TL;DR:

- CBD retailers face payment processing challenges due to industry classification as high-risk, leading to frequent account terminations by mainstream providers. Specialized high-risk processors offer more stable options with transparent pricing, dedicated accounts, and support for alternative payment methods like crypto and ACH transfers. Maintaining multiple active payment relationships and optimizing chargeback management are essential strategies for ensuring business stability in this high-risk industry.

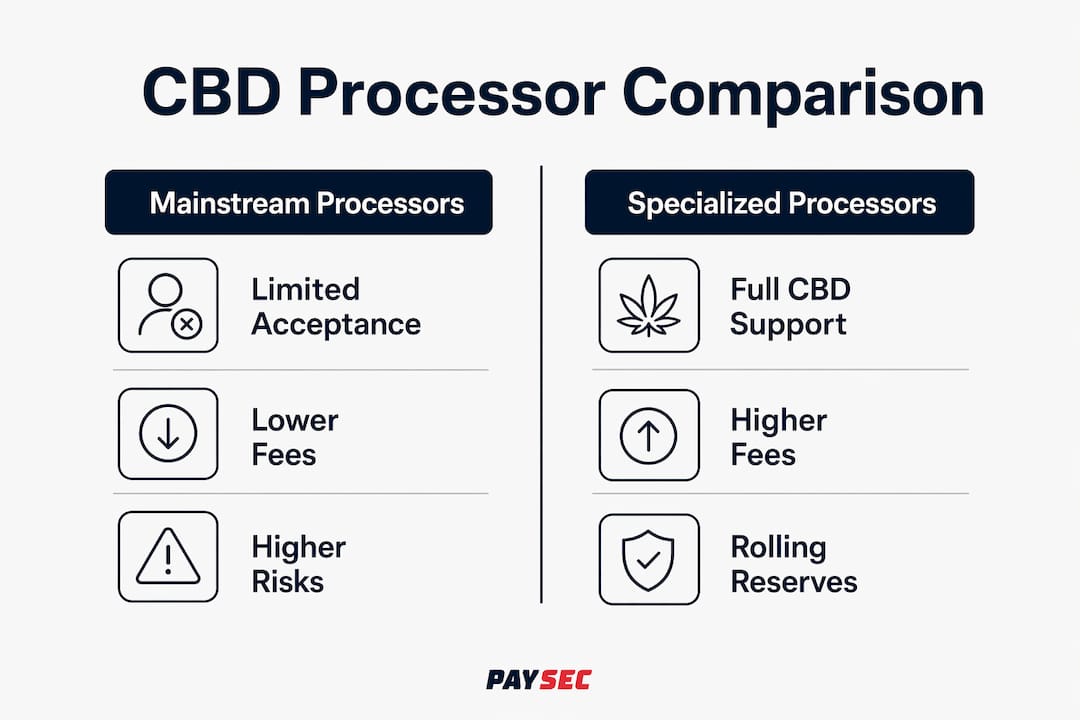

CBD businesses require payment processing alternatives because mainstream processors classify the industry as high-risk and routinely terminate accounts without warning. Stripe, PayPal, and Square explicitly prohibit CBD products in their terms of service, leaving retailers with no fallback when their accounts go dark. The consequences are severe: 67% of hemp businesses report significant payment processing challenges, and 43% have faced account termination despite full compliance. Understanding why cbd needs payment processing alternatives is not optional for CBD retailers. It is the foundation of a stable, revenue-generating business.

Why traditional payment processors restrict CBD merchants

The core reason mainstream processors refuse CBD merchants comes down to three compounding factors: regulatory uncertainty, elevated chargeback rates, and automated risk classification systems that treat CBD like cannabis.

The FDA has not approved CBD as a food additive or dietary supplement, which creates a legal gray zone that processors find unacceptable. Visa and Mastercard maintain their own merchant category codes, and CBD products fall into categories that trigger automatic flags in underwriting systems. These automated risk systems systematically flag CBD businesses due to regulatory overlaps, regardless of whether a specific retailer is fully compliant with the 2018 Farm Bill.

Chargeback rates compound the problem. CBD merchants see chargeback rates surge 222% between Q1 2023 and Q1 2024, crossing card network thresholds that trigger automatic review and termination. That kind of growth in dispute rates signals fraud risk to processors, even when the underlying cause is customer confusion about product effects rather than actual fraud.

The structural problem with platforms like Stripe and Square is their pooled merchant account model. Thousands of merchants share a single merchant ID, which means delayed category detection causes abrupt terminations when the processor eventually identifies CBD sales in the transaction stream. A retailer can process thousands of dollars in sales for weeks before the system catches up, then face an immediate account freeze.

When termination happens, the financial damage extends well beyond lost sales. Mainstream processors place fund holds of 90 to 180 days on terminated accounts, locking up working capital at the worst possible moment. For a small CBD retailer carrying inventory, that kind of cash flow disruption can be fatal to the business.

- Stripe, PayPal, and Square all explicitly prohibit CBD in their acceptable use policies

- Rolling reserves of 5% to 10% are standard even on approved high-risk accounts

- Fund holds after termination run 90 to 180 days, freezing operating capital

- Chargeback thresholds above 1% trigger automatic review on Visa and Mastercard networks

- Regulatory ambiguity at the federal level gives processors legal cover to refuse the category entirely

Pro Tip: Before applying to any processor, pull your chargeback ratio from your current processor's reporting dashboard. If it exceeds 1%, address the root cause first. Processors see that number immediately during underwriting, and a high ratio will get your application declined before a human ever reviews it.

Specialized processors vs. mainstream options for CBD payments

The comparison between specialized high-risk merchant accounts and mainstream processors is not close on stability, but the cost difference is real and worth understanding before you commit.

| Factor | Mainstream Processors (Stripe, Square, PayPal) | Specialized CBD Processors |

|---|---|---|

| CBD acceptance | Prohibited | Explicitly supported |

| Processing fees | 2.9% + $0.30 standard | 3% to 8% depending on volume and product type |

| Account stability | High termination risk | Dedicated underwriting, stable accounts |

| Fund holds | 90 to 180 days on termination | Rolling reserve of 5% to 10%, released on schedule |

| Chargeback support | Minimal, automated | Active dispute management |

| Compliance support | None | FDA and state law guidance included |

| POS integration | Broad (Square hardware, Stripe Terminal) | Varies by processor; most support major POS systems |

Specialized CBD processors like PaymentCloud, Dharma Merchant Services, and eMerchantBroker are the leading providers in this space. Each offers dedicated merchant accounts with acquiring banks that have explicitly approved CBD as a permitted product category. That distinction matters enormously. A dedicated account means your business has its own merchant ID, its own underwriting file, and its own relationship with the acquiring bank. There is no pooled account risk.

The fee range of 3% to 8% reflects real underwriting costs. Processors absorb more risk with CBD accounts, and the pricing reflects that. However, the fee spread within that range is wide, and volume matters. A retailer processing $50,000 per month will negotiate better rates than one processing $5,000. Product type also affects pricing: edibles and ingestibles carry higher rates than topicals because the regulatory risk profile is different.

Rolling reserves are the other cost to model carefully. Most specialized processors hold 5% to 10% of gross sales in reserve for a period of 90 to 180 days. That reserve is eventually released, but it represents real capital tied up in escrow. A retailer doing $30,000 per month at a 10% reserve has $27,000 locked up after nine months of processing. That is not a hidden fee, but it is a cash flow consideration that many merchants underestimate when switching processors.

The integration question is practical and solvable. Most specialized processors support API connections to platforms like WooCommerce, Shopify (through third-party gateways), and BigCommerce. For physical retail, processors like PaymentCloud offer compatible terminals that work with common POS systems. The setup process is more involved than plugging in a Square reader, but the dedicated merchant account stability that results is worth the configuration time.

What alternative payment methods work for CBD retailers?

Beyond specialized card processors, CBD merchants have three categories of alternative payment methods that bypass traditional banking intermediaries entirely: cryptocurrency, ACH direct bank transfers, and hybrid checkout models that combine multiple rails.

Cryptocurrency payments, specifically stablecoins like USDC and USDT, represent the most structurally different option. Crypto accepts USDC or USDT payments directly with irreversible transactions and zero chargebacks. That last point is significant. Chargebacks are one of the primary reasons processors flag CBD merchants, so eliminating them from a portion of your transaction volume directly reduces your risk profile. There are no card network rules, no merchant category codes, and no acquiring bank to terminate your account.

The practical limitation is customer adoption. Most retail CBD customers do not hold stablecoins, and asking them to set up a crypto wallet at checkout creates friction that reduces conversion. Crypto payments work best for online stores with a tech-forward customer base, or as a secondary option rather than the primary checkout method.

ACH and direct bank transfer services like Trustly and Plaid-connected bank pay options offer a middle path. These methods pull funds directly from a customer's bank account, bypassing card networks entirely. Fees run significantly lower than card processing, typically 0.5% to 1.5%, and there is no card network chargeback mechanism. The tradeoff is that ACH transfers take one to three business days to settle, which affects cash flow timing.

The most practical implementation strategy for most CBD retailers is a hybrid checkout model:

- Set up a dedicated high-risk merchant account as your primary card processing rail

- Add an ACH or bank transfer option at checkout for customers willing to use it

- Integrate a crypto payment gateway (BitPay, Coinbase Commerce, or NOWPayments) as a third option

- Test the mix by routing 20% of transactions to crypto checkout for 30 days to measure adoption and net revenue impact

- Adjust the checkout presentation based on actual customer behavior data

| Payment Method | Typical Fee | Settlement Time | Chargeback Risk | Customer Adoption |

|---|---|---|---|---|

| High-risk card processor | 3% to 8% | 1 to 2 days | Moderate (1.5% to 3%) | High |

| ACH / bank transfer | 0.5% to 1.5% | 1 to 3 days | Low | Moderate |

| Crypto (USDC/USDT) | 0.5% to 1% | Near instant | Zero | Low to moderate |

Pro Tip: When presenting crypto or ACH options at checkout, frame them as a benefit to the customer, not a workaround. "Pay directly from your bank and skip card fees" converts better than any technical explanation of why you offer the option.

How to implement payment alternatives as a CBD retailer

Implementing a multi-rail payment setup requires a structured approach. The goal is redundancy: no single processor termination should be able to stop your business from accepting payments.

-

Audit your current setup first. Identify every payment touchpoint, online checkout, in-store terminal, and invoice payments, and document which processor handles each. This map reveals single points of failure before they become emergencies.

-

Select a specialized processor with explicit CBD underwriting. Apply to processors that have a documented history with CBD merchants and acquiring bank relationships that specifically permit the category. Review the merchant agreement for the reserve percentage, reserve release schedule, and termination notice period before signing.

-

Integrate with your existing POS and e-commerce platform. Most specialized processors provide API documentation and support for WooCommerce, Magento, and Shopify-compatible gateways. For physical retail, confirm terminal compatibility before committing to a processor. Paysec's CBD payment accounts integrate with both retail and online environments, reducing the technical lift for merchants managing both channels.

-

Add ACH as a checkout option. Services like Dwolla, Trustly, or bank-linked payment options through Plaid connect directly to your e-commerce platform. The lower fee structure on ACH transactions meaningfully reduces your blended processing cost when a portion of customers adopt it.

-

Monitor your chargeback ratio weekly, not monthly. Most processors provide a dashboard showing dispute rates in near real time. Keeping your ratio below 0.9% gives you a buffer before hitting the 1% threshold that triggers automatic review. Respond to every dispute within 24 hours with transaction evidence, delivery confirmation, and product documentation.

-

Establish a backup processor before you need one. Apply to a second specialized processor and keep the account active with a small transaction volume each month. When your primary processor has issues, you switch immediately rather than spending weeks in a new underwriting process.

The high-risk merchant processing landscape in 2026 rewards merchants who treat payment infrastructure as a core business system rather than a vendor relationship. Retailers who build redundancy into their payment stack from the start avoid the cash flow crises that derail competitors.

Key takeaways

CBD merchants who build multi-rail payment infrastructure with a dedicated high-risk processor, ACH transfers, and crypto options eliminate the single points of failure that cause most payment disruptions.

| Point | Details |

|---|---|

| Mainstream processors ban CBD | Stripe, PayPal, and Square prohibit CBD, making specialized accounts the only stable card processing option. |

| High-risk fees are real but manageable | Fees of 3% to 8% reflect actual underwriting costs; volume and product type determine where you land in that range. |

| Crypto eliminates chargebacks | USDC and USDT payments carry zero chargeback risk, directly reducing the metric processors use to flag CBD accounts. |

| Hybrid checkout reduces disruption risk | Combining card, ACH, and crypto rails means no single termination can stop your business from accepting payments. |

| Rolling reserves require cash flow planning | Reserves of 5% to 10% held for 90 to 180 days represent real capital; model this before switching processors. |

The payment problem most CBD retailers solve too late

From working directly with merchants across high-risk industries, the pattern is consistent: CBD retailers treat payment processing as a problem to solve once, not a system to maintain. They find a processor that approves them, set it up, and move on. Then the termination notice arrives and they are scrambling.

The merchants who operate without payment disruptions share one practice. They run two active processing relationships at all times. Not as a backup plan, but as standard operating procedure. When one processor tightens underwriting or changes policy, the other rail keeps revenue flowing while they find a replacement. That redundancy is not expensive to maintain. A low monthly volume on a second account costs almost nothing compared to the cost of a week without payment processing.

The other insight that rarely appears in generic payment guides: your chargeback ratio is a marketing problem as much as a payment problem. Most CBD chargebacks come from customers who did not understand what they were buying, expected different results, or could not reach customer service. Fixing product descriptions, adding clear dosage guidance, and making your return policy visible at checkout reduces disputes more reliably than any payment processor feature. Processors see your chargeback ratio. Your marketing directly controls it.

The long-term outlook for CBD payment processing is improving. More acquiring banks are building explicit CBD programs, fee ranges are compressing as competition increases, and stablecoin payment infrastructure is maturing. Merchants who build compliant, well-documented operations now will be positioned to access better pricing as the market normalizes. The merchants who cut corners on compliance or try to obscure their product category will face permanent blocks from the processors who matter most.

— Paysec Marketing Team

How Paysec helps CBD retailers process payments with confidence

CBD retailers working with Paysec get dedicated merchant accounts built specifically for high-risk industries, with transparent pricing through Network Offset Pricing that delivers measurable savings of 30% to 60% compared to standard high-risk rates. There are no hidden fees, no minimums, and no long-term contracts.

Paysec's interchange pricing model passes wholesale rates directly to merchants, which is a structural advantage for CBD retailers who are already absorbing elevated processing costs. Terminals for countertop, wireless, and mobile retail environments connect to the same account, so online and in-store transactions run through a single reporting dashboard. Detailed transaction reporting gives CBD merchants the financial visibility they need to monitor chargeback ratios, track reserves, and demonstrate compliance to acquiring banks. Getting started is straightforward, with dedicated support from day one.

FAQ

Why do Stripe and PayPal ban CBD merchants?

Stripe and PayPal prohibit CBD products in their acceptable use policies due to regulatory uncertainty around FDA classification and elevated chargeback rates. Their pooled merchant account model also makes CBD category detection and compliance management impractical at scale.

What fees do specialized CBD payment processors charge?

Specialized high-risk processors charge between 3% and 8% in processing fees, depending on monthly volume, product type, and chargeback history. Most also require a rolling reserve of 5% to 10% held for 90 to 180 days.

Can CBD merchants use cryptocurrency to accept payments?

Yes. Stablecoins like USDC and USDT allow CBD merchants to accept payments with zero chargebacks and no card network restrictions. The primary limitation is customer adoption, which makes crypto most effective as a secondary checkout option alongside card processing.

What is a rolling reserve and how does it affect CBD retailers?

A rolling reserve is a percentage of gross sales, typically 5% to 10%, held by the processor for a set period before release. It protects the processor against chargebacks and represents real working capital that CBD merchants must account for in their cash flow planning.

How many payment processors should a CBD retailer maintain?

CBD retailers should maintain at least two active processing relationships at all times. Running a second specialized processor with a low monthly volume costs little but provides immediate failover if the primary processor terminates the account or changes its CBD policy.