TL;DR:

- An ecommerce payment stack comprises interconnected technologies like processors, gateways, fraud tools, security, and reporting that manage online transactions and influence revenue. Proper configuration and ongoing optimization of each layer enhance authorization rates, customer experience, and compliance while reducing costs. Selecting the right providers and implementing payment orchestration now supports scalable growth and operational resilience as businesses evolve.

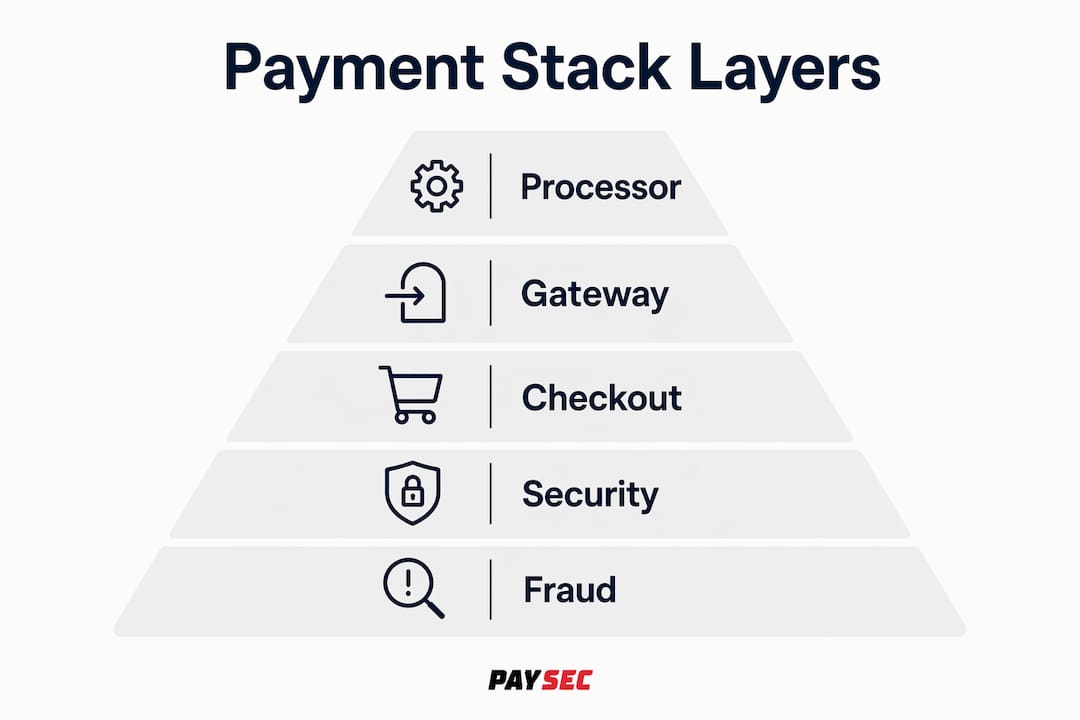

An ecommerce payment stack is the integrated system of technologies and services that processes, secures, and manages every online transaction your business accepts. It covers far more than a single payment gateway. The full stack includes a payment processor, checkout flow, fraud management tools, security and compliance controls, and reporting infrastructure. Providers like Stripe, PayPal, and Adyen have popularized all-in-one approaches, but most growing businesses eventually need to understand each layer independently. Getting this architecture right directly affects authorization rates, customer experience, and your total cost of accepting payments.

What is an ecommerce payment stack and why does it matter?

An ecommerce payment stack is defined as the complete set of integrated components that enable a merchant to accept, process, secure, and reconcile online payments. The term is not a formal industry standard. Payment professionals typically refer to this as your "payment infrastructure" or "payment architecture," but the stack framing is useful because it forces you to think in layers rather than treating payment acceptance as a single tool.

Payment stacks include the payment processor, gateway, checkout experience, security and compliance controls, fraud management, and reporting as distinct but interconnected elements. Each layer has a specific job, and a failure in any one of them affects the entire transaction lifecycle. A misconfigured fraud filter, for example, can reject legitimate customers just as reliably as it blocks bad actors.

The business case for understanding your stack is financial. Authorization rates, chargeback ratios, and processing fees are all directly influenced by how well your stack components work together. Merchants who treat payment infrastructure as a commodity rather than a strategic asset consistently leave revenue on the table through declined transactions and excessive fees.

What are the core components of a payment stack?

Payment processors transmit transaction data between the merchant, the issuing bank, and the acquiring bank to execute credit and debit card transactions. Think of the processor as the back-office engine. It communicates with card networks like Visa and Mastercard, requests authorization from the cardholder's bank, and confirms the result back to the merchant.

A payment gateway encrypts and transmits customer payment data securely, functioning as the digital equivalent of a point-of-sale terminal. The gateway sits between your checkout page and the processor, handling the secure handoff of sensitive card data. Without it, raw card numbers would travel unprotected across your servers, which is both a security risk and a compliance violation.

The remaining components of a payment stack each address a distinct operational need:

- Checkout flow. The customer-facing interface where payment method selection happens. Checkout implementations can be hosted on-site, off-site redirect, or hybrid, with each option presenting different trade-offs between design control and PCI DSS scope. An on-site checkout gives you full branding control but increases your compliance burden. A redirect to a hosted page reduces PCI scope but hands the customer experience to a third party.

- Security and compliance. PCI DSS certification, tokenization, and HTTPS encryption form the baseline. Tokenization replaces sensitive card data with a non-sensitive token, so your systems never store a real card number.

- Fraud management. Tools like 3D Secure (3DS) authentication add a verification layer that decreases fraudulent transaction risk without requiring manual review of every order. Machine learning models score transactions in real time based on behavioral signals, device fingerprints, and historical patterns.

- Reporting and analytics. Transaction monitoring, reconciliation dashboards, and decline reason codes give finance teams the data needed to identify problems and optimize performance. Without this layer, you are flying blind on authorization rates and chargeback trends.

Understanding how each component fits into the payment lifecycle lets you diagnose problems precisely. A high decline rate is not a "payment problem." It is either a processor routing issue, a fraud filter misconfiguration, or a card network rule conflict. Knowing which layer to investigate saves hours of troubleshooting.

How does payment orchestration improve authorization rates and scalability?

Payment orchestration is middleware that connects a merchant to multiple payment service providers (PSPs) through a single API, then optimizes how transactions are routed across those providers. It sits above your individual processors and gateways, acting as an intelligent traffic controller for your payment flow. As merchants scale globally, managing separate integrations with Stripe, Adyen, and regional acquirers becomes operationally unsustainable. Orchestration solves that by unifying them behind one abstraction layer.

The practical benefits of orchestration break down into four areas:

- Smart dynamic routing. Dynamic routing improves approval rates by up to 12% by directing each transaction to the acquirer most likely to approve it based on geography, card type, and historical performance data. A UK-issued Visa card processed through a UK acquirer will consistently outperform the same card routed through a US acquirer. Orchestration makes that decision automatically, in milliseconds.

- Failover resilience. When a PSP experiences downtime, orchestration automatically reroutes transactions to a backup provider. Without failover, a processor outage means lost sales. With it, the customer sees nothing unusual.

- Vault portability. Orchestration platforms maintain a centralized token vault, so a customer's stored payment method works across every connected PSP. This protects subscription revenue and repeat-purchase conversion when you switch or add providers.

- Unified reconciliation. Global scaling introduces varied provider APIs and settlement timing across currencies and regions. Orchestration consolidates multi-provider reporting into a single data stream, cutting reconciliation time significantly for finance teams managing cross-border operations.

Pro Tip: Before investing in a full orchestration platform, audit your current authorization rate by card type and geography. If you see approval rates below 85% in specific markets, that is the clearest signal that routing optimization will deliver measurable ROI.

Orchestration is not a tool for every merchant at every stage. Early-stage businesses with a single market and one PSP gain little from it. The value compounds as transaction volume grows, markets diversify, and the cost of a single provider's downtime or suboptimal routing becomes material.

What security and compliance practices protect your payment stack?

PCI DSS (Payment Card Industry Data Security Standard) compliance is the non-negotiable baseline for any business that accepts card payments online. The standard defines 12 requirements covering network security, access controls, encryption, and monitoring. Your compliance burden, measured by the Self-Assessment Questionnaire (SAQ) level you qualify for, depends directly on how your stack handles card data.

Keeping cardholder data off merchant servers through hosted pages or tokenization significantly reduces PCI audit scope and compliance costs. A merchant using a hosted payment page or an iframe-embedded payment field from a PCI-certified provider qualifies for SAQ A, the simplest self-assessment. A merchant who processes card data through their own servers faces SAQ D, which involves hundreds of controls and typically requires a Qualified Security Assessor.

Practical steps to reduce your PCI scope and strengthen your payment stack security:

- Use hosted payment fields or iframes. These embed the payment form directly from your provider's PCI-certified environment. Card data never touches your server.

- Implement tokenization. Tokenization and hosted payment fields avoid passing PAN and CVV through merchant servers, dramatically lowering compliance burden. Tokens are useless to attackers even if your database is compromised.

- Enforce HTTPS across your entire site. Not just the checkout page. Search engines and browsers flag mixed-content pages, and any unencrypted page in the customer journey creates a potential interception point.

- Deploy a Web Application Firewall (WAF). A WAF filters malicious traffic before it reaches your application layer, blocking SQL injection, cross-site scripting, and credential-stuffing attacks that target payment flows.

- Maintain secure logging and monitoring. PCI DSS requires audit logs of all access to cardholder data environments. Automated alerting on anomalous access patterns catches breaches before they escalate.

- Work with PCI-certified providers. When your gateway, processor, and fraud tools are all PCI Level 1 certified, their compliance posture extends to your integration. Verify certifications annually, not just at onboarding.

Pro Tip: Ask every payment vendor for their current Attestation of Compliance (AOC) document before signing a contract. A vendor who cannot produce one quickly is a compliance risk, regardless of how polished their sales presentation is.

The redirect versus embedded checkout decision deserves specific attention. Redirect checkouts, where the customer leaves your site to complete payment on the provider's page, offer the lowest PCI scope but the highest friction. Embedded checkouts keep the customer on your site and improve conversion, but require careful implementation to maintain scope reduction. The right choice depends on your conversion data and your team's technical capacity to implement embedding correctly.

How do popular ecommerce payment providers compare?

Leading providers like Stripe, PayPal, and Adyen offer combined gateway and processor services with fraud tools and checkout technology built in. Each targets a different merchant profile, and selecting the wrong one for your business size or transaction mix creates unnecessary cost and integration complexity.

The table below summarizes key differences across the most widely used providers:

| Provider | Best for | Payment methods | Global coverage | Pricing model |

|---|---|---|---|---|

| Stripe | Developer-led teams, SaaS, marketplaces | Cards, wallets, bank transfers, BNPL | 46+ countries | Per-transaction flat rate |

| PayPal | Consumer trust, SMBs, marketplaces | PayPal balance, cards, Venmo, BNPL | 200+ countries | Per-transaction flat rate |

| Adyen | Enterprise, omnichannel, high volume | 250+ payment methods | 40+ currencies | Interchange-plus |

| BigCommerce integrations | Mid-market ecommerce on BigCommerce platform | Varies by connected PSP | Varies by PSP | Varies by PSP |

Stripe's developer-first design makes it the default choice for technical teams building custom checkout experiences. Its documentation, API design, and ecosystem of third-party integrations are the strongest in the market. PayPal's primary advantage is consumer recognition. Displaying the PayPal button at checkout measurably increases conversion for merchants selling to consumers who trust the PayPal brand more than an unfamiliar checkout form.

Adyen targets enterprise merchants who need a single provider for card-present and card-not-present transactions across multiple geographies. Its interchange-plus pricing model rewards high-volume merchants with lower effective rates than flat-rate competitors. The trade-off is a more complex onboarding process and a minimum volume requirement that makes it unsuitable for early-stage businesses.

Pricing comparisons between providers require looking beyond the headline transaction fee. Monthly fees, chargeback fees, currency conversion markups, and the cost of add-on fraud tools all affect total cost of ownership. A provider with a lower per-transaction rate but a 1.5% currency conversion markup can cost more than a higher-rate provider with no conversion fee for a merchant with significant international volume. Reviewing your ecommerce processing fee structure against actual transaction data is the only reliable way to compare providers accurately.

Pro Tip: Request a fee analysis from any provider you are evaluating. Give them three months of actual transaction data and ask them to calculate what you would have paid on their pricing. Any provider unwilling to do this exercise is not confident in their own pricing.

When evaluating providers, also assess their merchant services capabilities beyond the gateway. Dedicated merchant accounts, chargeback support, and dispute management processes vary significantly and affect your operational workload after a provider is live.

Key takeaways

A well-designed ecommerce payment stack requires the right combination of processor, gateway, fraud tools, compliance architecture, and reporting to protect revenue and support growth.

| Point | Details |

|---|---|

| Stack has six core layers | Processor, gateway, checkout, security, fraud management, and reporting each serve a distinct function. |

| Orchestration lifts authorization rates | Dynamic routing improves approval rates by up to 12%, with the greatest gains in cross-border transactions. |

| PCI scope is controllable | Hosted payment fields and tokenization reduce compliance burden to SAQ A, the simplest audit level. |

| Provider selection is context-dependent | Stripe, PayPal, and Adyen each serve different merchant profiles; total cost of ownership matters more than headline rates. |

| Reporting is not optional | Transaction monitoring and decline reason codes are the only way to diagnose and fix authorization problems systematically. |

What we have learned building payment infrastructure for merchants

The most common mistake we see from ecommerce businesses is treating the payment stack as a one-time setup decision rather than an ongoing operational discipline. A stack that works well at $500,000 in annual revenue often breaks down at $5 million, not because the technology fails, but because the merchant never revisited routing logic, fraud thresholds, or provider mix as their transaction profile changed.

The second pattern worth naming is tool sprawl. Merchants add a fraud tool here, a currency conversion service there, and a subscription billing layer on top, without mapping how these tools interact. Overlapping fraud filters are a particularly costly version of this problem. Two independent fraud tools scoring the same transaction can produce conflicting signals, and the conservative one wins, blocking legitimate orders. Payment stack design must be tailored to a merchant's specific needs, and integration complexity from overlapping tools is one of the most underestimated operational risks.

On the compliance side, the instinct to minimize PCI scope by using hosted pages is correct, but it needs to be paired with ongoing monitoring. Merchants who achieve SAQ A certification and then stop thinking about compliance are the ones who get caught when a third-party script injected into their site starts capturing keystrokes on the checkout page. PCI scope reduction is not a permanent state. It requires continuous verification.

The businesses that get payment infrastructure right share one habit: they review authorization rate data by card type, geography, and payment method every month. That single practice surfaces more optimization opportunities than any technology investment. If your current provider cannot give you that breakdown, that is itself a signal worth acting on.

— PaySec Marketing Team

See how Paysec reduces your payment processing costs

Paysec's Network Offset Pricing eliminates traditional processing fees by passing wholesale interchange rates directly to merchants, with no hidden fees, no minimums, and no long-term contracts. Merchants across ecommerce, SaaS, healthcare, and CBD retail report processing cost reductions of 30 to 60%, with one client achieving a 42% reduction in processing costs. Paysec also provides detailed transaction reporting and compliance support, giving your finance team the visibility needed to manage your payment stack effectively. If you are ready to stop overpaying on every transaction, explore Paysec's solutions and see what your business could save.

FAQ

What is an ecommerce payment stack?

An ecommerce payment stack is the integrated set of technologies and services that processes, secures, and manages online payments for a merchant. It includes the payment processor, gateway, checkout flow, fraud management, security controls, and reporting tools working together across every transaction.

How does a payment gateway differ from a payment processor?

A payment gateway encrypts and transmits card data from the checkout to the processor, while the payment processor communicates with card networks and banks to authorize and settle the transaction. The gateway handles data security; the processor handles the financial transaction itself.

What is payment orchestration in ecommerce?

Payment orchestration is middleware that connects a merchant to multiple PSPs through a single API and routes transactions to the provider most likely to approve them. It delivers failover resilience, vault portability, and unified reporting across all connected providers.

How can ecommerce businesses reduce PCI DSS compliance burden?

Using hosted payment fields, iframe embeds, or tokenization SDKs keeps raw card data off merchant servers, qualifying most businesses for SAQ A, the lowest-complexity PCI self-assessment. Working with a PCI Level 1 certified provider extends their compliance posture to your integration.

Which payment provider is best for ecommerce businesses?

The right provider depends on your transaction volume, geographic markets, and technical resources. Stripe suits developer-led teams, PayPal adds consumer trust for SMBs, and Adyen serves high-volume enterprise merchants needing omnichannel coverage. Evaluating total cost of ownership across your actual transaction mix is the most reliable selection method.