Figuring out which payment processing software will actually lower transaction costs and integrate cleanly with retail or healthcare workflows often hits snags on hidden fees or limited device compatibility. Many well-known processors only offer flat-rate pricing that ignores card mix savings or require expensive add-ons for broader integration, locking out smaller merchants or specialized verticals. This comparison details rates, integration options, and onboarding speed across five payment processing platforms so you can pick a solution that fits your industry and volume without surprise complications.

Table of Contents

- PaySec

- Prahsys

- Elevated Payments

- YapPay

- Hyperswitch

- Comparative Analysis of Payment Processing Platforms

PaySec

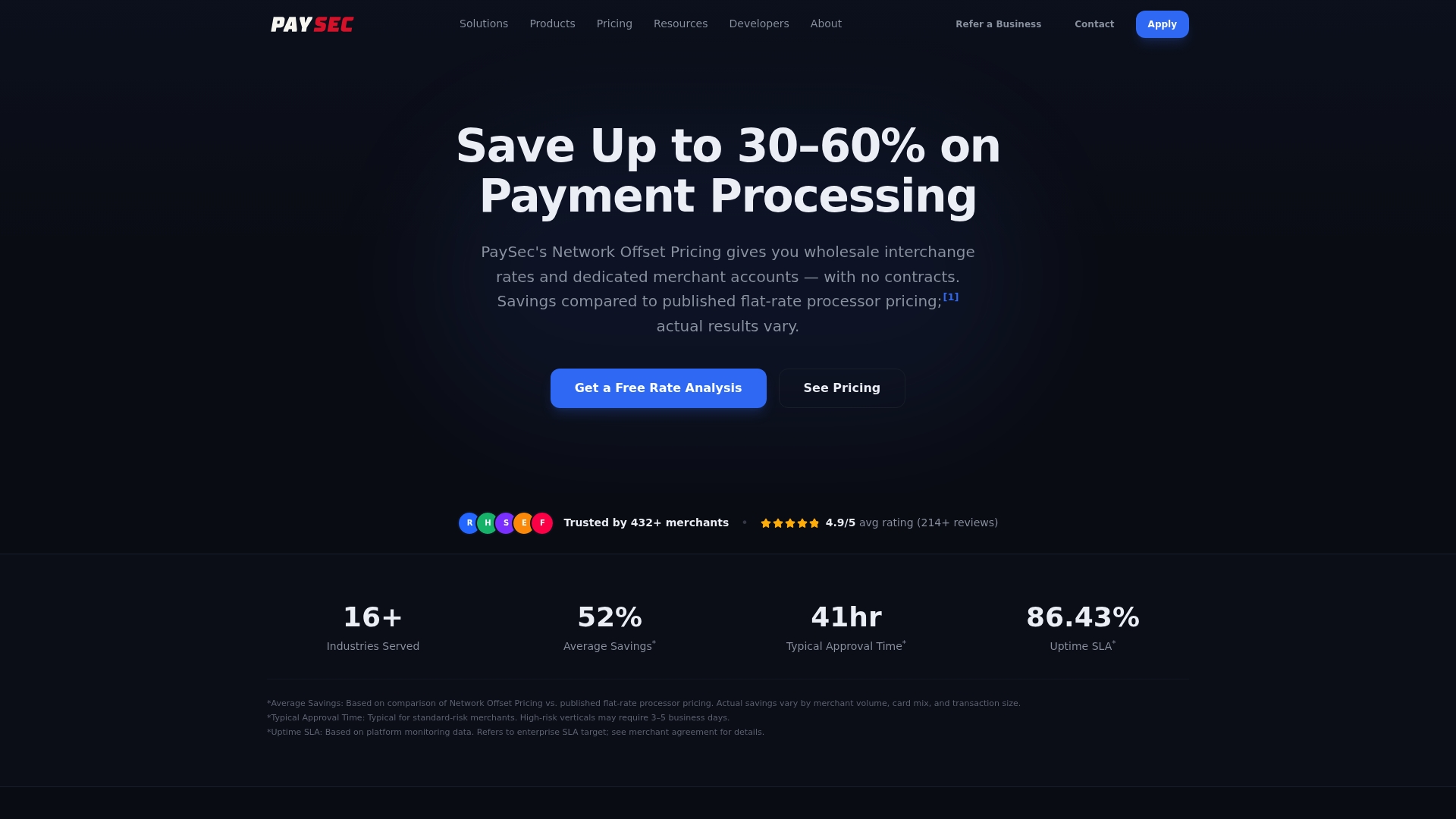

At a Glance

PaySec's marketing materials report Network Offset Pricing that typically saves merchants 30–60% versus flat-rate processors. The company advertises dedicated merchant accounts, transparent interchange pass-through with a fixed margin, and no long-term contracts or hidden fees.

Core Features

- Network Offset Pricing that passes wholesale interchange rates through to merchants with a transparent fixed margin.

- Dedicated merchant accounts to avoid aggregator risk and reduce the chance of fund holds or account closeouts.

- The vendor states fast approvals often within 48 hours and onboarding tailored to industry specifics.

- Automated chargeback management with Ethoca and Verifi, which the vendor claims can reduce chargebacks by up to 40% or more.

- Integrated hardware and online support: EMV and NFC terminals, mobile readers, self service kiosks, plus plugins and APIs for major eCommerce platforms.

- Recurring billing, card updater services, AI fraud scoring, 3D Secure 2.0, and compliance support including PCI DSS Level 1 and SOC 2.

Key Differentiator

Network Offset Pricing passing wholesale interchange to merchants with a transparent fixed margin. That single mechanism makes each transaction reflect its true cost instead of hiding interchange inside a blended percentage.

Pros

- The savings claim above gives merchants a concrete way to lower total processing spend compared with flat-rate billing, especially when card mix favors lower interchange.

- Dedicated accounts reduce aggregator exposure, which helps merchants in sensitive sectors avoid sudden holds or unexpected closures.

- Transparent pricing eliminates surprise line items and simplifies monthly reconciliation for finance teams.

- Industry-specific support for healthcare, restaurants, eCommerce, CBD, and other high risk sectors speeds compliance work and reduces manual overhead.

- Advanced fraud controls and the chargeback tooling mentioned above help reduce disputes and recoveries, improving net merchant revenue.

Cons

- Actual savings depend on transaction volume, card mix, and industry risk; results vary and must be modeled against your processing profile.

Notable Integrations

- QuickBooks

- Shopify

- Toast

- Square POS

- Xero

- Salesforce

- WooCommerce

- Clover

Who It's For

Merchants from small shops to enterprise sellers who want interchange transparency and lower effective rates. Especially relevant for high volume or high risk businesses that need dedicated accounts and compliance support such as healthcare practices, restaurants, subscription SaaS, eCommerce stores, and CBD retailers.

Unique Value Proposition

Passing wholesale interchange straight through with a fixed margin changes the economics of card acceptance. Instead of a blended flat fee that hides cost drivers, you get transaction-level pricing tied to card type and issuer, which makes margin forecasting more precise and gives finance teams levers to manage cost.

Real World Use Case

The vendor reports a 12-office dental group consolidated multiple merchant accounts into one and reduced its effective payment rate from 2.85% to 1.62%, while automating reconciliation and detailed transaction reporting. That example highlights both fee reduction and time saved on back office tasks.

Pricing

PaySec advertises typical savings of 30–60% versus flat-rate processors; exact costs vary by industry, card mix, and monthly volume. Pricing is delivered as custom quotes based on your processing profile, with no hidden fees and no long-term contracts.

Website: https://paysec.ai

Prahsys

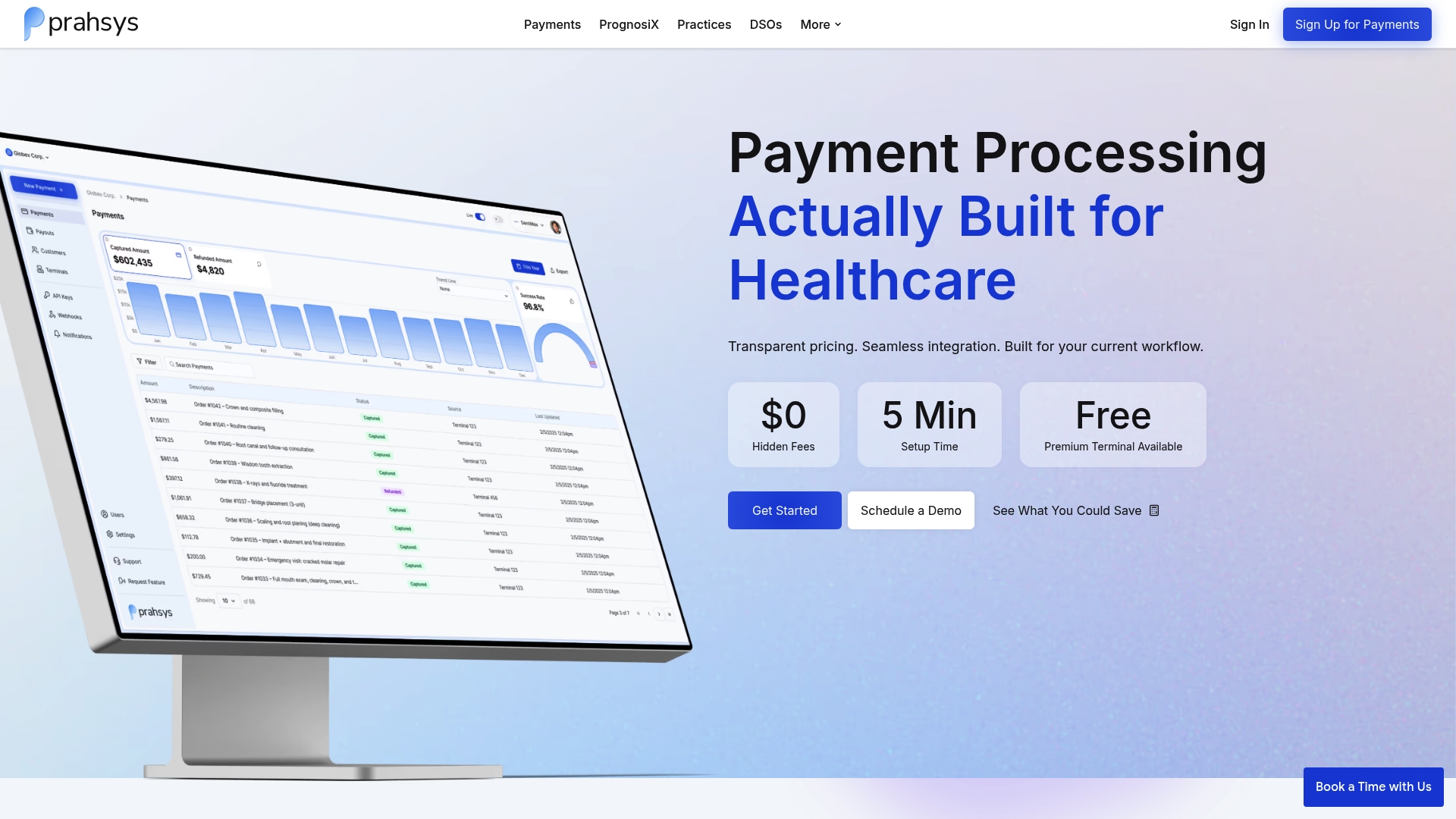

At a Glance

Prahsys' marketing materials advertise transparent merchant pricing with $0 hidden fees and a 2.49% + $0.49 per transaction rate, a clear selling point for cost-conscious practices. The vendor also claims a five minute setup and enterprise security posture including HIPAA, PCI DSS, and SOC2.

Prahsys pairs payment processing with AI-enhanced medical imaging aimed primarily at dental and dental-related practices. The combined offering targets clinics, multi-location DSOs, and practice management vendors that want embedded payments plus clinical imaging in one stack.

Short note. Very focused.

Core Features

- Integrated payment processing built for healthcare workflows, handling in-office and online payments.

- AI-enhanced DICOM imaging designed to support dental diagnostics without extra imaging hardware.

- Seamless API integration so software vendors and practices can embed payments and imaging into existing systems.

- Real-time payment monitoring and analytics for reconciliation and cashflow visibility.

- White-label payment solutions for partners wanting branded payment or imaging interfaces.

Key Differentiator

Prahsys emphasizes an API-first approach that combines AI imaging and payments without introducing additional hardware. That focus on embeddable APIs makes it practical for practice management platforms and DSOs to centralize transactions and imaging workflows inside their existing applications.

Pros

- The transparent pricing claim above removes surprise fees on paper, which simplifies cost forecasting for small and mid-size practices.

- The vendor advertises a five minute setup, a proposition that reduces technical overhead during rollout and shortens training time for front-desk staff.

- The platform advertises enterprise-grade security with HIPAA, PCI DSS, and SOC2 mentioned, which matters for clinical data and payment handling.

- Multi-channel payment support covers card-on-file, invoicing, and in-office terminals, letting practices consolidate receipts and reduce reconciliation work.

- Dedicated US-based premium support and onboarding assistance is listed, which helps practices that prefer hand-holding through implementation.

Cons

- No third-party reviews were located in the provided data, so independent user feedback and long-term usage reports are limited.

- The public record lacks community validation, which raises due-diligence time for risk-averse buyers who require references.

- Feature maturity for very large DSOs or high-volume hospitals is unclear from the vendor materials alone.

When It May Not Fit

If you require a vendor with a long trail of independent customer case studies or public reviews, Prahsys may not satisfy your procurement team. Organizations that mandate multiple independent attestations or long-term, peer-reviewed validation will want additional references.

Who It's For

Healthcare providers, dental practices, and practice management software companies that want a single supplier for payments and clinical imaging APIs. Especially suitable for DSOs and software partners planning branded, embedded payment flows.

Real World Use Case

A multi-location dental group embeds Prahsys APIs into its practice management portal. Patients pay online or at the chair, payments route into centralized reporting, and AI-enhanced DICOM images flow into the same patient record for quick clinician review.

Website: https://prahsys.com

Elevated Payments

At a Glance

The vendor advertises mobile payment acceptance starting at 0% processing for specific programs — a striking entry offer for merchants watching fee pressure. The company also advertises support for over 100 integrations, a claim that signals broad connector coverage for POS, CRM, and fraud tools.

Core Features

- Point of Sale support across many hardware vendors and terminal providers for in-person checkout.

- Mobile acceptance programs with promotional processing rates for qualifying merchants, plus desktop terminal support over ethernet or Wifi.

- E-commerce and MOTO transaction links to websites, invoicing, and CRM workflows for unified reconciliation.

- Fraud prevention with real-time data integrations and automation to flag risky transactions and reduce chargebacks.

- Self-order kiosks that reduce queue time and add an extra sales channel.

Key Differentiator

Elevated Payments positions itself as an all-in-one payments stack that emphasizes transparent pricing and broad integrations. That combination aims to reduce integration overhead for merchants who want a single vendor to handle in-store, mobile, and online rails without stitching multiple providers together.

Pros

- Fast processing and competitive exchange rates reported by users, which helps margin-sensitive retailers and online sellers.

- The dashboard is described as simple and intuitive, making daily reconciliation and terminal management less time consuming.

- Broad payment method coverage and the large integrations footprint make it easier to connect terminals to CRMs and fraud systems.

- Pricing options range from a free entry plan to specialized high-risk pricing, giving smaller merchants a lower barrier to test the platform.

Cons

- Several user reports mention inconsistent customer support responsiveness, which can lengthen resolution times for disputes or settlement questions.

- Some merchants reported missing or hard-to-trace funds, a serious operational issue that warrants careful contract and settlement monitoring.

- Onboarding complexity appears higher for certain accounts, with users describing a more involved signup than competitors advertise.

- A few packages reportedly lack advanced features, requiring add-ons or workarounds for specific workflows.

When It May Not Fit

If you need ironclad, fast-response support as part of the SLA, this platform may feel risky given reports on support variability. If your business cannot tolerate any settlement ambiguity, the anecdotal fund-tracing issues above are a red flag.

Notable Integrations

- NMI for gateway connectivity.

- Stripe and Authorize.net for merchant routing and tokenization.

- Konnektive CRM for customer and subscription workflows.

- Funnel and Chargebackhelp for reporting and dispute assistance.

Who It's For

Small to medium retail and online merchants that want a single payments partner covering POS, mobile, and e-commerce. The platform also targets high-risk verticals that need specialized pricing and fraud connectors rather than a basic off-the-shelf gateway.

Real World Use Case

A restaurant franchise deploys elevated POS terminals at multiple locations, ties online ordering into the same merchant account, and layers fraud rules to reduce chargebacks. The consolidated reporting cuts reconciliation time for the regional manager each week.

Pricing

Pricing varies by plan. The vendor lists a Free plan, a Cost Plus Pricing option at 1.99%, and a High Risk tier at 3.00%. Program terms and eligibility determine which rate applies.

Website: https://elevatedpayments.io

YapPay

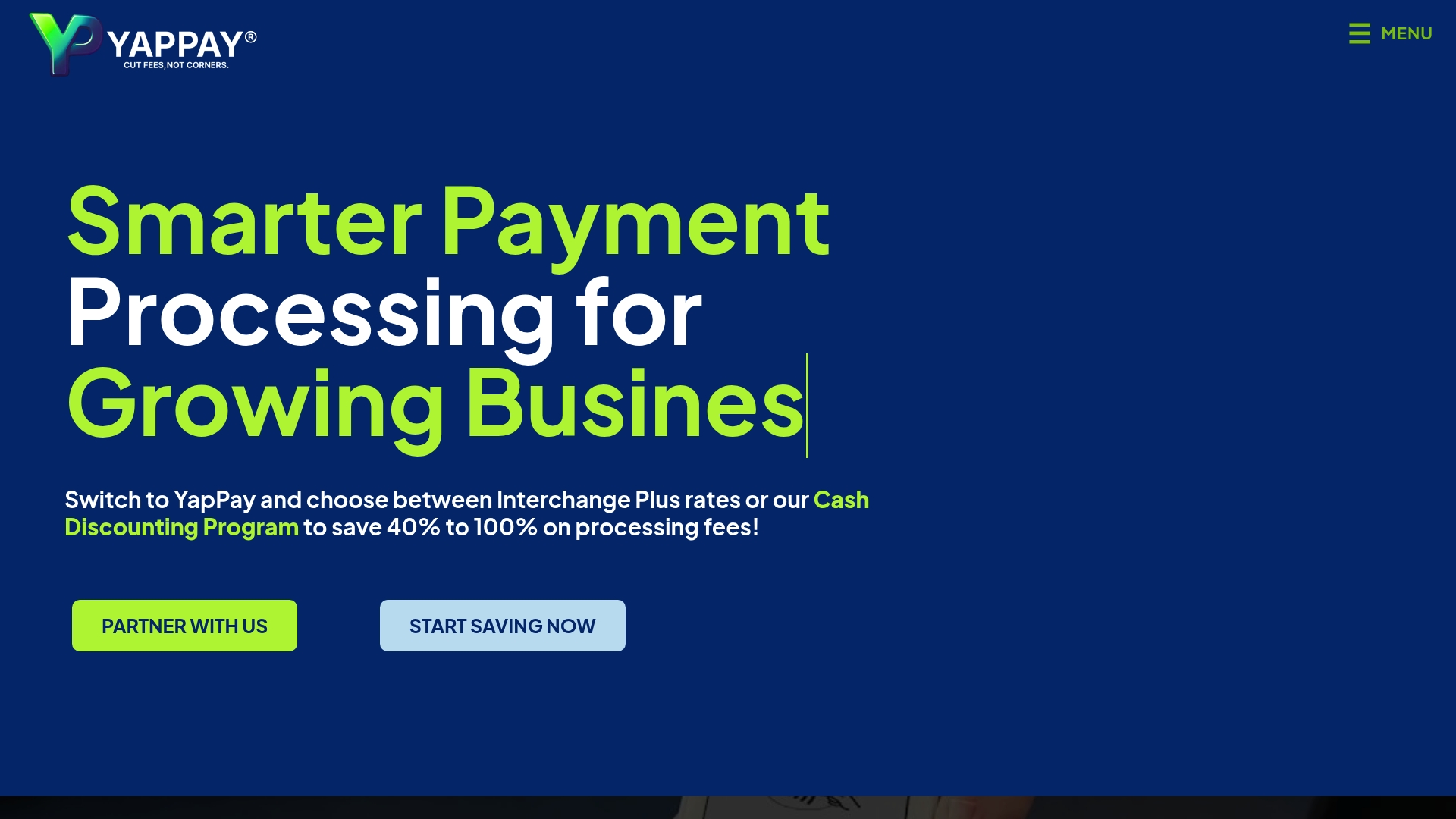

At a Glance

YapPay's marketing materials advertise a Cash Discounting Program that lets merchants retain 100% of on-paper profits by shifting processing costs to customers. The vendor also highlights flexible Interchange Plus pricing and claims approvals can happen in as little as one hour.

Core Features

- Interchange Plus pricing and a Cash Discounting option that target lower net costs for merchants.

- The vendor advertises fast onboarding with approval as quick as one hour, and reports quick funding for settled batches.

- Real-time transaction tracking, analytics, and enterprise-grade security with PCI-focused controls and fraud monitoring.

- Hardware and software connectivity that supports POS and SaaS integrations for stores, restaurants, and e-commerce.

Key Differentiator

YapPay positions its payment rails as enterprise-grade while keeping options for smaller merchants. The key angle is that merchants can pick a transparent Interchange Plus model or adopt the cash discount setup to change how fees appear on the books while staying on the same core platform.

Pros

- User-friendly backend management with responsive support. Users report faster issue resolution compared with legacy providers.

- Creates professional, customizable mobile and POS applications so your checkout matches your brand and workflows.

- Flexible payment programs that can materially reduce processing costs when configured correctly, especially for higher-volume card categories.

- Fast approval process and quicker access to funds relative to many traditional ISOs based on the vendor's messaging.

- Strong security posture. The transaction monitoring and encryption features reduce fraud surface area for merchants that handle sensitive card data.

Cons

- Manual data entry shows up at lower tiers which can be tedious for businesses that batch-upload many sessions or reconciliations.

- The interface has a learning curve for some users and may require training for staff unfamiliar with modern terminal dashboards.

- Lower tier accounts have limited data import features which forces manual work during initial migrations.

When It May Not Fit

If your team needs a fully automated import pipeline out of the gate, YapPay's lower tiers will slow you down. Teams without a staff member who can field basic terminal setup or data clean-up will spend time on manual entry during onboarding.

Notable Integrations

The vendor reports integrations with over 450 gateways, POS systems, and CRMs including GoHighLevel. That breadth helps if you run a mix of in-person and online channels and want to avoid swapping POS vendors.

Who It's For

Small to medium-sized retailers, restaurants, and service businesses that want transparent pricing options and the ability to switch between Interchange Plus and cash discounting without changing providers.

Real World Use Case

A mid-sized retail shop moves from a flat-rate processor to YapPay's Interchange Plus plan. They integrate the existing POS, use the reporting to isolate high-fee card types, and cut net processing spend while keeping settlement timelines similar to their prior provider.

Pricing

Pricing varies by program. The vendor lists Interchange Plus around 2.40% plus $0.20 per transaction as an example. The Cash Discounting option is advertised as a no-processing-fee model where customers cover the card fees and hardware is included.

Website: https://yappay.app

Hyperswitch

At a Glance

The vendor advertises a 99.999% uptime SLA and supports both on-premises deployment and a fully managed cloud offering. Hyperswitch pairs that availability claim with an open-source modular stack covering routing, reconciliation, vault, and revenue recovery modules. Evaluate its modules against your processor roster to see where control and cost savings appear.

Core Features

Modular, production-ready components let engineering teams pick only what they need and extend the stack where required.

- Payment routing that lets you orchestrate multiple processors and apply custom cost rules.

- Reconciliation module to automate ledger matching and reduce manual exceptions.

- Vault for hosted credential storage and tokenization alongside revenue recovery features.

- Deployable on-premises or via a hosted cloud service to meet regional and compliance needs.

Map these modules to a two week proof of concept before committing to a full rollout.

Key Differentiator

Hyperswitch’s defining trait is its combination of open-source code and a truly modular architecture. That design hands engineering teams full control to replace or extend components without being locked to a single vendor. Run a short integration sprint to validate how easily your internal systems can call its APIs.

Pros

-

Flexible architecture lets you swap processors and local acquiring partners without rewriting business logic. Teams that manage multi-region routing will find this useful.

-

Open-source transparency reduces vendor blind spots and allows internal security reviews and audits.

-

Supports a wide set of payment methods and processors, which helps enterprises consolidating fragmented payment flows.

-

High availability is part of the vendor claims, and that uptime figure above matters for transaction critical paths and settlement reliability.

-

The vendor reports adoption by large, established companies, which suggests the platform has been used in regulated enterprise contexts.

Each pro above should be validated with a short technical trial and a security review.

Cons

-

There are no substantive third-party user reviews available, so community-sourced strengths and weaknesses are not documented.

-

Deployment and customization can be complex and will likely require senior engineering and DevOps resources for configuration, scaling, and monitoring.

-

Pricing is tailored and not transparent up front, which means you will need direct vendor contact to get a scoped quote and SLA commitments.

-

The modular approach reduces vendor lock in but increases the integration surface and internal maintenance burden.

Plan for at least one month of internal technical evaluation before a production decision.

When It May Not Fit

If your business lacks dedicated engineering or DevOps capacity, Hyperswitch will add operational burden and cost. If you need a plug-and-play, hosted processor with fixed transaction fees and a self-serve sign up, this product is not the right match. Also avoid it if transparent, list-priced billing is a procurement requirement for your vendor policy.

Who It's For

Enterprises, fintechs, banks, airlines, and large SaaS companies that want to build or operate a highly customizable payments stack and control routing, reconciliation, and data residency. Ideal where in-house engineering teams can own deployment and maintenance.

Real World Use Case

A large fintech deployed Hyperswitch on-premises to unify reconciliation and implement region-specific routing logic. Using the modules above, the team automated exception handling and reduced manual settlement work. Test that same flow in a pilot to measure error reduction and reconciliation time.

Pricing

Pricing is customized with self-hosted community and enterprise editions plus a fully hosted cloud service. The vendor provides specific costs on request, typically after scoping deployment and support needs. Request a detailed statement of work and a quote that includes expected support and upgrade windows.

Website: https://hyperswitch.io

Comparative Analysis of Payment Processing Platforms

Choosing the ideal payment processing platform depends on specific business needs, including pricing transparency, industry compatibility, and technical capabilities. The platforms reviewed here provide unique advantages, catering to diverse operational requirements, but distinct tradeoffs exist.

Comparison of Pricing Strategies and Cost Efficiency

PaySec offers a Network Offset Pricing model that emphasizes transparency by passing wholesale rates directly to merchants with a fixed margin. This contrasts Prahsys' fixed-percentage pricing of 2.49% per transaction, which simplifies cost forecasting for smaller businesses but may not provide cost efficiency as transaction volumes scale. Elevated Payments provides adaptable pricing options, including a cost-plus model for high-risk merchants, giving flexibility but requiring detailed analysis to ensure accurate cost management.

Technical Customization and Integration Breadth

Hyperswitch stands out with its modular and open-source architecture, facilitating extensive customization and integration capabilities for enterprise-grade businesses with in-house technical resources. For small to medium-sized service retailers, YapPay’s extensive integration support and customizable applications ensure effective compatibility with existing systems, proving advantageous for businesses with limited technical teams. In comparison, PaySec’s compatibility with existing major platforms offers a balanced solution for firms seeking ready-to-use integrations without overhauling infrastructure.

Best Fit Recommendations

- PaySec: Best for merchants prioritizing cost efficiency via transparent pricing structures, particularly those operating in high-risk environments requiring advanced compliance features.

- Prahsys: Ideal for healthcare and dental clinics needing payment integration alongside medical imaging solutions without the need for additional hardware investments.

- Elevated Payments: Suitable for small retailers and restaurants requiring affordable, straightforward payment solutions with broad integration options and low initial costs.

- Hyperswitch: Recommended for enterprises with strong in-house technical support requiring highly customizable routing, reconciliation, and data residency controls.

Our Pick: PaySec

PaySec distinguishes itself by offering a unique pricing mechanism, especially beneficial for high-volume or high-risk businesses, providing clear interchange transparency with flexible merchant account setup. However, for scenarios requiring in-house customization with modular API components, Hyperswitch may be a more fitting solution.

Payment Processing Platforms Comparison

Here is a comparison of payment processing platforms, highlighting their core offerings and unique differentiators to assist buyers in selecting the most suitable solution.

| Product Name | Core Feature | Key Differentiator | Best For | Pricing | Notable Limitation |

|---|---|---|---|---|---|

| Paysec | Network Offset Pricing for reduced rates | Transparent interchange pass-through | High-volume businesses or high-risk sectors | Not disclosed | Savings depend on transaction profile |

| Prahsys | Payment processing with AI-enhanced imaging | Combines payments with dental imaging | Dental and healthcare practices | 2.49% + $0.49 per transaction | Limited third-party reviews |

| Elevated Payments | POS and mobile payment processing | All-in-one payments stack | Small to mid-size retail and online merchants | Plans from Free to 3.00% | Reports of inconsistent customer support |

| YapPay | Cash Discounting and Interchange Plus pricing | Flexible fee models | Small to medium-sized retailers and restaurants | 2.40% + $0.20 per transaction (example) | Manual data entry at lower tiers |

| Hyperswitch | Modular open-source payment stack | Highly customizable architecture | Enterprises with in-house development teams | Pricing on request | Requires significant engineering resources |

Discover Transparent Payment Processing with Paysec

If you are exploring fintech5group.com alternatives to reduce payment processing costs and gain clearer financial insights, Paysec is a solution designed to cut your transaction fees by 30 to 60 percent while eliminating hidden charges. Paysec’s Network Offset Pricing passes wholesale interchange rates with a fixed margin, empowering businesses in SaaS, healthcare, restaurants, and eCommerce to take full control of their payment expenses.

Gain measurable savings and financial transparency by switching to Paysec today. Visit Paysec to see how detailed transaction reporting and compliance support can simplify your reconciliation and lower your overall costs. Take action now and receive custom pricing tailored to your business needs with no long-term contracts or surprises.

Frequently Asked Questions

How does Paysec's Network Offset Pricing benefit merchants?

Paysec's Network Offset Pricing allows merchants to pay wholesale interchange rates with a transparent fixed margin, which can reduce overall payment processing costs by 30–60% compared to flat-rate processors. This feature directly benefits businesses that handle a mix of card types and want clear pricing without hidden fees. Merchants can expect lower effective rates, making it easier to manage their payment processing expenses.

What is the primary strength of Prahsys when compared to Paysec?

Prahsys offers an integrated payment processing solution specifically designed for healthcare workflows, which can be particularly beneficial for dental practices needing AI-enhanced imaging alongside payments. While Paysec excels in providing transparency in interchange pricing, Prahsys’s focus on seamless integration into clinical settings makes it suitable for healthcare providers looking for combined payment and imaging solutions.

Does Elevated Payments provide more integrations than Paysec?

Elevated Payments boasts support for over 100 integrations across various platforms, making it a suitable choice for merchants looking for extensive connectivity with POS, CRM, and fraud tools. Paysec also offers integrations but focuses more on transparency in pricing and dedicated merchant accounts, which help reduce exposure for high-risk industries. Merchants should consider their specific integration needs when choosing between the two.

Can I use YapPay's Cash Discounting feature if I'm already using another processor?

YapPay's Cash Discounting program enables merchants to retain 100% of their profits by passing processing costs to customers, which could be attractive for retailers looking to lower their bottom line. While transitioning from another processor may require careful planning, businesses can easily explore YapPay as a cost-effective alternative for payment processing. Paysec, with its interchange transparency, may also be a worthy consideration for similar savings.

How fast can I get started with Paysec compared to Hyperswitch?

Paysec promises quick onboarding, often completed within 48 hours, allowing merchants to start processing payments swiftly. In contrast, Hyperswitch requires a more technical setup and evaluation period, which might extend the onboarding time for businesses that lack dedicated resources. Merchants looking for an immediate start should take Paysec's expedited process into account.