TL;DR:

- API payment integration connects your application directly to a payment gateway, enabling secure, automated transactions without redirecting users. It involves creating accounts, generating API keys, and embedding code to process payments, with a typical flow from card data capture to settlement taking 1 to 3 days, while security features like tokenization and 3DS2 protect sensitive information. Selecting the right provider depends on cost structure, supported methods, integration support, and robust reporting; best practices include thorough testing, secure key management, and webhook setup for real-time updates.

API payment integration is the process of connecting your business systems directly to a payment gateway through software interfaces, enabling secure, automated transaction processing without redirecting customers away from your site or app. Providers like Stripe, Square, and Paysec expose these interfaces so developers can embed checkout flows, trigger charges, issue refunds, and pull transaction data programmatically. Setup follows four core steps: account creation, API key generation, embedding the integration code, and running test transactions before going live. Understanding what is api payment integration gives you the foundation to choose the right provider, build a better checkout experience, and cut unnecessary processing costs from day one.

What is API payment integration and how does it work?

API payment integration is the technical bridge between your application and the global payment network. An API, or Application Programming Interface, is a set of rules that lets two software systems communicate. In the payments context, your website or app sends a request to a payment provider's API, which then routes that request through card networks like Visa or Mastercard, communicates with the issuing bank, and returns an authorization response.

The payment gateway sits at the center of this flow. A payment gateway is a software intermediary that securely processes card payments between the customer, merchant, and banking network, delivering authorization in under 2 seconds. That speed matters because checkout abandonment spikes when payment confirmation takes longer than a few seconds.

Integration options range from pre-built checkout forms to fully custom API calls. Embedding payment code into websites can be done via checkout forms, SDKs, or direct API calls for customized payment experiences. A pre-built SDK like Stripe Elements or Square Web Payments SDK gets you running in hours. A fully custom direct API integration gives you complete control over the UI and data flow, but requires more development time.

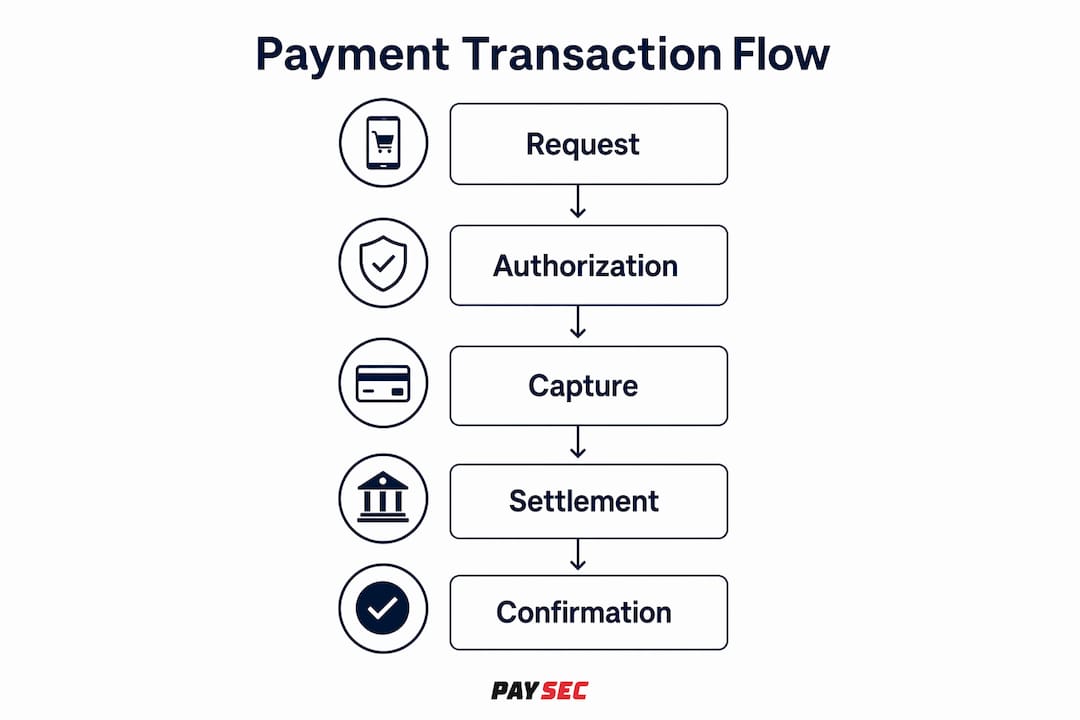

How does the full transaction flow work step by step?

Understanding the payment lifecycle prevents costly mistakes in production. Here is the complete flow from card entry to funds in your account.

- Card data capture. The customer enters card details into your checkout form. If you use a JavaScript SDK, the card data never touches your server. The SDK tokenizes it client-side and sends a secure token to the payment provider.

- Authorization request. Your server sends an API call to the payment gateway with the token and transaction amount. The gateway forwards the request to the card network, which contacts the issuing bank.

- Authorization response. The issuing bank approves or declines the transaction. Authorization under 2 seconds is the standard for card-not-present API transactions. Your API response contains an authorization code, which you store against the order.

- Capture. Authorization only reserves funds. Actual money transfer happens via a batch settlement process, typically overnight. You capture the authorized amount either immediately or later, depending on your fulfillment model.

- Settlement. Settlement of funds after API authorization takes between 1 and 3 business days depending on the card network and bank relationships. That means an authorization on Monday may not deposit until Wednesday.

- Reconciliation. Your system matches settled amounts against authorized amounts. Discrepancies here are the most common source of accounting errors in API-integrated businesses.

Pro Tip: Always store both the authorization ID and the capture ID separately in your database. When a dispute arises, you need both references to trace the full transaction lifecycle with your payment provider.

The authorization vs. settlement distinction

This is the single most misunderstood concept in API payment integration. Authorization status returned by payment APIs only reserves funds. The actual transfer occurs later via batch settlement, which causes reconciliation confusion if not tracked properly. Many developers mark an order as "paid" on authorization and never reconcile against the settled amount. That gap creates accounting errors, especially when partial captures or refunds are involved.

Security features built into payment apis

Tokenization and 3DS2 authentication are the two security pillars of modern payment API integration. Tokenization replaces raw card data with a non-sensitive token, so even if your database is breached, no usable card data is exposed. 3DS2 adds a real-time authentication layer where the issuing bank verifies the cardholder's identity, reducing fraud liability and meeting Strong Customer Authentication requirements in regulated markets.

| Security Feature | What It Does | Who Benefits |

|---|---|---|

| Tokenization | Replaces card data with a secure token | Merchants, reduces PCI scope |

| 3DS2 Authentication | Verifies cardholder identity in real time | Issuers, merchants, cardholders |

| Idempotency Keys | Prevents duplicate charges on retried requests | Developers, customers |

| TLS Encryption | Encrypts data in transit between systems | All parties |

Every API call that creates or modifies a transaction requires an idempotency key to prevent duplicate charges in case of network retries. This is non-negotiable in production environments where network timeouts are common.

What are the key benefits of API payment integration for businesses?

API integration for payments delivers advantages that go well beyond simply accepting cards online. The benefits split into four categories: speed, experience, security, and flexibility.

Speed and automation. Manual payment processing requires staff to enter transaction data, reconcile records, and chase failed payments. API-driven payments automate all three. Real-time transaction feedback from payment APIs enables faster issue resolution and reconciliation, which directly improves cash flow management. A SaaS company processing 10,000 monthly subscriptions cannot afford manual billing. API automation makes that volume manageable without adding headcount.

Checkout experience. Embedded payment forms keep customers on your domain throughout the purchase. Redirecting to a third-party page breaks trust and increases abandonment. With a payment gateway API, you control the look, feel, and flow of the entire checkout. That control translates to higher conversion rates, especially on mobile.

Multi-method and multi-currency support. Modern payment APIs support credit and debit cards, digital wallets, and bank transfers with multi-currency capability. A single API integration can accept Visa, Mastercard, Apple Pay, Google Pay, and ACH bank transfers without separate technical setups for each method. For businesses selling internationally, multi-currency support through a single API connection is a significant operational advantage. You can read more about cross-border payment infrastructure to understand how API layers handle global compliance.

Security and fraud prevention. Because the payment provider handles PCI DSS compliance on their infrastructure, your compliance scope shrinks dramatically. You are not storing card data. You are not processing raw card numbers. The API provider absorbs the heaviest security obligations.

Pro Tip: Enable webhook notifications from your payment provider for every event type: charge.succeeded, charge.failed, refund.created, and dispute.created. Webhooks give you real-time visibility without polling the API, and they are the fastest way to catch fraud patterns early.

How do payment API providers compare for your business?

Provider selection requires assessing pricing, developer tools, and integration support because fees, features, and ecosystem depth vary significantly across platforms. The wrong choice costs you in processing fees, developer hours, or both.

Here is a direct comparison of leading payment API solutions:

| Provider | Standard Card Rate | Key Strength | Best For |

|---|---|---|---|

| Stripe | 2.9% + $0.30 per transaction | Developer tools, global reach | Tech-forward businesses, SaaS |

| Square | 2.6% + $0.10 (in-person) | Hardware and software bundle | Retail, restaurants |

| Paysec | Network Offset Pricing (30–60% savings) | Pricing transparency, no hidden fees | SMBs across 18+ industries |

| PayPal | 3.49% + $0.49 (advanced checkout) | Brand recognition, buyer trust | Consumer-facing eCommerce |

Paysec's Network Offset Pricing model stands apart from standard percentage-based fees. Rather than charging a flat rate on every transaction, Paysec passes wholesale interchange rates to merchants, which produces savings of 30–60% compared to standard processing fees. Merchants in sectors like healthcare, SaaS, and CBD retail have reported a 42% reduction in processing costs after switching. There are no minimums and no long-term contracts, which removes the risk of locking into a provider before you know it fits.

When evaluating any payment API provider, weigh these factors:

- Pricing model. Flat-rate pricing is predictable but expensive at scale. Interchange-plus or offset pricing rewards higher volume.

- Developer documentation. Stripe's documentation is the industry benchmark. Any provider you consider should offer sandbox environments, code samples in multiple languages, and a responsive developer support channel.

- Supported payment methods. Confirm the provider supports every method your customers use, including digital wallets and ACH if relevant.

- Ecosystem integrations. Does the API connect natively to your eCommerce platform, CRM, or accounting software? Native integrations save weeks of custom development.

- Reporting and analytics. Detailed transaction reporting helps you spot trends, manage chargebacks, and satisfy auditors. Paysec provides granular transaction reporting that supports financial transparency and compliance.

For businesses that operate across multiple countries, business payment account access for international companies is a separate consideration that affects which payment API providers are even available to you.

What are the best practices for implementing payment API integration?

A successful API payment integration follows a structured process. Skipping steps here is the primary cause of production failures, duplicate charges, and compliance gaps.

- Create your provider account and complete verification. Payment providers require business verification before granting live API keys. Submit your business documents early. Verification can take 1–3 business days depending on the provider.

- Generate and secure your API keys. You receive a test key and a live key. Store live keys in environment variables or a secrets manager like AWS Secrets Manager or HashiCorp Vault. Never hardcode keys in source code or commit them to version control.

- Choose your integration method. Decide between a pre-built SDK, a hosted checkout page, or a direct API integration. SDKs reduce your PCI scope and development time. Direct API calls give you maximum flexibility but require more careful security handling.

- Build in the test environment. Use your provider's sandbox to simulate successful charges, declines, network timeouts, and refunds. Test every edge case before touching live keys.

- Implement idempotency keys on every write operation. Any API call that creates a charge, issues a refund, or modifies a subscription must include a unique idempotency key. This prevents duplicate transactions when your server retries a timed-out request.

- Set up webhooks for real-time event handling. Do not rely on synchronous API responses alone. Webhooks deliver event notifications for asynchronous processes like settlement, dispute creation, and payout completion.

- Run a QA cycle with real cards in staging. Before going live, process small real transactions using your live API key in a controlled staging environment. Confirm that authorization, capture, and refund all behave as expected.

- Go live and monitor closely for 72 hours. The first three days in production reveal edge cases that testing missed. Watch your error logs, webhook delivery reports, and reconciliation reports in real time.

Pro Tip: Build a reconciliation job that runs nightly and compares your internal order database against the settled transactions report from your payment provider. A mismatch of even a few cents signals a logic error that compounds over time.

Common pitfalls to avoid

Transaction reconciliation errors are the most expensive mistake in API payment integration. They stem from treating authorization as payment. Track authorization, capture, and settlement as three separate states in your database. A second common pitfall is ignoring PCI DSS scope. Even with a tokenized integration, you must complete an annual Self-Assessment Questionnaire and maintain network security standards. Your payment provider handles card data security, but you are still responsible for your application's security posture.

Key takeaways

API payment integration works because it separates card data handling from your application logic, letting payment providers absorb compliance complexity while you control the customer experience.

| Point | Details |

|---|---|

| Authorization is not payment | Authorization reserves funds; settlement transfers them, typically 1–3 business days later. |

| Idempotency keys are required | Every write API call needs a unique key to prevent duplicate charges on network retries. |

| Provider pricing models differ widely | Offset pricing models like Paysec's can cut processing costs by 30–60% versus flat-rate providers. |

| Security scope shrinks with tokenization | Tokenized integrations remove raw card data from your systems, reducing PCI DSS obligations. |

| Webhooks outperform polling | Real-time event webhooks catch disputes, failures, and settlements faster than synchronous API checks. |

What the payment API space gets wrong about "simple" integration

The payment API industry markets integration as a weekend project. In practice, the technical setup is genuinely fast. What takes time is everything around it: reconciliation logic, webhook reliability, dispute handling workflows, and compliance documentation. I have seen businesses go live in 48 hours and spend the next three months fixing reconciliation gaps because no one built the nightly settlement matching job.

The other thing the industry undersells is pricing model complexity. Most developers and business owners accept flat-rate pricing because it is easy to understand. That simplicity costs real money at scale. A business processing $500,000 per month at 2.9% pays $14,500 in fees. The same volume under an interchange-plus or offset model can drop that number by $4,000 to $8,000 per month. Paysec's Network Offset Pricing is one of the clearest examples of a model built to give that money back to the merchant.

The future of payment APIs points toward embedded finance, where payment processing is one capability inside a broader financial stack that includes lending, insurance, and treasury management. Businesses that build clean, well-documented API integrations now will find it far easier to add those capabilities later. The architecture decisions you make today determine how much that expansion costs in 2027 and beyond. Pick a provider with a deep ecosystem, transparent pricing, and documentation that your team can actually use.

— Paysec Marketing Team

Ready to cut your processing costs with a better payment API?

Paysec gives merchants across 18+ industries a payment API built for real cost savings and full transparency. Its Network Offset Pricing passes wholesale interchange rates directly to you, with no hidden fees, no minimums, and no long-term contracts. Businesses in SaaS, eCommerce, healthcare, and restaurants have cut processing costs by 30–60% after switching. Paysec's detailed transaction reporting keeps your financials clean and audit-ready from day one. If you want a payment integration that works for your bottom line, explore Paysec merchant services to see how quickly you can get started.

FAQ

What is API payment integration in simple terms?

API payment integration connects your website or app to a payment provider's network so you can accept and process payments programmatically. It lets you trigger charges, issue refunds, and retrieve transaction data without leaving your platform.

How does API payment work during a transaction?

Your system sends a payment request to the provider's API, which routes it through the card network to the issuing bank for authorization. The bank returns an approval or decline in under 2 seconds, and funds settle to your account within 1–3 business days.

What is the difference between authorization and settlement in payment apis?

Authorization reserves the customer's funds but does not transfer them. The actual transfer happens during batch settlement, which typically runs overnight and completes within 1–3 business days after the authorization.

Why do payment apis use idempotency keys?

Idempotency keys prevent duplicate charges when a network timeout causes your server to retry an API request. Each unique key tells the payment provider to process the operation only once, regardless of how many times the request is sent.

What should i look for when choosing a payment API provider?

Evaluate pricing model, supported payment methods, developer documentation quality, and reporting depth. Providers like Paysec that offer offset pricing and transparent fee structures deliver measurable cost advantages over flat-rate competitors, especially at higher transaction volumes.