TL;DR:

- A healthcare payment aggregator simplifies accepting multiple payment methods under one shared account, reducing setup time and administrative burden.

- It integrates with electronic health systems to automate payments and reconciliation, improving cash flow and patient retention.

A healthcare payment aggregator is a third-party service that enables medical practices to accept multiple types of patient payments through a single, shared master merchant account, without managing separate bank relationships for each payment channel. This model, also called a payment aggregator or sub-merchant model, sits at the center of modern payment processing in healthcare. It consolidates credit cards, debit cards, digital wallets, FSA/HSA cards, and more under one umbrella. For administrators and practice managers, understanding what is a healthcare payment aggregator means understanding how to reduce billing overhead, speed up collections, and give patients more ways to pay.

What is a healthcare payment aggregator and how does it work?

A healthcare payment aggregator acts as an intermediary between patients, their banks, and your practice. Instead of your practice applying for its own dedicated merchant account, the aggregator enrolls you as a sub-merchant under its master account. That structure is what makes near-instant digital onboarding possible, cutting setup time from weeks of traditional bank underwriting down to hours or even minutes.

The aggregator handles the relationship with card networks like Visa and Mastercard on your behalf. It routes each transaction, manages settlement, and deposits funds into your practice's bank account. You never negotiate directly with acquiring banks. That simplicity is the core value proposition for small and mid-sized practices that lack dedicated finance teams.

The trade-off built into this structure is shared risk. Because all sub-merchants operate under one master account, the aggregator applies centralized risk monitoring across its entire portfolio. That monitoring affects fees and, in some cases, eligibility for certain practice types. Knowing this upfront helps you set realistic expectations before you sign up.

How aggregators integrate with EHR and practice management systems

Integration is where aggregators create the most measurable value for healthcare administrators. A payment aggregator that connects directly to your Electronic Health Record (EHR) or Practice Management System (PMS) automates payment posting and reconciliation. That means fewer manual entries, fewer posting errors, and faster end-of-day close.

Billing confusion drives patient attrition. Research shows 36% of patients switched providers recently because of billing confusion. An aggregator integrated with your EHR presents patients with clear, accurate balances and multiple ways to pay, which directly reduces that friction. The result is better patient retention alongside improved cash flow.

Integration also enables automated payment reconciliation. When a patient pays online, the system matches the payment to the correct account and updates the ledger without staff intervention. That frees front-desk teams to focus on scheduling and patient care rather than chasing down payment records.

Pro Tip: When evaluating aggregators, ask specifically which EHR and PMS platforms they support natively. A direct API integration with systems like AdvancedMD or similar platforms eliminates manual reconciliation entirely. Paysec, for example, offers an AdvancedMD integration that removes processing fees from the equation.

Key integration capabilities to look for include:

- Real-time payment posting to patient accounts

- Automated end-of-day reconciliation reports

- Patient-facing payment portals accessible from billing statements

- Support for recurring payment plans tied to treatment schedules

- Secure tokenization that stores payment credentials for future visits

What are the benefits and trade-offs of payment aggregators in healthcare?

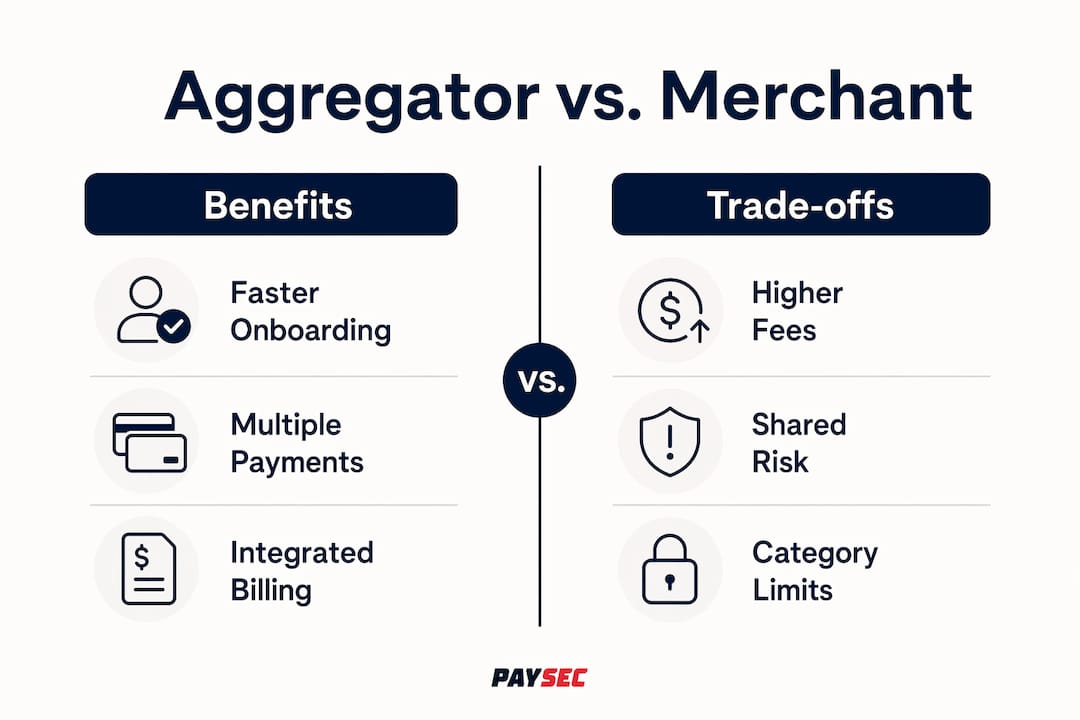

The benefits of payment aggregators are most visible at the operational level. Simplified onboarding, broad payment method acceptance, and reduced administrative burden are the three advantages that healthcare administrators cite most often. Aggregators suit small to medium practices particularly well because those organizations rarely have the transaction volume to justify the cost and complexity of a dedicated merchant account.

Faster patient payments are another concrete benefit. When patients can pay by text link, QR code, or digital wallet at checkout, collection rates rise. Practices that previously chased paper statements see a measurable drop in accounts receivable aging. That improvement in cash flow is not theoretical. It shows up in monthly revenue cycle reports.

The trade-offs are real and worth understanding before you commit. Aggregators typically charge higher per-transaction fees than dedicated merchant accounts. For a practice processing a low monthly volume, that premium is acceptable. For a high-volume specialty group or hospital system, those basis points add up quickly. Larger organizations often find dedicated accounts more cost-efficient over the long term.

Pro Tip: Calculate your monthly processing volume before choosing an aggregator. If your practice processes above a threshold where per-transaction fees exceed what a dedicated account would cost, the math favors moving to a dedicated merchant account. Paysec's Network Offset Pricing is worth reviewing as a cost benchmark.

The table below compares the aggregator model against a dedicated merchant account across criteria that matter most to healthcare practices.

| Feature | Aggregator model | Dedicated merchant account |

|---|---|---|

| Onboarding speed | Hours to days | Weeks (full underwriting) |

| Transaction fees | Higher per-transaction rate | Lower negotiated rate at volume |

| Setup complexity | Minimal | Requires bank application and review |

| Risk control | Centralized by aggregator | Managed by your practice directly |

| Best fit | Small to mid-sized practices | High-volume or specialty organizations |

| Payment method variety | Broad, out of the box | Depends on processor and contract |

One more trade-off deserves attention: category restrictions. Automated risk monitoring under aggregator models can flag certain merchant types or transaction patterns. Healthcare practices that handle high-risk billing categories, such as certain elective procedures or out-of-network billing, should review an aggregator's prohibited merchant policy before signing up. Unexpected account termination is the worst-case outcome of ignoring this step.

What payment methods and technologies do healthcare aggregators support?

Modern healthcare payment aggregators support a wide range of payment methods out of the box. That breadth is one of the clearest advantages over older, single-channel billing systems. Supported payment types typically include:

- Credit and debit cards (Visa, Mastercard, American Express, Discover)

- FSA and HSA cards, which are critical for healthcare billing

- Digital wallets such as Apple Pay and Google Pay

- UPI and bank transfer options for direct account payments

- Online patient portals with saved payment credentials

- Text-to-pay links sent directly to a patient's mobile phone

- QR code payments displayed at the front desk or on printed statements

- Batch processing for end-of-month insurance co-pay collections

Each of these methods serves a different patient segment. Older patients may prefer card-present transactions at a terminal. Younger patients expect to pay from their phones. Offering all channels from a single platform means no patient is left without a convenient option.

Batch processing and instant payouts are particularly valuable for busy practices. Batch processing lets billing staff run a single end-of-day sweep across all outstanding balances rather than chasing individual accounts. Instant or next-day payouts improve cash flow predictability, which matters when payroll and supply costs are fixed monthly obligations.

Compliance and security in healthcare payment technology

Healthcare payment processing carries compliance obligations that go beyond standard PCI DSS requirements. HIPAA governs how patient financial data is handled alongside clinical data. Any aggregator you work with must demonstrate HIPAA-compliant payment processing practices, including encrypted data transmission, secure tokenization of stored card data, and audit-ready transaction logs.

PCI DSS Level 1 compliance is the baseline standard for any aggregator handling card data at scale. Practices should request a copy of the aggregator's most recent PCI compliance certification before onboarding. That document confirms the aggregator has passed an independent security audit.

Tokenization deserves special mention. When a patient's card number is tokenized, the actual card data never touches your practice management system. The aggregator stores a token instead. That reduces your practice's liability in the event of a data breach and simplifies your own PCI compliance scope.

How to choose the right healthcare payment aggregator for your practice

Choosing the right aggregator starts with an honest assessment of your practice's transaction volume, payment method needs, and technology stack. The criteria below give you a structured way to evaluate any aggregator before you commit.

- Transaction volume: Estimate your monthly card processing volume. Aggregators are cost-effective below a certain volume threshold. Above that threshold, a dedicated merchant account typically wins on price.

- Integration compatibility: Confirm the aggregator integrates directly with your EHR and PMS. A native integration eliminates manual work. A generic API integration requires developer time to configure.

- Fee structure transparency: Request a full fee schedule including per-transaction rates, monthly fees, chargeback fees, and any volume-based adjustments. Hidden fees in medical billing are a documented problem across the industry.

- Prohibited merchant categories: Review the aggregator's restricted business list. If your practice type or billing category appears on that list, you face termination risk. Understanding prohibited categories prevents that outcome.

- Patient-facing experience: Test the patient payment portal yourself. If it is confusing or slow, patients will abandon it. A poor payment experience directly reduces collection rates.

- Support quality: Confirm the aggregator offers live support during your practice's operating hours. Payment failures at checkout need immediate resolution, not a 48-hour email queue.

- Scalability: If your practice plans to grow, add locations, or increase volume significantly, ask how the aggregator handles that transition. Some aggregators offer a path to a dedicated merchant account as volume grows.

The onboarding process itself is worth evaluating. A well-designed aggregator gets your practice processing payments quickly, with clear documentation and a straightforward setup. Paysec, for example, operates with no long-term contracts and no minimums, which removes the commitment risk that often makes administrators hesitant to switch platforms.

Pro Tip: Run a 90-day cost comparison after onboarding. Track your effective processing rate (total fees divided by total volume) and compare it to your previous billing costs. That single metric tells you whether the aggregator is delivering real savings or just shifting costs around.

Payment processing trends in 2026 point toward real-time settlements and patient-centered billing as the next wave of features aggregators will need to support. Choosing a platform that is already moving in that direction protects your practice from needing to switch again in two years.

Key Takeaways

A healthcare payment aggregator reduces administrative burden and accelerates patient collections by consolidating multiple payment methods under one shared merchant account, making it the most practical starting point for small to mid-sized practices.

| Point | Details |

|---|---|

| Core definition | An aggregator enrolls your practice as a sub-merchant under a shared master account, enabling fast setup. |

| Integration value | Direct EHR and PMS integration automates reconciliation and reduces billing errors that drive patient attrition. |

| Cost trade-off | Aggregators charge higher per-transaction fees; high-volume practices should compare costs against dedicated accounts. |

| Compliance requirement | Any aggregator must meet both PCI DSS and HIPAA standards before handling patient payment data. |

| Selection criteria | Evaluate volume thresholds, integration fit, fee transparency, and prohibited category policies before signing. |

The real shift aggregators are driving in healthcare billing

The convenience versus control trade-off is real, but most healthcare administrators focus on the wrong side of it. The conversation in billing departments tends to center on fees. The more important question is how much unbillable staff time your current system wastes on manual reconciliation, returned statements, and phone-based payment collection.

From working with practices across multiple specialties, the pattern is consistent. Practices that switch to an integrated aggregator model do not just save on processing costs. They recover hours of administrative time per week that were previously lost to manual posting and payment follow-up. That recovered time has a dollar value that rarely shows up in a fee comparison spreadsheet.

The 36% patient attrition figure tied to billing confusion is the number that should concern administrators most. A patient who leaves because they could not understand their bill or could not pay it conveniently represents lost lifetime revenue, not just a lost co-pay. Aggregators that integrate with your EHR and present patients with clear, digital payment options directly address that attrition driver.

The emerging trend worth watching is real-time settlement. Most aggregators today settle funds on a next-day or two-day cycle. Real-time settlement, already available from select platforms, eliminates that lag entirely. For practices managing tight cash flow, that difference is meaningful. Paysec's approach to healthcare payment compliance and transparent pricing puts it in a strong position as real-time settlement becomes standard.

My honest observation after working across healthcare payment implementations: the practices that get the most value from aggregators are the ones that treat payment setup as a patient experience decision, not just a finance department decision. When the payment process is easy, patients pay faster, complain less, and return more often.

— Paysec Marketing Team

How Paysec supports healthcare payment processing

Paysec gives healthcare practices a payment platform built around transparent pricing, compliance, and flexible acceptance options.

Paysec's Network Offset Pricing eliminates hidden fees and gives practices a clear view of what every transaction actually costs. Clients across healthcare and 18+ other industries report processing cost reductions of 30–60%. There are no long-term contracts and no minimums, so your practice is never locked in. Paysec also offers a full range of payment terminals for card-present transactions at the front desk, alongside digital tools for text-to-pay and online collections. If you want to see exactly how much your practice could save, Paysec's team is ready to walk you through a cost comparison with your current processor.

FAQ

What is a healthcare payment aggregator?

A healthcare payment aggregator is a third-party service that consolidates multiple patient payment methods under a single shared master merchant account. It enables practices to accept credit cards, digital wallets, FSA/HSA cards, and more without setting up separate bank relationships for each channel.

How do payment aggregators differ from dedicated merchant accounts?

Aggregators enroll practices as sub-merchants under a shared account, enabling fast setup but typically at higher per-transaction fees. Dedicated merchant accounts involve full bank underwriting, lower negotiated rates at volume, and more direct control over risk management.

Are healthcare payment aggregators HIPAA compliant?

Reputable aggregators meet both PCI DSS and HIPAA standards, using encrypted data transmission and tokenization to protect patient financial information. Practices should request proof of compliance certifications before onboarding any aggregator.

What payment methods do healthcare aggregators support?

Most aggregators support credit and debit cards, FSA/HSA cards, digital wallets, UPI, text-to-pay links, QR code payments, and batch processing for co-pay collections. The breadth of supported methods varies by platform, so confirm your required channels before signing up.

When should a practice switch from an aggregator to a dedicated merchant account?

A practice should evaluate the switch when monthly processing volume reaches a point where the aggregator's per-transaction fees exceed the cost of a dedicated account. High-volume specialty groups and multi-location organizations typically reach that threshold faster than single-provider practices.