TL;DR:

- CBD retailers rely on specialized high-risk payment processors like PaymentCloud and DozyPay that have dedicated acquiring banks to ensure payment stability and compliance. Non-compliant product labeling, website claims, and state restrictions can lead to account termination or frozen funds, making thorough compliance review essential. Choosing a processor based on bank stability, transparent pricing, and active monitoring offers more lasting and cost-effective payment solutions.

CBD retail payment processor options are specialized merchant services built to handle cannabis industry transactions with compliance controls, acquiring bank stability, and fee structures that general processors refuse to offer. Standard platforms like Stripe, Square, and PayPal prohibit CBD product sales in their terms of service, which forces CBD retailers into a separate category of high-risk payment solutions. Processors like PaymentCloud, DozyPay, and Paysec fill that gap by pairing dedicated acquiring banks with underwriting expertise specific to hemp and CBD commerce. Getting this choice right determines whether your store processes payments reliably or faces sudden account terminations and frozen funds.

What compliance requirements must CBD retailers understand for payment processing?

CBD retail compliance requirements for payment processing go well beyond simply selling a legal product. The 2018 Farm Bill federally legalized hemp-derived CBD with less than 0.3% THC, but acquiring banks and card networks still classify CBD merchants as high-risk. That classification triggers a separate underwriting process with stricter documentation, ongoing monitoring, and product review requirements.

Acquiring banks play the central role in this process. They are the financial institutions that actually hold your merchant account and assume liability for your transactions. Their commitment to CBD portfolios determines whether your account stays open during a policy shift or gets terminated with 24 hours notice. A processor with a gateway but no dedicated CBD acquiring bank is a liability, not a solution.

CBD retailers must meet several compliance requirements before and during merchant account approval:

- Product labeling accuracy: Labels must reflect actual CBD content, avoid unapproved health claims, and comply with FDA guidance on dietary supplements.

- Website content review: Product pages cannot make disease treatment claims. Processors like DozyPay offer pre-submission compliance checks on product pages to improve approval odds.

- State-level restrictions: Some states impose additional licensing or sales restrictions on CBD products. Your processor's underwriting team must understand the states you sell into.

- Age verification: Many acquiring banks require age gates on CBD retail websites as a condition of approval.

- Chargeback thresholds: Card networks set chargeback ratio limits. CBD merchants who exceed those limits risk account termination regardless of product legality.

Non-compliance at any of these points can result in account holds, fund reserves, or permanent termination. The consequences are not theoretical. CBD retailers who launch without a compliance review frequently face rejection during underwriting or mid-operation shutdowns.

Pro Tip: Before applying for a merchant account, audit every product page for health claims. Remove phrases like "treats anxiety" or "cures inflammation" and replace them with factual descriptions of ingredients and suggested use.

What payment processor options are available to CBD retailers?

CBD retailers have four main categories of payment solutions to evaluate. Each carries different tradeoffs on stability, cost, approval speed, and customer support.

High-risk specialized processors

High-risk processors built for CBD are the most reliable starting point. PaymentCloud publicly supports CBD merchants with underwriting expertise and transparent fee structures. DozyPay maintains acquiring banks dedicated specifically to CBD portfolios, which reduces the risk of abrupt account closures. PayKings operates similarly, with underwriting teams experienced in hemp and cannabis merchant categories. These processors understand the product types, the compliance landscape, and the chargeback patterns specific to CBD retail.

Aggregator gateways with CBD restrictions

General payment aggregators pool merchants into shared accounts. Stripe, Square, and PayPal all prohibit CBD in their terms of service. Their shared acquiring relationships cannot accommodate the risk profile of CBD sales. Retailers who attempt to process CBD through these platforms risk permanent account bans and fund holds without warning. This is not a gray area. Their terms are explicit.

ACH, eCheck, and bank transfer processors

ACH and eCheck transactions offer lower fees and reduced chargeback exposure, making them well-suited for repeat customers and wholesale CBD buyers. Bank account integration tools like Plaid and Dwolla provide alternative payment rails that bypass card network restrictions entirely. The tradeoff is slower settlement and a checkout experience that some retail customers find less convenient than card payments.

Cryptocurrency processors

Crypto payment processors accept Bitcoin and stablecoins as payment for CBD products. This option eliminates card network restrictions but introduces volatility risk and a limited customer base. Adoption is growing in CBD retail, but crypto remains a supplementary channel rather than a primary one for most stores.

POS systems with integrated payments

Point-of-sale systems like Flowhub, Green Bits, and BioTrackTHC combine compliance tracking with payment processing in a single platform. These systems offer seed-to-sale inventory tracking alongside compliant payment acceptance. They are particularly useful for CBD dispensaries that also handle hemp flower or other regulated products.

| Processor type | Stability | Fees | Approval speed | Best for |

|---|---|---|---|---|

| High-risk specialists | High | Moderate to high | 3–7 days | Most CBD retailers |

| ACH/eCheck | High | Low | 1–3 days | Wholesale, repeat buyers |

| Crypto processors | Variable | Low | Fast | Tech-forward retailers |

| POS-integrated systems | High | Bundled | 5–10 days | Dispensaries, multi-location |

| General aggregators | None | Low | Instant | Not available for CBD |

Pro Tip: Run ACH as a secondary payment option alongside card processing. Offering both reduces your dependence on any single payment rail and lowers your average transaction cost for high-volume orders.

How to evaluate and select the best payment processor for your CBD retail business

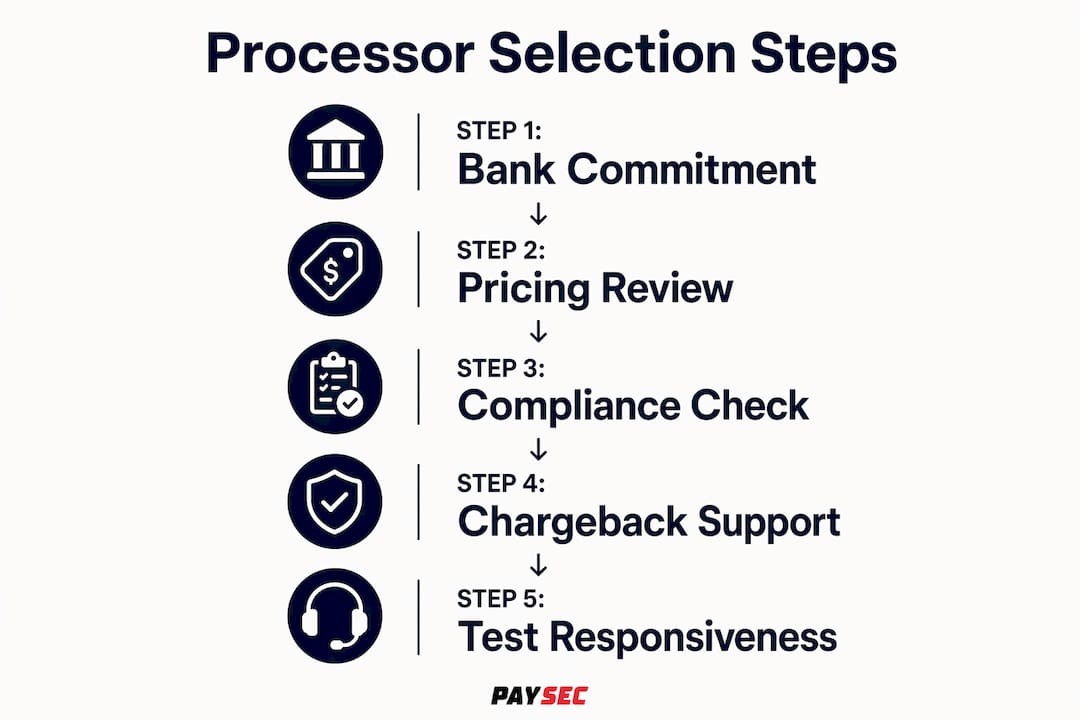

Selecting the best payment processor for CBD retailers requires evaluating five specific criteria. Gateway features matter, but the acquiring bank relationship is the single most important factor in long-term account stability.

1. Confirm the acquiring bank's CBD commitment

Ask every processor directly: which acquiring bank holds your CBD merchant accounts? A processor that cannot name a specific bank or describes a "network of banks" is likely routing your account through a general high-risk pool. Retail CBD payment stability depends on the acquiring bank's long-term commitment to CBD portfolios, not just the gateway technology sitting in front of it.

2. Understand the full pricing structure

CBD merchant accounts carry higher fees than standard retail accounts. Expect interchange-plus pricing, monthly account fees, and sometimes a rolling reserve. A rolling reserve holds back a percentage of your revenue, typically for 90–180 days, as a risk buffer. Processors that explain pricing before signup and disclose all fees upfront are the ones worth pursuing. Hidden fees in CBD processing are common and costly.

3. Evaluate gateway features that matter for CBD retail

The gateway is the software layer that connects your store to the acquiring bank. Key features to verify include:

- Fraud screening tools that flag suspicious orders before they become chargebacks

- Recurring billing support for subscription CBD products

- Integration with your existing eCommerce platform, whether Shopify, WooCommerce, or a custom build

- Tokenization for storing customer payment data securely

4. Review chargeback management support

CBD products generate above-average chargeback rates because customers sometimes dispute charges when they are dissatisfied with results. Processors that offer chargeback alerts, dispute management tools, and dedicated support contacts give you a real advantage. Ask whether the processor provides chargeback representment assistance or simply notifies you of disputes.

5. Test support responsiveness before committing

Call the processor's support line before you sign anything. Ask a technical question about their CBD underwriting process. The quality of that conversation tells you exactly what you will get when a real problem occurs. The best CBD merchant services provide ongoing support, not just account approval.

How to integrate and set up payment processing in your CBD retail store

Setting up payment processing for a CBD store follows a specific sequence. Skipping steps in this process is the most common reason applications get rejected or accounts get terminated early.

-

Audit your website and product listings first. Remove any health claims from product descriptions. Verify that your terms of service, refund policy, and privacy policy are published and current. Processors review these pages during underwriting.

-

Gather your business documentation. You will need your EIN, business license, three to six months of bank statements, a voided check, and a processing history report if you have one. CBD processors require more documentation than standard merchant account applications.

-

Select a compatible POS and gateway. If you operate a physical store, confirm that your chosen processor supports your POS hardware. Systems like Flowhub and Green Bits integrate directly with CBD-specific acquiring relationships. For eCommerce, verify gateway compatibility with your platform before applying.

-

Submit your application with a compliance review. Some processors, including DozyPay, conduct pre-submission reviews of your product pages. Use that service. A clean application with compliant product listings moves through underwriting faster and with fewer conditions.

-

Configure recurring billing and chargeback controls. Once approved, set up clear subscription terms with visible cancellation policies. Ambiguous subscription language is the leading cause of CBD chargebacks. Enable chargeback alerts through your processor or a third-party service like Ethoca or Verifi.

-

Test transactions before going live. Run test transactions across all payment methods you plan to offer. Verify that receipts, confirmation emails, and refund flows work correctly. A failed refund process is a chargeback waiting to happen.

Pro Tip: Keep a dedicated folder with all your compliance documentation, product certificates of analysis, and processor correspondence. When your acquiring bank conducts a portfolio review, having this ready shortens the review period significantly.

What best practices keep CBD payment processing stable and affordable?

Long-term payment stability in CBD retail requires active management, not a set-and-forget approach. Processors change acquiring bank relationships, card networks update rules, and state regulations shift. Retailers who monitor these changes stay ahead of account disruptions.

The following practices protect your processing stability and reduce costs:

- Monitor your chargeback ratio monthly. Card networks flag accounts that exceed a 1% chargeback ratio. Track your ratio and investigate any spike immediately. A sudden increase in disputes often signals a product quality issue or a confusing billing descriptor.

- Use ACH for high-value repeat orders. Wholesale orders and subscription renewals processed via ACH carry lower fees and almost no chargeback risk. This is a direct cost reduction that compounds over time.

- Keep your processor informed of product changes. Adding new product categories, especially anything that could be classified differently by your acquiring bank, requires notification. Processors that discover undisclosed product changes during a portfolio review may suspend your account.

- Review your contract annually. Fee structures in CBD processing change. Processors renegotiate acquiring bank terms, and those changes sometimes flow through to merchant accounts. An annual contract review catches fee increases before they become significant.

- Maintain a backup processing relationship. CBD merchants who rely on a single processor are vulnerable to sudden account disruptions. A secondary processor, even one used only for ACH or as a failover, protects your revenue continuity.

"The acquiring bank relationship is the foundation of CBD payment stability. Everything else, the gateway, the POS, the fee structure, sits on top of that foundation. Build it right first."

The real lesson CBD retailers learn about processor selection

Most CBD retailers focus on fees when choosing a processor. That instinct is understandable but misplaced. Fees matter, but they are secondary to account stability. A processor charging 0.5% less per transaction is not a better deal if your account gets terminated in month four because their acquiring bank exited the CBD space.

At Paysec, we have seen this pattern repeatedly. A retailer signs with a lower-cost processor, processes for a few months, then faces a sudden account hold or termination. The cost of that disruption, lost sales, customer trust damage, and the time spent reapplying, far exceeds any fee savings. The acquiring bank's commitment to CBD portfolios is the variable that determines whether your processing relationship lasts.

The other pattern worth noting is the underuse of ACH. CBD retailers who add ACH as a payment option for repeat customers consistently reduce their processing costs without sacrificing conversion. The checkout experience is slightly different, but customers who buy CBD regularly are motivated buyers. They complete ACH transactions at high rates.

Crypto adoption in CBD retail is growing, but it remains a niche channel in 2026. The retailers gaining the most from crypto are those using it as a supplementary option for specific customer segments, not as a replacement for card processing. The volatility and conversion friction still limit its role as a primary payment method.

For retailers new to the high-risk processing space, the high-risk merchant account guide is worth reading before you start your processor search. Understanding the mechanics of high-risk underwriting changes the questions you ask and the processors you shortlist.

— PaySec Marketing Team

Paysec offers CBD retailers a stable, transparent processing solution

CBD retailers who have been declined, terminated, or overcharged by other processors have a direct path forward with Paysec.

Paysec works with CBD merchants across physical retail and eCommerce, pairing dedicated acquiring bank relationships with Network Offset Pricing that cuts processing costs by 30–60%. There are no hidden fees, no minimums, and no long-term contracts. Paysec's merchant services for CBD include full compliance support, detailed transaction reporting, and payment terminal options for in-store operations. Retailers who want to see exactly what they pay before they commit can review the full pricing structure and compare it against their current processor. The numbers speak for themselves.

Key takeaways

CBD retailers who select a processor based on acquiring bank stability, transparent pricing, and compliance support build payment operations that last.

| Point | Details |

|---|---|

| Acquiring bank stability is primary | Choose processors with dedicated CBD acquiring banks to prevent sudden account terminations. |

| General processors do not work for CBD | Stripe, Square, and PayPal prohibit CBD sales; specialized processors are required. |

| ACH reduces costs and chargeback risk | Use ACH for repeat and wholesale orders to lower fees and protect your chargeback ratio. |

| Compliance review before applying | Audit product pages and remove health claims before submitting any merchant account application. |

| Active monitoring protects your account | Review chargeback ratios monthly and notify your processor of any product category changes. |

FAQ

What are CBD retail payment processor options?

CBD retail payment processor options are specialized merchant services that support hemp and CBD product sales, including high-risk processors like PaymentCloud and DozyPay, ACH providers, and POS-integrated systems like Flowhub. General platforms like Stripe and Square prohibit CBD transactions entirely.

Why do CBD retailers need a specialized payment processor?

CBD is classified as high-risk by acquiring banks and card networks, which means standard processors will not approve or will terminate CBD merchant accounts. Specialized processors maintain dedicated acquiring bank relationships that support CBD portfolios long-term.

How long does CBD merchant account approval take?

Approval timelines vary by processor, but most high-risk CBD merchant accounts take 3–7 business days with complete documentation. Pre-submission compliance reviews of product pages can shorten that timeline by reducing underwriting questions.

What is a rolling reserve in CBD payment processing?

A rolling reserve is a percentage of your transaction revenue held by the acquiring bank as a risk buffer, typically released after 90–180 days. Many CBD processors require rolling reserves during the first year of processing as a condition of account approval.

How can CBD retailers reduce payment processing fees?

Adding ACH as a payment option for repeat and wholesale customers is the most direct way to reduce fees, since ACH transactions carry lower rates than card payments. Processors that offer interchange-plus pricing with transparent markups also produce lower long-term costs than flat-rate or tiered pricing models.