data to benefit from it.

Pro Tip: Pull your last 90 days of transaction data and categorize fees by type: interchange, assessment, processor markup, and non-processing costs. Most finance teams find that non-processing costs account for 30–40% of total payment spend once they run this exercise.

How can optimizing your payment method mix cut payment processing expenses?

The payment method your customer uses determines the interchange rate you pay. Credit cards, especially rewards cards and corporate cards, carry the highest interchange rates. ACH transfers and SEPA Direct Debit carry flat fees that are often a fraction of a percent of the transaction value. Shifting 10–15% of payment volume from credit cards to ACH or SEPA can save SaaS businesses thousands of dollars annually.

This is not a passive outcome. You have to design your billing experience to make lower-cost methods attractive to customers. The following steps produce measurable results:

- Default new customers to ACH or bank transfer during onboarding. Most customers accept the default. Offering ACH as the primary option with credit card as a secondary choice shifts volume without friction.

- Offer a small incentive for bank transfer payments. A modest discount for ACH payment is often cheaper than the credit card fee you would have paid. The math works in your favor at any meaningful transaction size.

- Segment your customer base by transaction value. High-value enterprise contracts paid monthly are ideal ACH candidates. Low-value monthly subscriptions may not justify the switch, since ACH has its own failure and return rates to manage.

- Communicate the option clearly at renewal. Many customers who would willingly pay by bank transfer simply never see the option. A single email at renewal time can shift a meaningful percentage of your base.

- Monitor payment method mix monthly. Track the percentage of volume processed on each rail and set a target. Treat it as a product metric, not a finance afterthought.

The payment method mix is a product variable, not a fixed condition. SaaS companies that treat it as a managed lever consistently report lower net processing costs than those that accept whatever method customers choose by default.

Pro Tip: For annual contracts, ACH is almost always the right default. The flat fee on a $10,000 annual payment via ACH is negligible compared to the 2.9% you would pay on a credit card for the same amount.

What role does enhanced transaction data play in cutting interchange fees for SaaS?

Enhanced transaction data submission is the practice of including additional fields, such as customer reference numbers, line-item detail, and tax amounts, when submitting a transaction for authorization. Visa calls its standard Visa CEDP Product 3. Mastercard calls its equivalent Level 3 data. Both programs qualify B2B and government transactions for lower interchange tiers. Many payment gateways do not submit this data automatically, which means merchants pay standard consumer interchange rates on transactions that should qualify for lower commercial rates.

The financial impact is direct. A transaction that downgrades from a commercial Level 3 rate to a standard consumer rate can cost significantly more in interchange. Across thousands of monthly transactions, that difference compounds into a material annual expense.

What you need to do to capture these savings:

- Audit your current data submission. Ask your payment processor or gateway which Level 2 and Level 3 fields you are currently submitting. Many platforms submit Level 2 (tax amount, customer code) but not Level 3 (line-item detail, unit of measure, commodity codes).

- Map your invoice data to interchange fields. Your billing system likely already captures the data required. The work is connecting it to your payment submission flow.

- Automate the submission. Manual data entry at transaction time is not viable at scale. Build the enrichment into your billing pipeline so every eligible transaction goes out with full data.

- Verify qualification rates post-implementation. Your processor can provide a report showing what percentage of transactions qualified for Level 2 or Level 3 rates. Track this monthly.

The table below shows how interchange qualification tiers affect cost at scale:

| Data level | Typical use case | Interchange rate impact |

|---|---|---|

| Level 1 (basic) | Consumer card transactions | Standard rate applies |

| Level 2 (enhanced) | B2B, tax-exempt purchases | Moderate rate reduction |

| Level 3 (full detail) | Government, large B2B | Largest rate reduction |

For SaaS companies selling to businesses or government entities, interchange fee optimization through Level 3 data submission is one of the highest-return technical investments available. The engineering effort is modest. The savings are recurring.

How does intelligent routing and retry logic reduce payment costs?

Intelligent routing is the practice of directing each transaction to the payment processor or rail most likely to approve it at the lowest net cost. A naive routing setup sends every transaction to a single processor regardless of card type, geography, or historical approval rates. A well-designed routing layer uses structured transaction-level data, including card BIN, issuing country, authorization response codes, and fee outcomes, to make smarter decisions in real time.

The key insight is that routing decisions should balance approval probability against net cost per capture. Choosing the cheapest rail that has a low approval rate costs more in the long run because failed payments generate their own costs: customer service contacts, involuntary churn, and re-billing overhead.

Common pitfalls to avoid when building routing logic:

- Routing only on price. A processor with a lower markup but a 5% lower approval rate on international cards will cost you more in lost revenue than the markup savings justify.

- Ignoring retry sequencing. When a payment fails, the retry attempt should go to a different processor or rail, not the same one that just declined it. Smart retry logic per payment rail recovers substantially more failed payments than generic retry schedules.

- Treating all declines the same. A soft decline (insufficient funds) has a different optimal retry timing than a hard decline (card reported lost). Build retry logic that reads the response code and acts accordingly.

- Skipping data enrichment. Routing decisions are only as good as the data feeding them. Without card type, BIN, and issuing country at the transaction level, your routing logic is guessing.

- Failing to measure net cost per capture. Track the total cost of a successful payment, including retries, not just the fee on the first attempt. This is the metric that actually reflects routing performance.

For SaaS subscription businesses, dunning systems built per payment rail recover significantly more revenue than generic retry schedules. A customer on ACH who fails due to insufficient funds needs a different retry window than a credit card that expired. Treating them identically leaves recoverable revenue on the table.

What pricing model changes and negotiation tactics lower SaaS payment fees?

The most direct way to decrease SaaS fees is to switch from flat-rate or tiered pricing to interchange-plus. Switching to interchange-plus pricing often requires no major technical rework when done through an embedded payment partner. The commercial model changes while your core payment flows stay intact. The benefit is immediate visibility into what you actually pay at the interchange level, which makes further optimization possible.

Negotiation leverage comes from demonstrating control over your payment volume. Processors compete for volume. If you can credibly show that you can shift transaction volume between rails or processors, your negotiating position improves without you having to switch vendors. Dynamic routing capability is the clearest signal to a processor that you are a sophisticated buyer who will act on pricing differences.

The question of building in-house payment facilitation (becoming a PayFac) comes up frequently in these conversations. The honest answer is that in-house PayFac infrastructure is rarely cost-effective for SaaS companies processing under £50M annually. The fixed costs of licensing, compliance, and infrastructure outweigh the margin gains at most volume levels. The better path for most companies is working with an established payment partner that offers wholesale interchange rates and transparent pricing.

Pro Tip: Before any pricing negotiation, pull a 12-month transaction report broken down by card type, BIN range, and interchange category. Walk into the negotiation with specific numbers. Processors respond to data, not general requests for better rates.

The comparison below summarizes the trade-offs between common pricing models:

| Pricing model | Best for | Key trade-off |

|---|---|---|

| Flat-rate | Early-stage, low volume | Simple but expensive at scale |

| Tiered | Processors, not merchants | Opaque; categories favor the processor |

| Interchange-plus | Growth-stage and above | Requires data literacy to benefit fully |

| Wholesale interchange | High-volume, optimized stack | Lowest cost; needs a capable partner |

For SaaS businesses ready to move beyond flat-rate pricing, the SaaS payment stack breakdown is a useful reference for understanding which components to prioritize when renegotiating or restructuring your payment infrastructure.

Key Takeaways

Reducing SaaS payment processing costs requires treating payment method mix, interchange qualification, routing logic, and pricing model as managed variables, not fixed conditions.

| Point | Details |

|---|---|

| True cost exceeds headline fees | Total payment cost runs 5–9% of revenue when compliance, engineering, and infrastructure are included. |

| Payment method mix is a lever | Shifting 10–15% of volume to ACH or bank transfer produces measurable annual savings. |

| Level 3 data submission reduces interchange | Submitting Visa CEDP Product 3 or Mastercard Level 3 data qualifies B2B transactions for lower rates. |

| Routing must balance cost and approval rate | Optimizing for price alone without tracking approval rates increases total cost per captured payment. |

| Interchange-plus pricing outperforms flat-rate | Merchants who understand their transaction mix consistently pay less under interchange-plus models. |

Why payment cost should be a product metric, not a finance afterthought

The most common mistake I see SaaS finance teams make is treating payment processing as a vendor relationship problem. They assume the rate is fixed, the processor is a utility, and the only lever is occasional renegotiation. That framing leaves the majority of available savings untouched.

Payment cost is a product variable. The method mix, the data submitted with each transaction, the routing logic, the retry sequencing: all of these are decisions that your product and engineering teams make, often without realizing they have financial consequences. When finance and engineering sit in separate rooms and never compare notes on payment outcomes, you get a system that is technically functional but financially inefficient.

The companies I have seen achieve the most meaningful payment cost reduction share one trait. They assign someone, whether a product manager, a payments lead, or a finance engineer, to own payment performance as a metric. That person tracks approval rates, interchange qualification rates, payment method mix, and net cost per capture on a monthly basis. They treat a drop in Level 3 qualification the same way a growth team treats a drop in conversion rate: as a problem to diagnose and fix.

The other myth worth disputing is that cost reduction requires a complete infrastructure overhaul. In most cases, the highest-return changes are commercial and configurational, not architectural. Switching pricing models, enriching transaction data, and adjusting retry logic are changes that can be implemented incrementally. You do not need to rebuild your payment stack to see real savings. You need visibility, a clear owner, and the willingness to treat payment cost as something you manage rather than something that happens to you.

— PaySec Marketing Team

How Paysec helps SaaS businesses lower processing costs

Paysec's Network Offset Pricing gives SaaS businesses access to wholesale interchange rates with no hidden fees, no minimums, and no long-term contracts. Clients across the SaaS sector have used Paysec's pricing model to save 30–60% on processing, with one SaaS marketplace achieving a 42% reduction in processing costs after switching. Paysec also provides detailed transaction reporting that makes payment cost analysis straightforward for finance teams.

If you are ready to move beyond flat-rate pricing and start managing payment costs as a real business variable, Paysec's wholesale interchange pricing is built for exactly that. Transparent rates, real data, and measurable results from day one.

FAQ

What is payment cost analysis in SaaS?

Payment cost analysis in SaaS is the process of auditing all fees associated with accepting payments, including interchange, processor markup, compliance, and engineering costs, to identify where money is being lost and where savings are achievable.

How much can a SaaS business realistically save on payment processing?

Savings depend on current pricing model and transaction mix, but businesses that switch to interchange-plus pricing, submit Level 3 data, and shift volume to lower-cost rails commonly reduce net processing costs by 30–60%.

What is the difference between flat-rate and interchange-plus pricing?

Flat-rate pricing charges one blended rate for all transactions regardless of card type. Interchange-plus passes the actual interchange cost through with a fixed markup, which is almost always cheaper for businesses with a managed transaction mix.

When does building in-house payment facilitation make financial sense?

In-house PayFac infrastructure is generally not cost-effective for SaaS companies processing under £50M annually. The licensing, compliance, and operational costs outweigh the margin gains at most volume levels.

How does ACH reduce payment processing costs compared to credit cards?

ACH transfers carry flat fees rather than percentage-based charges, making them significantly cheaper than credit cards for high-value transactions. Shifting even 10–15% of subscription volume to ACH produces measurable annual savings for most SaaS businesses.