TL;DR:

- SaaS platforms pay effective processing rates between 4.5% and 7% due to layers of hidden fees beyond the advertised rate. These additional costs, including international surcharges, platform fees, and chargebacks, grow exponentially as revenue and transaction complexity increase. Managing transaction-level data and optimizing billing structures can significantly reduce these excessive processing costs.

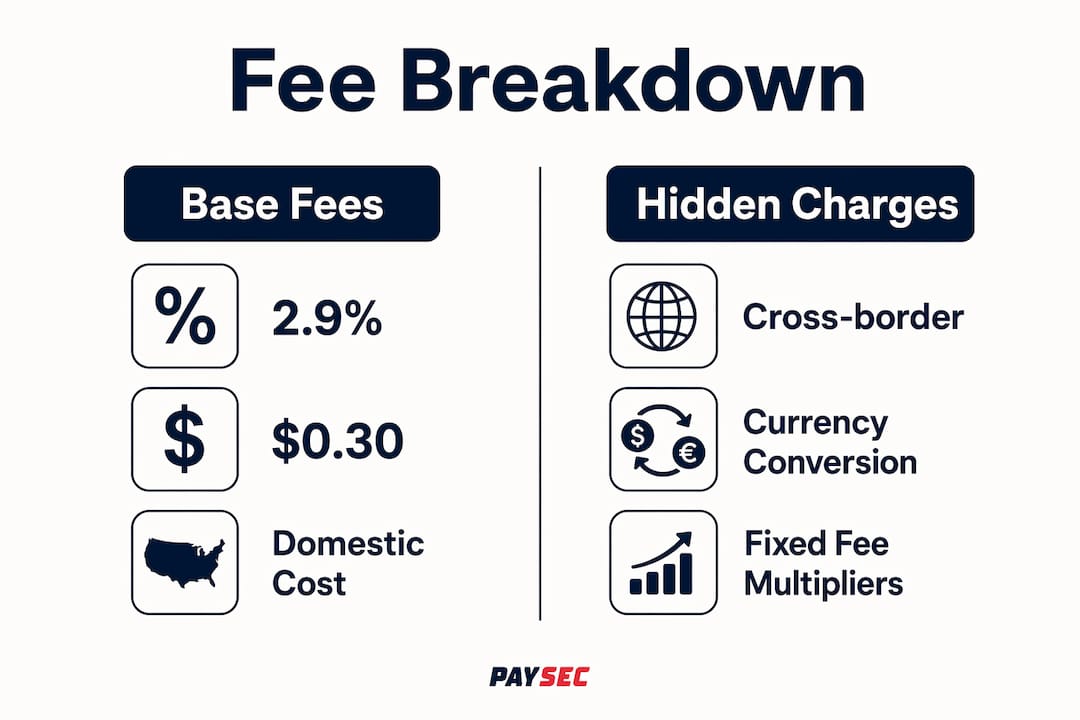

SaaS platforms pay excess processing fees because the true effective rate for global transactions runs between 4.5% and 7%, far above the advertised 2.9% + $0.30 that most operators budget against. That gap is not a rounding error. At $50,000 in monthly recurring revenue, the difference between the headline rate and the actual effective rate translates to $17,400 to $28,050 in annual hidden costs. Understanding why SaaS processing fees exceed advertised rates requires looking at every layer of the payment stack, from base interchange to billing platform add-ons, international surcharges, and the compounding math that punishes growth.

Why SaaS platforms pay excess processing fees: the full fee breakdown

The advertised 2.9% + $0.30 rate is the floor, not the ceiling. SaaS platforms with global customers routinely pay 4%–7% effective rates once all fee layers are counted. Each layer compounds on the one below it.

Base processing fees vs. effective rates

The base card processing fee covers interchange, the card network assessment, and the processor's margin. For domestic consumer cards, that math stays close to the advertised rate. The moment a customer pays with a corporate card, a rewards card, or a card issued outside the United States, the interchange category shifts upward. Corporate cards carry higher interchange by design. Rewards cards pass their cashback costs to the merchant. International cards trigger a separate surcharge on top of everything else.

The hidden charges that compound costs

The following fee categories are the primary drivers of excess costs in SaaS payment stacks:

- International card surcharges: Stripe and most processors add 1.5% for international cards on top of the base rate. Currency conversion adds another 1% on top of that. Combined, international surcharges add 1.5% or more to every cross-border transaction.

- Billing platform fees: Stripe Billing charges an additional 0.5%–0.8% of revenue for subscription management. Stripe Tax adds another layer for automated tax calculation. Stripe Connect, used by SaaS marketplaces, adds 0.25%–0.5% per transaction on top of base processing.

- Chargeback fees: Recurring chargebacks cost $15 each. At scale, even a 0.5% dispute rate generates thousands of dollars in chargeback fees annually.

- Fixed per-transaction fees: The $0.30 fixed fee is a flat charge regardless of transaction size. On a $5 add-on charge, that fixed fee alone represents 6% of the transaction value before the percentage rate is applied.

| Fee Type | Typical Rate | Impact at Scale |

|---|---|---|

| Base processing | 2.9% + $0.30 | Baseline cost for domestic consumer cards |

| International card surcharge | +1.5% | Applied to every non-U.S. card transaction |

| Currency conversion | +1.0% | Applied when currency differs from settlement currency |

| Stripe Billing add-on | +0.5%–0.8% | Applied to all subscription revenue managed through Billing |

| Stripe Tax | +0.5% | Applied to transactions using automated tax features |

| Chargeback fee | $15 flat | Charged per disputed transaction regardless of outcome |

Pro Tip: Pull a 90-day transaction report and segment by card type. Most SaaS finance teams discover that 20%–35% of their volume runs on international or corporate cards, which explains the gap between the quoted rate and the actual effective rate.

The compounding effect is the key insight here. A SaaS platform using Stripe Billing, serving international customers, and processing a mix of corporate and consumer cards can easily reach a 6%–7% effective rate before chargebacks are counted. That is not a billing error. It is the designed structure of the payment stack.

How do SaaS pricing models drive fee escalation?

SaaS pricing models create a fee problem that pure e-commerce platforms rarely face. The reason is billing event frequency. A traditional retailer processes one transaction per sale. A SaaS platform with hybrid pricing processes multiple billing events per customer per month.

Per-seat and usage-based billing multiply fixed fees

Consider a SaaS platform charging a $50 base subscription, a $10 per-seat fee for five users, and a $5 usage overage. That single customer generates three separate billing events in one month. Each event carries the $0.30 fixed fee. The total fixed fee burden for that customer is $0.90 per month, or $10.80 per year, before the percentage rate is applied. Hybrid pricing triggers multiple billing events, each with its own fixed fee, causing unexpected fee escalations that compound across a growing customer base.

The math gets worse as average transaction value falls. A $5 add-on transaction carries a much higher effective fee percentage than a $500 annual subscription. Low-value transactions disproportionately increase fee percentage because the $0.30 fixed fee represents a larger share of a smaller charge.

Why processing fees scale with SaaS growth

- Revenue growth increases transaction count. More customers mean more billing events. Each billing event carries fixed fees. Total fixed fee costs grow in direct proportion to customer count, not just revenue.

- Expansion revenue triggers additional charges. Upgrades, seat additions, and plan changes each generate a new billing event. A customer who upgrades mid-cycle creates two charges in one month.

- International expansion shifts the card mix. As SaaS platforms grow globally, the share of international and corporate cards in their transaction mix increases. Each shift upward in card category increases the effective rate.

- Processor markups compound on higher interchange. Payment processors apply their markup as a percentage of the base interchange cost. When interchange rises, the processor's margin in absolute dollars also rises. The markup is not a flat dollar amount. It is a multiplier.

- Fee growth outpaces revenue growth. One documented case study shows that a 50% revenue increase led to a 124% increase in processing fees. That is not an outlier. It is the predictable result of compounding markups on a growing, increasingly international customer base.

Pro Tip: Model your fee exposure at 2x and 3x current revenue before you hit those milestones. Most SaaS operators discover the fee problem after it has already become material. Running the projection early gives you time to renegotiate or restructure billing before growth locks in the cost.

The core issue is that SaaS financial models typically project revenue growth linearly while payment fees grow exponentially. That mismatch is the reason so many SaaS operators describe payment costs as a surprise at Series B and beyond.

In-house payments vs. outsourcing: what does each actually cost?

The total cost of ownership question is where SaaS payment strategy gets genuinely complex. Many operators look at a 5%–6% effective processing rate and assume building in-house infrastructure would be cheaper. The math rarely supports that conclusion below a specific volume threshold.

| Cost Category | In-House Infrastructure | Outsourced to PSP |

|---|---|---|

| Engineering headcount | 2–4 full-time engineers | Included in processor fees |

| PCI DSS compliance | $50,000–$200,000 annually | Handled by processor |

| Tax calculation and remittance | Dedicated tax engineering or software | Available as add-on (0.5%) |

| Payment stack maintenance | Ongoing sprint allocation | Included in processor fees |

| Total cost as % of revenue | 5%–9% | 3%–7% effective rate |

In-house payment infrastructure costs 5%–9% of revenue when engineering, PCI compliance, and tax management are counted together. That figure converges across multiple analyses of SaaS payment operations. The break-even point where in-house infrastructure becomes cost-effective sits at approximately £50 million in annual processing volume. Below that threshold, the fixed costs of compliance and engineering exceed the savings from lower per-transaction rates.

Outsourcing to a specialized payment service provider eliminates the need for multiple full-time engineers dedicated to payment infrastructure. PayFac models at scale save £1–3 million annually compared to maintaining equivalent in-house capability. The more important consideration is opportunity cost. Engineering time spent on PCI compliance and payment stack maintenance is engineering time not spent on product features that drive revenue.

The right frame for this decision is not "what is the per-transaction rate?" It is "what is the total cost of processing payments as a percentage of revenue, including all labor, compliance, and technology costs?" Viewing payment fees as total cost of ownership rather than headline transaction rates changes the analysis entirely for most SaaS operators.

For platforms operating across borders, the complexity multiplies further. Cross-border payment infrastructure adds currency settlement, local acquiring relationships, and regulatory compliance layers that each carry their own cost. Most SaaS platforms underestimate these costs until they are already operating in five or more international markets.

How can SaaS platforms reduce transaction costs?

Reducing excess fees in SaaS requires a combination of structural changes to billing, active negotiation, and analytics-driven identification of overcharged transactions. None of these strategies require switching processors. Most can be implemented within an existing payment stack.

Consolidate invoices to cut fixed fee exposure

Invoice consolidation reduces the number of fixed fees charged and directly lowers effective processing costs. Instead of billing a customer three times in a month for base subscription, seat additions, and usage overages, consolidate all charges into a single monthly invoice. The percentage fee stays the same. The fixed fee drops from $0.90 to $0.30. At 1,000 customers, that consolidation saves $7,200 per year before any other changes.

Negotiate based on volume and transaction mix

Stripe's volume discounts are relationship-dependent with no published public pricing tiers below the standard rate. Most SaaS operators do not know they can negotiate. The negotiation leverage comes from two sources: total processing volume and transaction mix stability. Processors prefer predictable, low-risk transaction mixes. A SaaS platform that can demonstrate consistent average transaction values, low chargeback rates, and growing volume has real negotiating power. Use it.

Optimize payment methods for large invoices

ACH bank transfers carry processing fees of 0.8% with a cap of $5.00. For annual subscription invoices above $1,000, ACH saves significantly compared to card processing at 2.9% plus surcharges. Offering ACH as the default payment method for annual plans, with card as an option, shifts the highest-value transactions to the lowest-cost payment rail.

Use analytics to identify misclassified transactions

Some transactions are misclassified at the interchange level, resulting in higher fees than the transaction actually warrants. Detailed transaction reporting for finance teams can surface these misclassifications. Correcting them requires submitting transaction data with the right level 2 or level 3 detail, which qualifies corporate card transactions for lower interchange categories.

Pro Tip: For B2B SaaS platforms billing other businesses, submitting level 2 and level 3 transaction data (purchase order numbers, item descriptions, tax amounts) can qualify corporate card transactions for interchange rates 0.5%–1.0% lower than the default corporate card rate. Most processors support this. Almost no SaaS platforms use it.

Consider alternative payment infrastructure

For SaaS platforms processing above $1 million in annual volume, exploring payment processing features built specifically for subscription billing can reduce costs materially. Wholesale interchange pricing models pass the actual interchange cost through to the merchant with a flat service fee on top, eliminating the processor's percentage markup entirely. That structure is fundamentally different from the standard bundled pricing model and can reduce effective rates by 30%–60% for platforms with the right transaction mix.

Key takeaways

SaaS platforms pay excess processing fees because effective rates compound across multiple hidden fee layers, and those layers scale faster than revenue as platforms grow internationally and add billing complexity.

| Point | Details |

|---|---|

| Effective rates exceed advertised rates | Global SaaS platforms pay 4.5%–7% effective rates, not the advertised 2.9% + $0.30. |

| Hidden fees compound at every layer | International surcharges, billing platform fees, and chargebacks each add to the base rate. |

| Hybrid pricing multiplies fixed fee exposure | Multiple billing events per customer increase fixed fee costs disproportionately as volume grows. |

| Total cost of ownership reframes the decision | In-house payment infrastructure costs 5%–9% of revenue; outsourcing often costs less below £50M volume. |

| Consolidation and negotiation reduce costs | Invoice consolidation, ACH for large invoices, and active rate negotiation each lower effective fees. |

The fee problem most SaaS founders discover too late

The pattern we see repeatedly is this: a SaaS founder builds a financial model at seed stage using the advertised 2.9% + $0.30 rate, raises a Series A, and then discovers at Series B that payment costs are consuming 5%–6% of revenue. By that point, the pricing model is set, the billing architecture is built, and renegotiating the payment stack requires engineering resources that are already allocated elsewhere.

The uncomfortable truth is that payment fees are almost never treated as a strategic cost center until they become a problem. Most SaaS operators treat payments as infrastructure, like cloud hosting, something you set up and forget. The difference is that cloud costs scale predictably with usage. Payment costs scale with usage, card mix, geography, billing complexity, and processor markup compounding. Those variables interact in ways that are genuinely hard to model without transaction-level data.

What I have found working with SaaS platforms across multiple growth stages is that the operators who manage fees well share one habit: they review transaction-level fee data monthly, not quarterly. They know their effective rate by card type, by geography, and by billing event type. That granularity is what makes negotiation possible and what makes consolidation decisions obvious.

The other misconception worth addressing is that switching processors solves the problem. It rarely does. The fee structure is largely determined by interchange categories set by Visa and Mastercard, not by the processor. What the processor controls is the markup on top of interchange and the structure of add-on fees. Negotiating that markup, optimizing the transaction mix, and choosing the right billing architecture matter far more than which processor logo appears on your dashboard.

Expect fee complexity to increase through 2026 and beyond. International expansion, new billing models like consumption-based pricing, and the growth of B2B SaaS with corporate card-heavy customer bases all push effective rates higher. The platforms that build fee management into their financial operations now will have a structural cost advantage over those that address it reactively.

— PaySec Marketing Team

Cut your SaaS processing costs with Paysec

SaaS platforms that have mapped their full fee structure consistently find that the gap between their advertised rate and their actual effective rate is larger than expected. Paysec's Network Offset Pricing passes wholesale interchange rates directly to SaaS operators with a flat service fee, eliminating the percentage markup that drives most of the excess cost. The result is a transparent, predictable fee structure with no minimums and no long-term contracts.

One SaaS marketplace working with Paysec achieved a 42% reduction in processing costs by moving to wholesale interchange pricing and optimizing its transaction mix. Paysec serves SaaS platforms across 18+ industries with detailed transaction reporting that surfaces the exact fee categories driving your effective rate. If your payment costs are growing faster than your revenue, the SaaS payment solutions at Paysec are built to fix that.

FAQ

What is the true effective processing rate for SaaS platforms?

The true effective processing rate for global SaaS platforms runs between 4.5% and 7%, well above the advertised 2.9% + $0.30. Hidden charges including international surcharges, billing platform fees, and chargeback costs drive the gap.

Why do processing fees grow faster than SaaS revenue?

Processing fees grow faster than revenue because processor markups are applied as a percentage of interchange, causing compound growth as interchange increases. One documented case shows a 50% revenue increase producing a 124% increase in processing fees.

How does hybrid pricing increase SaaS processing costs?

Hybrid pricing creates multiple billing events per customer per month, each carrying the $0.30 fixed fee. A customer billed for a base subscription, seat additions, and usage overages in one month generates three fixed fees instead of one.

Can SaaS platforms negotiate lower processing rates?

SaaS platforms can negotiate lower rates, but Stripe and most processors do not publish volume discount tiers. Negotiation leverage comes from total processing volume, low chargeback rates, and a stable, predictable transaction mix.

What is the cheapest payment method for large SaaS invoices?

ACH bank transfer is the lowest-cost payment method for large invoices, carrying a fee of 0.8% capped at $5.00. For annual subscription invoices above $1,000, ACH saves significantly compared to card processing rates with international surcharges applied.