TL;DR:

- Payment data security involves encryption, tokenization, and layered authentication measures to prevent unauthorized access during transactions. Using hosted payment forms, TLS encryption, and real-time fraud detection minimizes PCI scope, helps ensure compliance, and reduces breach impact. Ongoing staff training, organizational coordination, and strategic backups are essential for maintaining a robust payment security program.

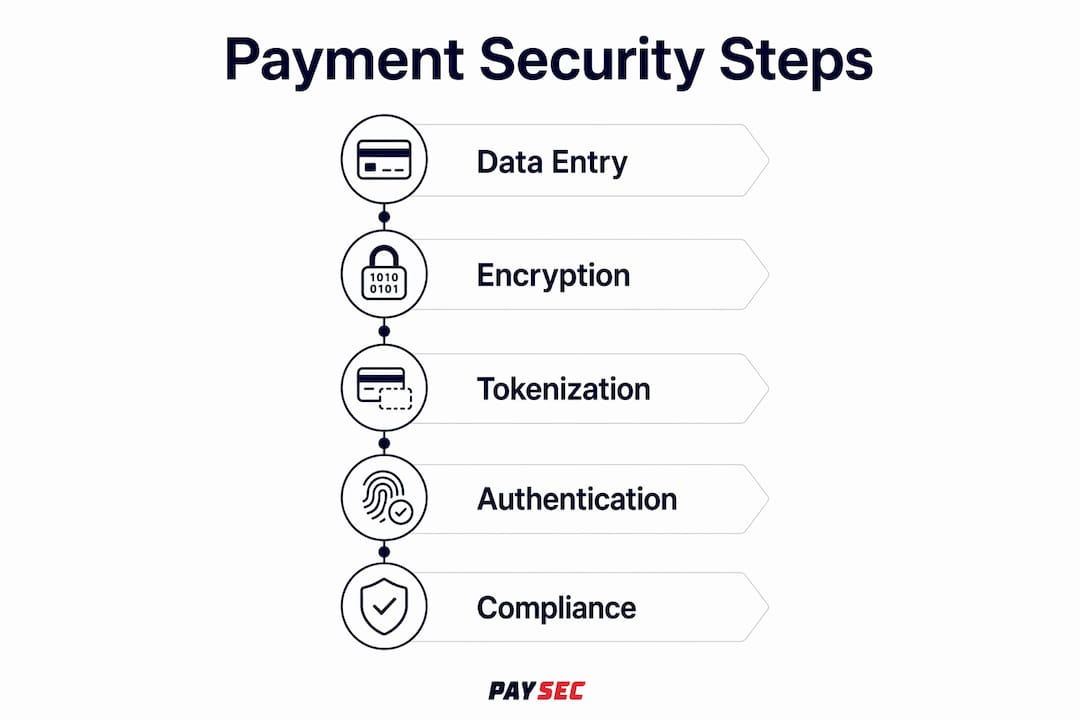

Payment data security is the process of protecting sensitive financial information through encryption, tokenization, and authentication to prevent unauthorized access during transaction processing. Every time a customer pays by card, their Primary Account Number (PAN), expiration date, and CVV travel through a chain of systems including payment gateways, card networks like Visa and Mastercard, acquiring banks, and issuing banks. Each link in that chain applies specific data security measures to keep cardholder data out of the wrong hands. Standards like PCI DSS 4.0 and technologies like TLS 1.3 encryption and 3-D Secure authentication define how payment data security works in practice today.

How payment data security works at the point of entry

The moment a customer types their card number into a checkout form, the security architecture either protects that data or exposes it. The safest implementations never let raw card data touch your servers at all. Tools like Stripe Elements or Braintree's hosted fields render a payment form inside an iframe controlled entirely by the payment processor. Your application receives only a token, not the actual PAN.

When raw card data does enter a system, TLS 1.3 encrypts it immediately in transit. TLS 1.3 is the current standard for transport layer security, and it eliminates older cipher suites that were vulnerable to downgrade attacks. No payment data should move between systems over anything less. The secure payment processing pipeline depends on this encryption being in place before data leaves the browser.

Tokenization takes over once the data arrives at the processor. The processor replaces the raw PAN with a randomly generated token, stores the mapping in a token vault, and returns the token to your system. Your database stores tokens, not card numbers. If your database is breached, attackers get strings of meaningless characters. Network tokenization produces approximately 30% lower online fraud rates and a 3 to 4% increase in transaction approval rates compared to storing PANs. That approval rate lift happens because card networks can validate tokens more confidently than raw PANs.

Two additional technical controls matter here:

- Idempotency keys: Every API call that changes transaction state must include a unique idempotency key. Idempotency keys prevent duplicate charges caused by network timeouts, which are a common integration bug that can result in double billing and compliance headaches.

- Webhook signature verification: When your payment processor sends event notifications, verifying the HMAC signature on each webhook confirms the message came from a legitimate source and was not tampered with in transit.

Pro Tip: If you are building a new checkout flow, start with hosted payment fields. This single decision reduces your PCI DSS scope to SAQ A and eliminates the need for your team to handle raw card data at any point.

How authentication and fraud prevention protect each transaction

Authentication answers one question: is this transaction being initiated by the legitimate cardholder? The answer requires more than a correct card number. Modern payment security uses layered signals to make that determination in real time.

3-D Secure 2.3.1 is the current authentication standard used by Visa (Visa Secure) and Mastercard (Identity Check). It works by sharing rich contextual data between the merchant, the card network, and the issuing bank during the authorization request. 3-D Secure 2.3.1 enables risk-based authentication challenges, improving issuer decisions and reducing false declines. Low-risk transactions pass through frictionlessly. High-risk transactions trigger a challenge, such as a one-time passcode sent to the cardholder's phone. This balance matters because unnecessary friction causes cart abandonment.

Fraud detection runs in parallel with authentication. The main techniques processors and fraud platforms use include:

- Device fingerprinting: Collects browser attributes, screen resolution, installed fonts, and IP address to build a device profile. Mismatches between the device profile and the cardholder's history flag suspicious activity.

- Velocity checks: Monitor how many transactions a single card, IP address, or device attempts within a defined time window. Rapid-fire attempts are a hallmark of card testing attacks.

- Location analysis: Compares the billing address, shipping address, and IP geolocation. A card registered in Ohio being used from an IP in Eastern Europe with a shipping address in Nevada is a high-risk signal.

- Behavioral biometrics: Some advanced platforms analyze how a user types, moves a mouse, or scrolls. Bots and fraudsters exhibit measurably different patterns than legitimate customers.

Multi-factor authentication (MFA) applies not just to cardholders but to everyone inside your organization who accesses payment systems. MFA must be enforced on admin panels and cloud consoles, because breaches frequently originate from compromised employee credentials rather than external attacks. A finance team member whose password is phished becomes an entry point into your entire payment infrastructure if MFA is absent.

The complete authorization round-trip completes within 800ms to 1,500ms. All of the above checks, encryption, tokenization, fraud scoring, and authentication happen within that window. The speed is possible because card networks like Visa and Mastercard run distributed authorization infrastructure designed for exactly this workload.

What compliance frameworks actually require you to do

PCI DSS 4.0, which became the mandatory standard in March 2025, defines the technical and operational controls every business that accepts card payments must implement. The framework organizes requirements into 12 domains covering network security, access control, encryption, monitoring, and incident response. Understanding PCI DSS is not optional for finance professionals. Non-compliance exposes your business to fines, increased processing fees, and liability for fraud losses.

The most practical compliance lever available to most businesses is minimizing PCI scope. Hosted payment pages reduce PCI-DSS scope to SAQ A, the simplest self-assessment questionnaire. SAQ A requires roughly 22 controls. SAQ D, which applies to businesses that store, process, or transmit cardholder data on their own systems, requires over 200 controls and a Qualified Security Assessor (QSA) audit. The architecture decision you make at the start of a project determines which path you walk.

Beyond scope management, PCI DSS 4.0 emphasizes several operational practices:

- Network segmentation: Payment systems must be isolated from general business networks. A flat network where the point-of-sale system shares a subnet with employee laptops violates this requirement and dramatically increases breach risk.

- Least privilege access: Every employee and system account should have access only to the data and functions required for their specific role. A customer service representative has no legitimate need to see full PANs.

- Continuous logging and monitoring: All access to cardholder data environments must be logged. Logs must be reviewed regularly and retained for at least 12 months. Security Information and Event Management (SIEM) tools like Splunk or Microsoft Sentinel automate this process.

- Penetration testing: PCI DSS 4.0 requires annual penetration tests and testing after significant infrastructure changes. This is not a checkbox exercise. A skilled penetration tester will find vulnerabilities your internal team missed.

- Incident response plans: A documented, tested incident response plan is mandatory. The plan must define who does what within the first 24 hours of a confirmed breach, including notification obligations to card networks and affected cardholders.

Compliance is a continuous program, not an annual audit. Businesses that treat PCI DSS as a once-a-year exercise consistently fail to catch configuration drift, new vulnerabilities, and access control violations that accumulate between assessments.

How architecture choices shape your security and compliance burden

Where card data first enters your system defines your entire compliance scope. This is the single most consequential technical decision in payment system design, and many businesses get it wrong by defaulting to custom card capture forms without understanding the implications.

| Architecture | PCI DSS scope | Audit requirement | Relative cost |

|---|---|---|---|

| Hosted payment page (e.g., Stripe Checkout) | SAQ A | Self-assessment | Low |

| Hosted fields / iframes | SAQ A | Self-assessment | Low |

| Custom card capture form, processor tokenizes | SAQ A-EP | Self-assessment + scan | Medium |

| Custom card capture, self-hosted vault | SAQ D or Level 1 | QSA audit | High |

Card data entry point determines PCI-DSS scope. Hosted fields reduce scope to SAQ A, while custom capture forms increase scope and require more costly audits. Building a custom card vault means your engineering team is responsible for encryption key management, hardware security modules (HSMs), access controls, and audit trails. That is a significant ongoing investment that most businesses outside of large financial institutions cannot justify.

For SaaS companies and eCommerce operators, the right default is a hosted payment page or hosted fields from a processor like Stripe, Adyen, or Braintree. You get PCI SAQ A scope, the processor handles tokenization and vault security, and your team focuses on product rather than compliance infrastructure. Finance professionals evaluating the SaaS payment stack should treat scope reduction as a primary selection criterion when choosing a payment processor.

Pro Tip: When evaluating payment processors, ask specifically whether their hosted fields implementation qualifies for SAQ A. Some implementations that appear hosted actually inject JavaScript into your page in ways that expand your scope to SAQ A-EP. Get the answer in writing.

Integrating payment security into your broader organizational risk management

Payment data security does not live in a silo. It intersects with HR policies, IT infrastructure, finance operations, and vendor management. Businesses that treat it as purely a technology problem consistently underestimate their exposure.

Staff training is the most underinvested control in most organizations. Human error is a leading cause of payment data exposure incidents. Training staff to avoid writing down payment information, pasting card numbers into support tickets, or sharing credentials eliminates an entire category of risk that no technical control can fully address. This training needs to happen at onboarding and annually thereafter, not just when a breach occurs.

Organizational coordination across finance, IT, and compliance teams determines how quickly your business detects and responds to fraud. Effective coordination requires:

- A defined owner for payment security who has authority to enforce policy changes

- Regular cross-functional reviews of fraud monitoring dashboards and transaction anomalies

- Clear escalation paths when fraud thresholds are breached or suspicious patterns emerge

- Vendor security reviews for every third party that touches payment data, including accounting software integrations and ERP connectors

Backup strategy is a frequently overlooked component of payment data protection. Encryption alone is insufficient against ransomware. If your encrypted backups are connected to the same network that ransomware has compromised, attackers can encrypt or delete those backups too. The 3-2-1 strategy recommended by the Australian Cyber Security Centre requires three copies of data, on two different media types, with one copy stored off-site and offline. For payment data environments, this means verified, air-gapped backups that ransomware cannot reach.

Modern payment platforms reduce the manual burden of these operational controls significantly. When you work with a processor that handles tokenization, fraud monitoring, and PCI compliance infrastructure, your internal team focuses on policy, training, and vendor oversight rather than building and maintaining security systems from scratch. Businesses exploring options to switch payment processors often discover that a better processor also means a materially lower compliance burden.

Key takeaways

Payment data security works through a layered system of encryption, tokenization, authentication, and compliance controls that together minimize the exposure of sensitive financial information at every stage of a transaction.

| Point | Details |

|---|---|

| Tokenization reduces fraud | Network tokenization cuts online fraud by approximately 30% and improves approval rates by 3 to 4%. |

| Architecture defines compliance scope | Hosted payment pages limit PCI DSS scope to SAQ A, reducing audit costs and compliance complexity. |

| Authentication must be layered | 3-D Secure 2.3.1 and MFA on admin access together address both customer-facing and internal threat vectors. |

| Compliance is continuous | PCI DSS 4.0 requires ongoing monitoring, penetration testing, and incident response planning, not annual checkboxes. |

| Human error is a real threat | Staff training on payment data handling eliminates risks that encryption and tokenization cannot address alone. |

What we have learned building payment security programs

The Paysec Marketing Team's perspective on what actually moves the needle.

The most common mistake we see is businesses treating payment security as a technical project with a finish line. There is no finish line. Configuration drift, new integrations, staff turnover, and evolving attack techniques mean your security posture degrades continuously unless you actively maintain it.

The second mistake is underestimating internal threats. Most security conversations focus on external attackers. The reality is that compromised credentials, misconfigured access controls, and accidental data exposure by employees account for a significant share of payment data incidents. Enforcing MFA on every system that touches payment data and auditing access permissions quarterly are not glamorous tasks, but they close more real vulnerabilities than most technical investments.

The principle we advocate most strongly is "touch as little data as possible." Every system that stores, processes, or transmits cardholder data is a liability. The most effective payment security strategy in 2026 is a layered approach that emphasizes minimizing data touchpoints through hosted payment pages and tokenization. When your systems never see raw card data, the consequences of a breach are dramatically reduced. A token database is worthless to an attacker.

We also see businesses underinvest in incident response planning until after a breach. A documented, tested plan that your finance, IT, and compliance teams have actually rehearsed is worth more than any single technical control. The first 24 hours after a confirmed breach determine the regulatory and reputational outcome. Know exactly what you will do before you need to do it.

— Paysec Marketing Team

How Paysec helps you secure payment data without the overhead

Paysec builds payment security directly into its processing infrastructure, so you get tokenization, hosted payment fields, and real-time fraud monitoring without assembling those capabilities yourself.

Paysec's architecture is designed to keep your PCI scope at SAQ A by default, which means your compliance program stays manageable regardless of your transaction volume. The platform integrates with major eCommerce and SaaS environments, and its Network Offset Pricing model means you retain full revenue while operating on a secure, compliant payment stack. Businesses across 18+ industries have reduced processing costs by 30 to 60% while gaining the merchant services and security infrastructure that larger enterprises typically pay significantly more to maintain. Explore what Paysec can do for your payment operations at paysec.ai.

FAQ

What is the difference between encryption and tokenization in payments?

Encryption transforms card data into unreadable ciphertext that can be decrypted with the correct key. Tokenization replaces card data with a random token that has no mathematical relationship to the original number, making it useless even if the decryption key is compromised.

What PCI DSS level applies to most small businesses?

Most small businesses using hosted payment pages qualify for SAQ A, which requires approximately 22 controls and no external QSA audit. Businesses that process card data on their own servers face SAQ D requirements, which involve over 200 controls and a formal audit.

How does 3-D Secure reduce fraud without hurting conversions?

3-D Secure 2.3.1 uses risk-based authentication to pass low-risk transactions through without a challenge step. Only high-risk transactions trigger additional verification, which reduces friction for the majority of legitimate customers while blocking suspicious activity.

Why is MFA required for payment system admin access?

Breaches frequently originate from compromised employee credentials rather than external attacks. MFA on admin panels and cloud consoles blocks attackers who obtain a valid password, because they still cannot complete the second authentication factor.

What is the 3-2-1 backup rule and why does it matter for payment data?

The 3-2-1 rule requires three copies of data on two different media types with one copy stored off-site and offline. Verified offline backups following this strategy protect payment data from ransomware attacks that can encrypt or destroy backups connected to the same network.