TL;DR:

- Offering multiple payment options significantly boosts ecommerce conversion rates and reduces cart abandonment. Providing 4 to 6 relevant payment methods tailored to customer demographics can increase revenue by up to 12%, with broader options further improving performance. Strategically managing payment infrastructure, including multi-provider setups and ongoing analysis, creates resilience and maximizes growth opportunities.

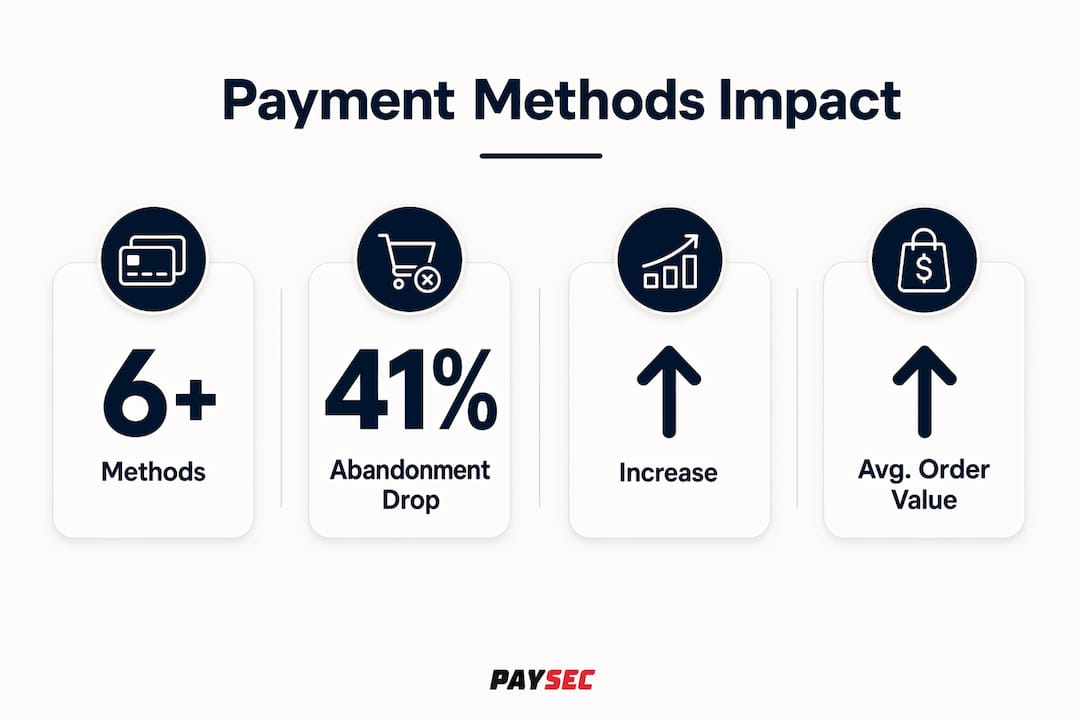

Offering multiple payment options is the single most effective checkout change an ecommerce store can make to increase revenue and reduce lost sales. Stores with six or more payment methods see conversion rates of 4.8% versus 2.9% for single-method checkouts. That gap represents real money left on the table every day. Payment diversity, the industry term for strategically offering multiple payment methods across your checkout, is no longer optional. It is a direct driver of growth, and the data behind why ecommerce needs multiple payment options has never been clearer.

Why multiple payment options cut cart abandonment

Cart abandonment is the most expensive problem in ecommerce, and payment friction is a leading cause. When shoppers reach checkout and do not see a payment method they trust, they leave. The fix is straightforward: give them options.

Stores offering six or more payment methods reduce cart abandonment by 41% compared to stores with a single option. That reduction translates directly into completed orders and higher monthly revenue. The mechanism is simple: every additional relevant payment method removes a reason to abandon.

The numbers become even sharper when you look at specific method combinations. Cart abandonment drops from 68% to 27% when BNPL, digital wallets, and crypto are added alongside traditional credit cards. That is a 41-percentage-point swing driven entirely by payment choice. Shoppers who might have left because they lacked a credit card, or preferred not to use one, now have a path to complete the purchase.

The financial impact compounds further through average order value. BNPL and digital wallets increase average order value by letting customers afford higher-ticket items they would otherwise skip. A customer who sees a $300 item as unaffordable on a credit card may complete that purchase through a BNPL option like Affirm or Klarna. That is not a small behavioral shift. It is a structural change in what your store can sell.

Pro Tip: Do not add every available payment method to your checkout. Focus on the 4–6 methods most relevant to your customer base. Irrelevant options add visual clutter without improving conversion.

How payment diversity affects revenue directly

The revenue math behind payment diversity is concrete. Adding one relevant extra payment method increases merchant revenue by 12% on average. Broader mix expansion can boost conversion rates by up to 30%. These are not marginal gains. For a store generating $500,000 annually, a 12% revenue lift from a single payment addition equals $60,000 in incremental sales.

| Payment Setup | Avg. Conversion Rate | Cart Abandonment Rate | Revenue Impact |

|---|---|---|---|

| Single method (cards only) | 2.9% | 68% | Baseline |

| 3–5 methods | ~3.8% | ~45% | Moderate lift |

| 6+ methods (cards, wallets, BNPL, crypto) | 4.8% | 27% | Up to +30% conversion |

| One added relevant method | Varies | Varies | +12% avg. revenue |

The table above shows that each step toward broader payment coverage produces measurable gains. The jump from single-method to six-plus methods nearly doubles conversion rate while cutting abandonment by more than half.

How do customer demographics shape payment preferences?

Payment preferences are not uniform. They split sharply by generation, and stores that ignore this leave money on the table with specific customer segments.

73% of Gen Z prefer Buy Now, Pay Later as their primary checkout method. Gen Z shoppers are entering their peak spending years, and BNPL providers like Affirm, Afterpay, and Klarna are their preferred tools. A store without BNPL is effectively invisible to a large share of this demographic at the moment of purchase.

Millennials favor digital wallets. PayPal, Apple Pay, and Google Pay dominate this group's checkout behavior. Millennials value speed and security, and digital wallets deliver both. They have already stored their payment credentials and want a one-tap checkout experience. Forcing them to enter a 16-digit card number is friction they will not tolerate when a competitor offers Apple Pay.

Gen X remains loyal to traditional credit and debit cards. This group trusts Visa, Mastercard, and American Express. They are also the highest-spending demographic in many product categories, so ignoring their preference for card-based checkout is a costly mistake.

Payment methods by demographic segment

Matching your payment mix to your customer base requires knowing who shops with you. Here is a breakdown of prominent payment methods by demographic:

- Gen Z (ages 18–27): Affirm, Afterpay, Klarna (BNPL); Cash App Pay; cryptocurrency options like Bitcoin

- Millennials (ages 28–43): PayPal, Apple Pay, Google Pay; Venmo for peer-influenced purchases; BNPL as secondary

- Gen X (ages 44–59): Visa, Mastercard, American Express credit cards; debit cards; PayPal as a trusted secondary

- Baby Boomers (ages 60+): Traditional credit and debit cards; PayPal; bank transfers for high-value purchases

The importance of payment diversity becomes concrete when you map these preferences against your own customer analytics. If your store's audience skews toward Gen Z and Millennials, a checkout without BNPL and digital wallets is structurally misaligned with your buyers. Reviewing your customer demographics in Google Analytics or Shopify Analytics and cross-referencing with this breakdown takes under an hour and can reshape your entire payment strategy.

Single vs. multi-provider: what is the smarter setup?

Most ecommerce stores start with a single payment service provider, or PSP. Stripe, Square, and Braintree are common first choices. That setup works at low volume. It becomes a liability as your store grows.

A single PSP creates a single point of failure. A provider outage can halt 100% of transactions until the issue is resolved. For a store processing $10,000 per day, even a two-hour outage costs roughly $833 in lost sales, and that assumes customers return rather than buying from a competitor. Multi-provider setups eliminate this risk by routing transactions to a backup PSP automatically when the primary goes down.

The strategic case for multiple PSPs goes beyond reliability. A multi-PSP strategy with payment orchestration intelligently routes transactions to optimize approval rates, system resilience, and cost. Different PSPs have different approval rates for different card types and geographies. Routing a transaction from a European customer through a PSP with strong European bank relationships improves the chance of approval. That is not a theoretical benefit. It is a measurable lift in completed transactions.

Pro Tip: Use a payment orchestration layer like Gr4vy or Spreedly to manage multiple PSPs from a single integration. This gives you routing control, fallback logic, and consolidated reporting without rebuilding your checkout for each new provider.

Single provider vs. multi-provider: a framework comparison

| Factor | Single PSP | Multi-PSP with Orchestration |

|---|---|---|

| Outage risk | High (100% transaction loss) | Low (automatic failover) |

| Approval rate optimization | Limited | High (geo and card-type routing) |

| Cost negotiation leverage | Weak | Strong (providers compete for volume) |

| Payment method coverage | Narrow | Broad |

| Integration complexity | Simple | Managed by orchestration layer |

| Vendor lock-in | High | Low |

The orchestration layer is the key enabler here. It sits between your checkout and your PSPs, making routing decisions in real time. Implementing a multi-PSP strategy requires this layer to route transactions based on card issuer preference, cost, and regional reliability. Without it, managing multiple PSPs manually creates operational overhead that cancels out the benefits.

Avoiding vendor lock-in also has a direct cost benefit. When a single PSP knows you have no alternative, your negotiating position on processing fees is weak. With two or more PSPs active, you can shift volume toward the provider offering better rates. That competition keeps your processing costs in check over time.

How do you choose the right payment mix for your store?

The goal is not to offer every payment method available. The goal is to offer the right ones for your specific customers. These are different objectives, and confusing them leads to cluttered checkouts that reduce conversion rather than improve it.

High-converting stores focus on 4–6 core payment methods aligned with their customer base rather than overwhelming shoppers with every available option. Too many choices create decision fatigue at the moment when you need the customer to act. The strategic selection of payment methods is where the real work happens.

Here is a practical framework for building your payment mix:

- Audit your current checkout data. Pull your checkout abandonment reports and identify at what step customers leave. If abandonment spikes at the payment selection screen, that is a direct signal that your current options are misaligned.

- Map your customer demographics. Use your analytics platform to identify the age distribution and geographic location of your buyers. Cross-reference with the demographic payment preferences outlined above.

- Identify your top three customer segments. Build your core payment mix around those three groups first. For most U.S. ecommerce stores, this means credit and debit cards, PayPal, and one BNPL provider.

- Add one new method and measure. Adding one relevant extra payment method increases revenue by 12% on average. Add a single new method, run it for 30 days, and measure its impact on conversion rate and average order value before adding another.

- Run A/B tests on checkout layout. The order in which payment options appear affects selection rates. Test whether placing Apple Pay or PayPal at the top of your checkout improves completion rates for mobile shoppers.

- Review quarterly. Consumer payment behaviors shift. BNPL adoption grew sharply between 2022 and 2026. Cryptocurrency acceptance is expanding. Set a calendar reminder to review your payment mix every quarter against current customer data.

The benefits of diverse payment methods compound over time when you treat this as an ongoing process rather than a one-time setup. Stores that review and adapt their payment mix quarterly consistently outperform those that set it once and forget it.

Victoria Cleland of the Bank of England has noted that payment choice is foundational for a well-functioning, inclusive payments system, strengthening resilience and enabling innovation. That principle applies directly to ecommerce. A store with a single payment method is not just less convenient. It is structurally fragile.

You can learn more about how the full ecommerce payment stack fits together, from gateway integrations to security layers, before finalizing your payment architecture decisions.

Key takeaways

Ecommerce stores that offer 4–6 strategically chosen payment methods consistently outperform single-method checkouts on conversion rate, cart abandonment, and average order value.

| Point | Details |

|---|---|

| Six-plus methods cut abandonment | Stores with 6+ payment options reduce cart abandonment by 41% and reach 4.8% conversion rates. |

| Demographics drive payment choice | 73% of Gen Z prefer BNPL; Millennials favor digital wallets; Gen X stays loyal to traditional cards. |

| Multi-PSP setups prevent revenue loss | A single PSP outage can halt 100% of transactions; multi-provider routing eliminates that risk. |

| One added method lifts revenue 12% | Adding a single relevant payment method increases merchant revenue by 12% on average. |

| Strategic selection beats volume | Offering 4–6 targeted methods outperforms cluttered checkouts with every available option. |

Payments are your front line, not your back office

By PaySec Marketing Team

Most ecommerce operators treat payments as infrastructure. You set it up once, it runs in the background, and you focus on marketing and product. That framing is costing you money.

Payments are the last thing a customer interacts with before handing you money. If that moment creates friction, confusion, or a missing option, the entire purchase funnel collapses at the finish line. Every dollar you spent on ads, email, and SEO to get that customer to checkout disappears. That is not a back-office problem. It is a front-line revenue problem.

What we have seen consistently is that merchants who treat payment strategy as a growth lever, not a compliance checkbox, outperform their competitors in ways that compound over time. Mismatched payment options cause brand damage and customer churn. A shopper who abandons your checkout because you do not offer Apple Pay does not just lose you one sale. They form an impression of your store as outdated or inconvenient, and they may not return.

The counter-intuitive insight here is that payment diversity is also a loyalty driver. When a customer completes a purchase using their preferred method, the experience feels frictionless. That feeling attaches to your brand, not to the payment provider. You get the credit for a smooth checkout even though the payment infrastructure did the work.

The forward-looking stores we work with are already thinking about payment resilience, not just payment coverage. That means multi-PSP architectures, orchestration layers, and quarterly payment mix reviews. It means treating the ecommerce payment processing layer as a strategic asset that requires active management. The stores that build this discipline now will have a structural advantage as consumer payment behaviors continue to shift.

— PaySec Marketing Team

See how Paysec supports your payment strategy

Paysec is built for ecommerce merchants who want to offer flexible payment options without watching processing fees eat into their margins. Its Network Offset Pricing model lets you pass processing costs to customers transparently, so you retain full revenue on every transaction.

Merchants across 18-plus industries use Paysec to manage diverse payment methods with no hidden fees, no minimums, and no long-term contracts. The result is measurable. Clients report 30–60% reductions in processing costs, with some seeing a 42% drop in fees after switching. If you are ready to support more payment methods while keeping more of what you earn, explore Paysec's pricing model or review merchant services tailored to ecommerce operators.

FAQ

How many payment methods should an ecommerce store offer?

High-converting stores offer 4–6 core payment methods aligned with their customer demographics. More than six options can create decision fatigue at checkout without meaningfully improving conversion.

Does adding BNPL really increase average order value?

Yes. BNPL options like Affirm, Afterpay, and Klarna let customers afford higher-ticket items by spreading payments, which directly increases average order value and order completion rates.

What happens if your payment provider goes down?

A single PSP outage can halt 100% of your transactions until the issue is resolved. A multi-PSP setup with automatic failover routing prevents total transaction loss during outages.

Which payment methods do gen z shoppers prefer?

73% of Gen Z shoppers prefer Buy Now, Pay Later as their primary checkout method. Stores without BNPL options are structurally misaligned with this growing demographic.

How do i know which payment methods my customers want?

Pull your checkout abandonment data and cross-reference it with your customer age and location demographics in Google Analytics or Shopify Analytics. Then map those demographics against known generational payment preferences to identify the gaps in your current checkout.