TL;DR:

- Underwriting high-risk merchants involves assessing chargeback, fraud, and compliance risks to determine financing terms. Ongoing management of metrics like chargeback ratio and MCC classification influences account stability and costs over time. Building a detailed risk profile and actively maintaining compliance can improve processing conditions and reduce costs.

Underwriting high-risk merchants is the process by which acquiring banks and payment processors determine whether a business's potential revenue justifies the financial exposure it carries. The role of underwriting high-risk merchants goes far beyond a simple credit check. It quantifies chargeback and fraud loss exposure, assigns pricing, sets reserve requirements, and defines the contractual terms that protect the acquiring bank if things go wrong. For financial decision-makers and risk managers, understanding this process is the difference between securing stable payment processing and facing sudden account terminations or frozen funds.

What is the underwriting process for high-risk merchants?

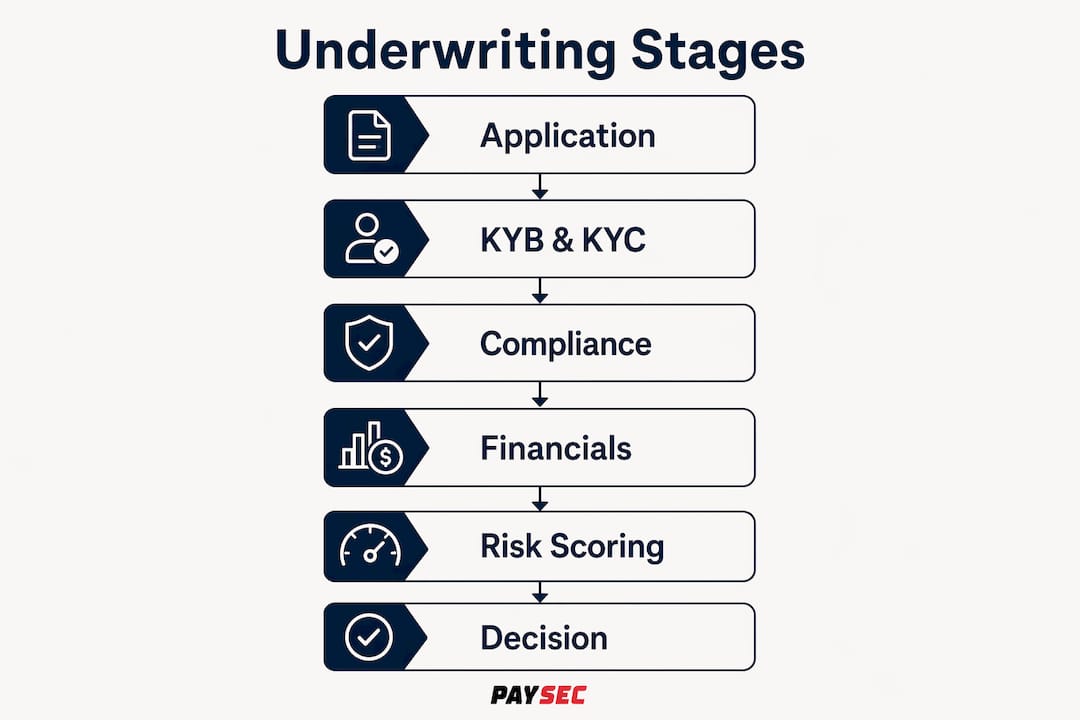

The underwriting process for high-risk merchants follows six defined stages, each designed to build a complete risk profile before any approval is granted.

Stage 1: Application intake

The merchant submits a formal application that includes business registration documents, ownership details, processing history, and a description of products or services sold. Incomplete applications trigger immediate delays. Payment processors use this stage to flag obvious disqualifiers before investing time in deeper review.

Stage 2: KYB and KYC verification

Know Your Business (KYB) and Know Your Customer (KYC) checks verify the legal existence of the business and the identity of its principals. Processors cross-reference government databases, check for sanctions, and confirm beneficial ownership. A principal who appears on a watchlist will stop the application at this stage regardless of the business's financial health.

Stage 3: Business and website compliance review

Underwriters review the merchant's website for clear refund policies, accurate product descriptions, and transparent pricing. Website and checkout transparency are critical compliance elements that directly affect approval outcomes. A subscription business with buried cancellation terms, for example, will raise immediate flags.

Stage 4: Financial analysis

Bank statements, processing history, and chargeback ratios are the core financial inputs. Underwriters look for revenue consistency, reserve adequacy, and any patterns of dispute spikes. A business with strong revenue but a chargeback ratio above 1% will face tighter terms than a lower-revenue business with clean dispute history.

Stage 5: Risk scoring

The underwriter assigns a risk score based on the combined inputs from all prior stages. This score determines the pricing tier, reserve requirement, and volume cap the merchant will receive. Industry classification and MCC assignment happen at this stage and carry significant weight.

Stage 6: Approval decision

The outcome is approval, conditional approval, or decline. Conditional approvals are common in high-risk underwriting. They typically require a rolling reserve, a lower initial processing volume cap, or additional documentation before the account can scale.

Pro Tip: Prepare at least six months of bank statements and a clean, fully compliant website before submitting a high-risk merchant application. Underwriters make faster decisions when documentation is complete on the first submission.

Which criteria are most critical in underwriting high-risk merchants?

Chargeback ratio is the single most consequential metric after industry classification in high-risk underwriting. Chargeback ratio directly influences risk management costs and pricing across every vertical. A ratio above 1.5% triggers automated hard declines at most processors, with no appeal pathway available.

Industry classification and MCC assignment

MCC (Merchant Category Code) assignment determines which underwriting pathway a merchant enters. MCC assignment and industry classification heavily influence acceptance, pricing, and the level of due diligence required. A merchant classified under a high-risk MCC, such as nutraceuticals, online gaming, or adult content, will face enhanced due diligence by default.

Being listed on an acquirer's prohibited vertical list can result in a decline regardless of financial strength. Industry classification via MCC code means that even a financially sound business can be rejected if its product category falls outside the processor's risk appetite. This is why some merchants work with specialized high-risk acquirers rather than general-purpose processors.

Key criteria underwriters evaluate

- Chargeback and dispute history: Ratios above 1% signal elevated risk. Ratios above 1.5% trigger automated hard declines that are difficult to reverse.

- MATCH list status: Appearing on the Member Alert to Control High-Risk Merchants list is a near-automatic disqualifier at most acquiring banks.

- Business model transparency: Subscription billing, free trials, and continuity programs receive heightened scrutiny because they generate disproportionate dispute volumes.

- Product and regulatory compliance: CBD, firearms accessories, and telehealth businesses must demonstrate active compliance with federal and state regulations.

- Processing volume history: Sudden volume spikes without explanation suggest fraud or business model changes that were not disclosed during the application.

- Refund policy clarity: Vague or hard-to-find refund terms correlate directly with higher dispute rates and flag compliance issues during website review.

The combined weight of these factors determines whether a merchant receives standard high-risk terms, enhanced conditions, or a decline. Risk managers who understand these criteria can prepare documentation that addresses each one before the application is submitted.

How do rolling reserves and other terms mitigate risk in high-risk underwriting?

Rolling reserves are the primary financial control acquiring banks use to manage liability exposure in high-risk merchant accounts. Rolling reserves typically withhold a fixed percentage of payments, for example 10%, for a set period such as 180 days, holding funds to cover delayed chargeback liabilities. This structure means the acquirer holds roughly two months of gross volume in reserve at any given time.

How rolling reserves work in practice

The reserve is not a fee. It is a portion of the merchant's own revenue held in a restricted account. If chargebacks occur, the acquirer draws from the reserve rather than pursuing collections. When the hold period expires, funds are released back to the merchant on a rolling basis, assuming no outstanding disputes.

| Reserve Term | Typical Range | Risk Manager Implication |

|---|---|---|

| Reserve percentage | 5%–15% of gross volume | Higher percentages reduce available working capital |

| Hold period | 90–180 days | Longer holds increase total funds tied up in reserve |

| Steady-state reserve balance | ~2 months of gross volume | Plan cash flow around this figure from day one |

| Release trigger | End of hold period, no open disputes | Clean dispute history accelerates fund release |

Negotiating reserve terms over time

Reserve terms are not fixed permanently. Negotiating reserve terms functions as a second underwriting review, where merchants with stable chargeback ratios can formally request reduced reserve percentages and shorter hold periods. Underwriting teams reassess based on actual chargeback history rather than initial risk assumptions. A merchant who maintains a chargeback ratio below 0.5% for 12 consecutive months has a strong basis for requesting a step-down in reserve requirements.

Most merchant agreements include clauses that allow the acquirer to increase reserve percentages unilaterally if chargeback ratios spike or if the merchant's business model changes materially. Risk managers should read these clauses carefully before signing. Understanding the triggers for reserve adjustments lets you build operational controls that prevent those triggers from being activated.

Pro Tip: Request a formal reserve step-down schedule in writing at the time of contract negotiation. Acquirers who agree to predefined milestones for reserve reduction give merchants a clear path to improved cash flow.

What practical impacts does underwriting have on merchant processing?

Underwriting outcomes shape every aspect of a merchant's payment processing operation, from the fees charged on each transaction to the volume of sales the account can process in a given month. Financial decision-makers who treat underwriting as a one-time event miss the ongoing nature of the relationship.

Periodic risk reviews occur post-onboarding triggered by chargeback spikes, volume growth, product changes, or customer complaints. These reviews can result in reserve increases, volume cap reductions, or account termination if the merchant's risk profile has deteriorated. Maintaining clean chargeback metrics and transparency improves longevity in high-risk payment processing.

Practical effects on operations and costs

- Transaction fees: High-risk merchants pay higher interchange-plus margins than standard merchants. The exact spread depends on the risk score assigned during underwriting.

- Volume caps: Initial approvals often include monthly processing limits. Exceeding these limits without prior approval can trigger an account review.

- Chargeback monitoring programs: Visa's Dispute Monitoring Program and Mastercard's Excessive Chargeback Program impose fines and processing restrictions on merchants whose ratios breach defined thresholds.

- Account holds: Processors can place temporary holds on settlements if fraud patterns emerge, even outside a formal review cycle.

- Reporting requirements: High-risk merchants often must provide monthly processing summaries or notify the acquirer of significant business model changes.

Strategies for maintaining favorable underwriting status

Risk managers who want to protect their processing relationships focus on four areas. First, they implement chargeback prevention strategies that address disputes before they reach the card networks. Second, they maintain clear and accessible refund policies that reduce the likelihood of customers filing disputes instead of requesting refunds. Third, they communicate proactively with their acquiring bank when volume is expected to grow significantly. Fourth, they conduct internal compliance audits of their website and checkout flow at least quarterly to catch issues before an underwriter does.

The merchants who maintain the best underwriting status over time are not necessarily those with the lowest-risk business models. They are the ones who manage their metrics actively and treat their acquiring bank as a long-term partner rather than a vendor.

Key Takeaways

Underwriting high-risk merchants is an ongoing risk management process that sets the financial terms, reserve requirements, and compliance standards governing every transaction a merchant processes.

| Point | Details |

|---|---|

| Underwriting quantifies liability | Acquirers assess chargeback and fraud exposure before approving any high-risk merchant account. |

| Chargeback ratio drives terms | Ratios above 1.5% trigger automated declines; ratios below 0.5% support reserve reduction requests. |

| MCC classification shapes the path | Industry classification determines which underwriting pathway and due diligence level applies. |

| Rolling reserves protect acquirers | A 10% reserve held for 180 days equals roughly two months of gross volume tied up at any time. |

| Ongoing compliance preserves accounts | Post-onboarding reviews triggered by volume spikes or disputes can change terms or close accounts. |

The underwriting conversation most risk managers never have

The Paysec Marketing Team has worked with merchants across more than 18 industries, and the pattern is consistent. Most financial decision-makers treat underwriting as a gate to pass through rather than a relationship to manage. They submit the application, accept the terms, and move on. That approach costs them money for years.

The reserve negotiation conversation is the one most merchants never initiate. Acquirers rarely volunteer a reserve reduction. They wait for the merchant to ask, and they expect that request to come with data. A merchant who shows up to that conversation with 12 months of clean chargeback history, a documented fraud prevention program, and a compliance-reviewed website is in a fundamentally different position than one who simply asks for better terms.

MCC classification is another area where merchants leave money on the table. If your business operates across multiple product categories, the MCC assigned at onboarding may not reflect your current revenue mix. A reclassification request, backed by current processing data, can shift your account to a lower-risk pathway and reduce your reserve requirement without changing your business at all.

The merchants who get the best long-term terms are not the ones with the cleanest initial applications. They are the ones who understand that underwriting is a living assessment, not a one-time judgment. Build your internal reporting around the metrics your acquirer watches. Review your chargeback ratio weekly, not monthly. Treat your high-risk merchant account as an asset that requires active maintenance, and your processing costs will reflect that discipline over time.

— Paysec Marketing Team

How Paysec supports high-risk merchants beyond underwriting

High-risk merchants who clear the underwriting process still face above-market processing fees that compound over time. Paysec's Network Offset Pricing addresses this directly by passing wholesale interchange rates to merchants, which produces documented savings of 30–60% on processing costs. Clients across SaaS, eCommerce, healthcare, and CBD retail have recorded measurable reductions, including a 42% drop in processing costs.

Paysec works with merchants across 18+ industries and provides detailed transaction reporting that gives risk managers the data they need to monitor chargeback metrics and stay ahead of underwriting reviews. There are no hidden fees, no minimums, and no long-term contracts. Review Paysec's merchant services to see how dedicated payment processing accounts are structured for high-risk businesses, or check the Network Offset Pricing page for a direct comparison against your current processing costs.

FAQ

What does underwriting mean for a high-risk merchant?

Underwriting for a high-risk merchant is the process by which an acquiring bank assesses chargeback and fraud exposure, then sets the fees, reserves, and volume limits that govern the merchant's account. It determines whether the business can be onboarded and on what financial terms.

Why do high-risk merchants pay higher processing fees?

Higher fees reflect the elevated chargeback and fraud risk the acquiring bank absorbs when processing transactions for high-risk business categories. The fee spread compensates the acquirer for the additional liability and monitoring costs associated with the account.

What triggers a post-onboarding underwriting review?

Post-onboarding reviews are triggered by chargeback spikes, significant volume growth, product or business model changes, or customer complaints escalated to the card networks. Merchants who experience any of these events should communicate proactively with their acquirer before a review is initiated.

Can a merchant negotiate rolling reserve terms?

Yes. Merchants with stable chargeback ratios can formally request reduced reserve percentages and shorter hold periods after demonstrating consistent performance. The best time to negotiate a step-down schedule is at the initial contract stage, before the account goes live.

What is a MATCH list and why does it matter in underwriting?

The MATCH list (Member Alert to Control High-Risk Merchants) is a database maintained by Mastercard that records merchants whose accounts were terminated for cause. Appearing on the MATCH list is a near-automatic disqualifier at most acquiring banks and significantly limits a merchant's ability to obtain new processing accounts.