TL;DR:

- Embedded payments integrate native transaction processing into digital platforms, reducing friction and increasing control. Using models like Stripe Connect, marketplaces select account types and payment flows to optimize compliance, user experience, and operational efficiency. Early implementation of best practices and infrastructure simplifies scaling and enhances vendor trust, fueling market growth.

An embedded payments marketplace is a platform that integrates payment processing directly into its digital environment, allowing buyers and sellers to transact without leaving the platform or interacting with a separate payment provider. Rather than redirecting users to an external checkout page, the payment experience becomes a native feature of the product itself. Frameworks like Stripe Connect and APIs from providers like NMI make this possible by handling the technical and regulatory infrastructure behind the scenes. The embedded payment market was $39.14 billion in 2025 and is projected to reach $430.29 billion by 2033, growing at a CAGR of 35.5%. That trajectory signals one clear reality: embedded payment solutions are no longer a feature differentiator. They are a baseline expectation for any serious marketplace.

What is an embedded payments marketplace and how does it work?

An embedded payments marketplace works by routing money between buyers, sellers, and the platform itself through a single, unified payment infrastructure. The platform acts as the orchestrator, collecting funds from buyers and distributing them to vendors while deducting its own fees in the same transaction flow. This is fundamentally different from asking vendors to set up their own merchant accounts and handle payments independently.

The mechanics rely on three core components: connected accounts for vendors, a payment routing model, and a payout schedule. Each component shapes how money moves, who holds liability, and how compliance is managed. Getting these decisions right at the architecture stage saves enormous operational headaches later.

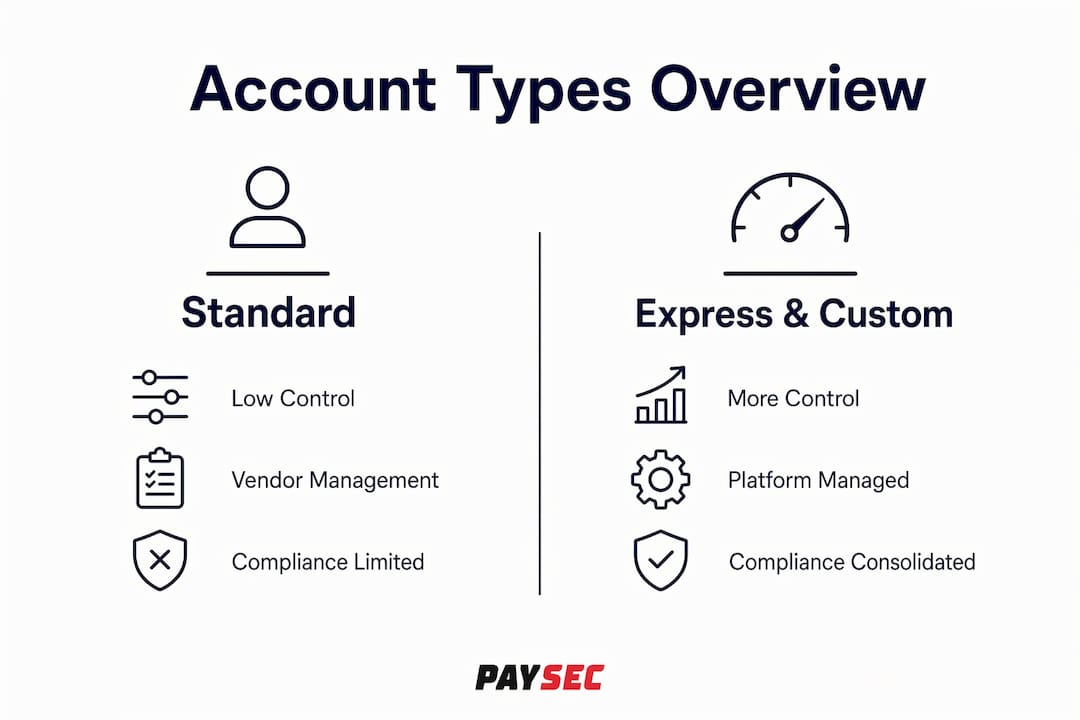

Account types: Standard, Express, and Custom

Stripe Connect account types for embedded marketplaces fall into three categories, each representing a different balance of control, compliance responsibility, and onboarding complexity.

| Account Type | Platform Control | Compliance Responsibility | Best For |

|---|---|---|---|

| Standard | Low | Stripe handles it | Simple marketplaces, fast launch |

| Express | Medium | Stripe handles KYC/AML | Most growth-stage marketplaces |

| Custom | High | Platform handles 100% | Enterprise platforms with legal teams |

Standard accounts redirect vendors fully to Stripe for onboarding and dashboard management. The platform loses visibility into vendor activity, but onboarding is frictionless. Express accounts give vendors a simplified Stripe Dashboard while Stripe manages KYC/AML compliance, reducing the operational burden on the marketplace significantly. Custom accounts hand the platform complete control over the user interface and compliance tracking, but that control comes with a steep cost. Platforms using Custom accounts absorb 100% of the compliance responsibility, including ongoing identity monitoring.

Payment flow models explained

Three primary payment flow models govern how money moves in a marketplace:

- Destination charges: The platform charges the buyer and routes funds to a connected vendor account. The platform controls the fee split and payout timing.

- Direct charges: The vendor's connected account charges the buyer directly. The platform collects an application fee. This model works well when vendors need full ownership of their transaction records.

- Separate charges and transfers: The platform charges the buyer in one transaction and transfers funds to vendors in a separate step. This model offers the most flexibility for complex fee structures but requires careful reconciliation.

Payout schedules are a critical design decision. Paying vendors too quickly reduces the platform's window to manage disputes and refunds. Paying too slowly damages vendor trust and retention. Most growth-stage marketplaces settle on a two to seven day rolling payout window as a practical middle ground.

Pro Tip: Define your fee deduction logic, payout timing, and refund handling before writing a single line of integration code. Retrofitting these decisions into a live marketplace is far more expensive than designing them correctly from the start.

What are the benefits of embedded payments for marketplaces?

Embedded payments allow customers to complete transactions without being redirected to external sites, which directly reduces checkout friction and improves conversion rates. For marketplace operators, the benefits extend well beyond user experience.

The most significant operational benefit is compliance consolidation. With Express accounts, the payment provider manages Know Your Customer (KYC) and Anti-Money Laundering (AML) checks on vendors. The marketplace does not need to build or maintain that infrastructure. For early-stage platforms, this alone can represent months of saved development time and significant legal cost avoidance.

Revenue visibility improves as well. Because all transactions flow through a single platform account before being distributed, the marketplace has a complete, real-time view of gross merchandise volume, fee income, and vendor payouts. This data is invaluable for financial reporting, investor updates, and pricing decisions.

The growth numbers reinforce the business case. The embedded payment market is expanding at 35.5% annually through 2033, meaning platforms that build this capability now are positioning themselves ahead of a market shift that is already underway. Competitors who rely on redirecting users to external payment pages will face increasing conversion rate disadvantages as buyer expectations shift toward fully native checkout experiences.

Key benefits at a glance:

- Reduced cart abandonment from native, in-platform checkout

- Simplified vendor onboarding through managed KYC/AML with Express accounts

- Centralized transaction data for reconciliation and reporting

- Platform fee collection automated within the payment flow

- Faster dispute resolution through unified transaction records

The challenge worth acknowledging is the compliance cost of Custom accounts. Platforms that choose Custom for maximum control often underestimate the ongoing cost of identity monitoring, sanctions screening, and regulatory reporting. That cost is not a reason to avoid embedded payments. It is a reason to choose the right account model from the beginning.

Embedded vs. integrated vs. traditional payment processing

These three terms are frequently used interchangeably, but they describe meaningfully different architectures with different implications for user experience, platform control, and compliance.

Integrated payments connect software to payment providers via APIs, but the payment experience still exists as a distinct layer. A SaaS billing tool that connects to a payment gateway via API is integrated. The payment still feels like a separate step. Embedded payments go further: the payment feature becomes native to the product. The user never perceives a boundary between the platform and the payment.

Traditional payment processing is the oldest model. Merchants apply for their own merchant accounts, integrate a payment gateway independently, and manage their own compliance. For a marketplace with dozens or hundreds of vendors, requiring each vendor to manage their own payment infrastructure is operationally unworkable.

| Model | User Experience | Platform Control | Compliance Owner | Typical Use Case |

|---|---|---|---|---|

| Traditional | Separate checkout | None | Merchant | Standalone retail |

| Integrated | Connected but visible | Partial | Shared | SaaS billing tools |

| Embedded | Fully native | High | Platform or provider | Marketplaces, platforms |

The distinction matters for decision-making. A business evaluating marketplace payment integration options needs to understand that choosing an integrated approach over a truly embedded one means accepting a user experience gap that compounds over time. Buyers notice when they are redirected. Vendors notice when their payouts are slower or less transparent. The native experience that embedded payments deliver is not a cosmetic upgrade. It is a structural advantage.

For platforms operating across multiple countries, the embedded model also simplifies multi-jurisdiction payment compliance by centralizing regulatory responsibility rather than distributing it across dozens of individual vendor accounts.

Best practices to optimize embedded marketplace payments

The difference between a well-functioning embedded payments marketplace and a liability-prone one often comes down to four operational decisions made during implementation.

1. Start with Express accounts. For most marketplaces, Express is the right default. It provides a meaningful level of platform control over the user experience while delegating KYC and AML compliance to the payment provider. The Express account model gives vendors access to a simplified dashboard, which reduces inbound support requests to the platform. Reserve Custom accounts for situations where your legal and engineering teams are genuinely resourced to manage full compliance ownership.

2. Build webhook handling from day one. Robust webhook handling, including listening to "account.updated` events, is not optional. When a vendor's KYC verification is revoked, the platform must immediately stop routing payments to that account. Platforms that ignore webhook events risk continuing to pay unverified sellers, which creates both fraud exposure and regulatory liability. This is one of the most commonly neglected integration points and one of the most consequential.

3. Store PaymentIntent and Transfer IDs for every order. Structured storage of PaymentIntent and Transfer IDs per order is the operational backbone of a multi-vendor marketplace. Without these records, coordinating refunds, responding to disputes, and reconciling monthly financials becomes a manual, error-prone process. Automate this storage at the transaction level from the start.

4. Align refund policies with vendors before launch. Refund workflows in embedded marketplaces are more complex than in single-merchant stores because funds have already been split and transferred. Define clearly whether the platform absorbs refund costs initially and recovers them from vendor payouts, or whether vendors are required to maintain a reserve balance. Ambiguity here creates vendor disputes and cash flow problems.

5. Audit your pricing model against actual transaction volume. Processing fees compound at scale. A platform processing $1 million monthly at a 2.9% flat rate pays $29,000 in fees. Switching to an interchange-plus or Network Offset Pricing model can reduce that figure substantially. Review your fee structure at every major volume milestone.

Pro Tip: Set a payout schedule of two to seven days rather than instant payouts during your first six months of operation. This window gives you time to catch fraudulent transactions and process legitimate refunds before funds leave the platform.

Key takeaways

Embedded payments marketplaces succeed when platforms choose the right account model, automate compliance through webhooks, and design payment flows before writing integration code.

| Point | Details |

|---|---|

| Define payment logic first | Set fee deductions, payout timing, and refund handling before integration begins. |

| Express accounts are the practical default | They balance platform control with managed KYC/AML compliance for most marketplaces. |

| Webhooks prevent compliance failures | Listening to account.updated events stops payments to revoked vendors automatically. |

| Store transaction IDs at every order | PaymentIntent and Transfer IDs are required for refunds, disputes, and reconciliation. |

| Market growth demands action now | The embedded payment market grows at 35.5% annually, making early adoption a competitive advantage. |

Why embedded payments are a strategic decision, not just a technical one

From where we sit at Paysec, the businesses that treat embedded payments as a purely technical integration project consistently underperform compared to those that treat it as a strategic product decision. The account model you choose, the payout schedule you set, and the compliance infrastructure you build are not back-office details. They shape vendor trust, buyer experience, and your platform's ability to scale.

We have seen marketplaces launch with Custom accounts because they wanted maximum control, only to discover six months later that the compliance overhead was consuming engineering resources that should have been building product features. The platforms that chose Express from the start moved faster, onboarded vendors more smoothly, and spent their engineering budget on differentiation rather than regulatory maintenance.

The other pattern worth calling out is the tendency to underinvest in reconciliation infrastructure. Platforms often treat PaymentIntent and Transfer ID storage as a nice-to-have until the first major dispute or audit. At that point, reconstructing transaction histories manually is expensive and stressful. Building that structure from day one costs almost nothing in comparison.

Compliance is also worth reframing. Most operators view it as a cost center and a constraint. The platforms that win treat compliance as a trust signal. Vendors who know their KYC is handled professionally and their payouts are reliable stay on your platform longer and refer other vendors. That retention effect compounds over time in ways that are genuinely difficult for competitors to replicate.

The embedded payments space is growing fast, and the platforms that will capture the most value are those that build payment infrastructure with the same intentionality they apply to their core product experience.

— PaySec Marketing Team

How Paysec supports your payment marketplace goals

Paysec's Network Offset Pricing gives marketplace operators access to wholesale interchange rates, which means transaction costs that are 30 to 60% lower than standard flat-rate processing. For platforms routing significant transaction volume, that difference directly improves margin without requiring any change to the buyer or vendor experience.

Paysec works with merchants across 18+ industries, from SaaS platforms to eCommerce marketplaces, with no hidden fees, no minimums, and no long-term contracts. Detailed transaction reporting gives platform operators the financial visibility they need to manage multi-vendor payouts accurately. If you are building or scaling a marketplace and want payment infrastructure that works as hard as your product does, explore Paysec's solutions and see what zero processing fees actually looks like in practice.

FAQ

What is an embedded payments marketplace?

An embedded payments marketplace is a platform that integrates payment processing natively into its digital environment, allowing buyers and sellers to transact without leaving the platform or using a separate payment provider.

How does a payments marketplace work technically?

The platform collects payments from buyers through connected accounts, deducts its fee, and routes the remainder to vendors using payment flow models like destination charges or direct charges, all managed through a single API-based infrastructure.

What are the main benefits of embedded payments?

The primary benefits of embedded payments include reduced checkout friction, higher conversion rates, centralized compliance management, automated fee collection, and real-time transaction visibility across all vendor accounts.

What is the difference between embedded and integrated payments?

Integrated payments connect software to a payment provider via API but keep the payment experience as a distinct layer. Embedded payments make the payment feature fully native to the product, so users never perceive a boundary between the platform and the checkout.

Which account type should most marketplaces start with?

Express accounts are the recommended starting point for most marketplaces because they balance platform control with managed KYC and AML compliance, reducing operational burden while still giving vendors access to a functional dashboard.