TL;DR:

- Marketplace payment processing manages multi-party funds flow, requiring specialized infrastructure beyond standard gateways. It involves escrow, split payments, and scheduled payouts, with the platform acting as a financial intermediary and risk bearer. Choosing appropriate models and providers is crucial for operational efficiency, compliance, and scaling success.

Marketplace payment processing is defined as the specialized multi-party payment infrastructure that collects, holds, splits, and disburses funds between buyers, sellers, and the platform operator within a single transaction. Unlike standard single-merchant payment processing, this system manages money flowing to multiple parties simultaneously, making it the financial backbone of platforms like Amazon, Etsy, Upwork, and Airbnb. Standard payment gateways cannot handle multi-party routing, escrow, or regulatory compliance at the scale marketplaces require. Providers like Stripe Connect and Zoho Payments have built dedicated marketplace payment solutions specifically to fill this gap.

What is marketplace payment processing and how does it differ from standard processing?

Marketplace payment processing is the technical and financial layer that manages money movement between three or more parties in a single transaction: the buyer, the seller, and the platform itself. Standard payment processing routes funds from one buyer to one merchant. Marketplace transaction processing routes those same funds through a holding layer, deducts a platform commission, and pays out the net amount to one or more sellers, often on a scheduled basis.

The distinction matters enormously for business owners. A restaurant using a standard payment processor receives the full transaction amount minus card network fees. A marketplace operator, by contrast, must collect funds centrally, calculate and retain a commission, and then distribute the remainder to the correct seller. That process requires purpose-built architecture, not a generic payment gateway.

Three structural elements separate marketplace payment systems from conventional ones. First, the platform acts as a financial intermediary, not just a technology layer. Second, split payments divide a single transaction automatically between marketplace commission and seller payouts, eliminating manual reconciliation. Third, payout scheduling controls when sellers receive their money, which can range from instant transfers to monthly disbursements depending on platform policy and risk management rules.

Understanding payment processing at the marketplace level also means recognizing the role of escrow. Funds are often held in a suspense or holding account between buyer payment and seller payout, creating a "collect, hold, disburse" cycle that protects both parties and gives the platform operational control.

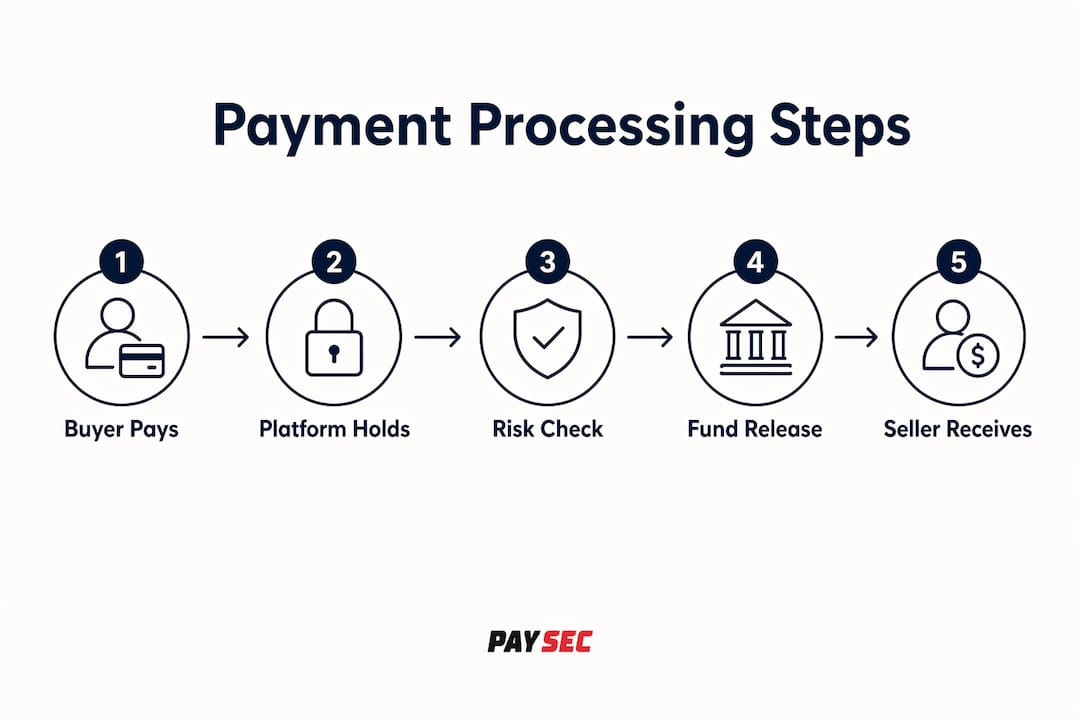

How marketplace payments work step by step

The payment flow in a marketplace follows a defined sequence, and each step carries distinct technical and financial implications.

-

Buyer initiates payment. The buyer selects a product or service and checks out using a preferred method: credit card, debit card, digital wallet, or bank transfer. The payment gateway tokenizes the card data and sends an authorization request to the card network.

-

Authorization and capture. The issuing bank approves or declines the transaction. Once authorized, the platform captures the funds, meaning the money moves from the buyer's account into the platform's holding account, not directly to the seller.

-

Funds enter escrow or a holding account. Marketplaces hold funds temporarily rather than instantly paying sellers. This holding period allows the platform to confirm delivery, run fraud checks, or wait for a dispute window to close. Platforms like Upwork hold contractor payments for a five-day security period before release.

-

Split payment calculation. The platform's payment logic calculates the commission percentage, deducts it from the gross transaction amount, and routes the net proceeds to the seller's sub-account. This split happens automatically through the payment processor's API.

-

Settlement and payout. The seller receives their funds according to the platform's payout schedule. Options include instant payouts, daily rolling settlements, weekly batch transfers, or monthly disbursements. Amazon Marketplace, for example, disburses seller funds every 14 days by default.

-

Reserve holds. High-risk sellers or new accounts may have a percentage of their earnings held in reserve for 30 to 90 days as a buffer against chargebacks and refunds.

Pro Tip: Set your payout schedule based on your seller base's cash flow needs. Frequent sellers on your platform will churn faster if payouts are delayed beyond two weeks. Daily or weekly schedules increase seller satisfaction without significantly raising your operational costs.

One counterintuitive fact: settlement delays create financial opportunity for platforms, not just friction. While funds sit in holding accounts, the platform earns float revenue on the pooled balance. This is a meaningful revenue line for large marketplaces processing millions of dollars daily.

What are the core challenges of marketplace payment processing?

Running payment infrastructure for a marketplace is operationally far more complex than running a single-merchant payment stack. The challenges fall into four categories.

-

Multi-party reconciliation. Every transaction generates at least three financial records: the gross buyer payment, the platform commission, and the seller net payout. When refunds, partial cancellations, or disputes occur, each record must be adjusted across all parties simultaneously. Without automated reconciliation tools, this process becomes a significant accounting burden.

-

Chargeback and dispute management. When a buyer disputes a charge, the platform must determine which party bears liability: the seller, the platform, or both. Platforms operating as the Merchant of Record absorb chargeback liability directly, which requires maintaining chargeback ratios below card network thresholds (typically 1% for Visa and Mastercard) to avoid penalties.

-

Compliance obligations. Marketplaces must comply with KYC (Know Your Customer), KYB (Know Your Business), AML (Anti-Money Laundering), PCI DSS, and regional regulations like PSD2 in Europe. Automated onboarding tools that verify seller identity during sign-up reduce compliance risk without slowing platform growth.

-

Liquidity and cash flow management. Settlement delays affect sellers' working capital. A freelancer waiting 14 days for payment may prefer a competing platform with faster payouts. Platforms that offer instant or next-day payouts gain a competitive advantage in seller acquisition.

-

Technology integration complexity. Managing escrow accounts, payment gateways, and API integrations across multiple payment methods and geographies requires significant engineering resources. Platforms that underinvest in payment infrastructure face higher error rates, failed payouts, and seller complaints.

Pro Tip: Integrate your payment processor's webhook system from day one. Real-time event notifications for payment captures, splits, and payouts let you build accurate financial dashboards without polling APIs manually, which reduces latency and reconciliation errors.

The compliance burden deserves special attention. KYC, AML, and PCI DSS requirements are not optional, and regulators treat marketplace operators as financial intermediaries in many jurisdictions. Platforms that treat compliance as an afterthought face fines, account suspensions, and reputational damage.

What are the common marketplace payment processing models?

The architecture of how a marketplace handles money depends on which entity is designated the Merchant of Record. This single decision affects liability, control, and user experience across the entire platform.

| Model | Who holds funds | Chargeback liability | Best for |

|---|---|---|---|

| Platform as Merchant of Record | Platform | Platform | Tightly controlled consumer marketplaces |

| Seller as Merchant of Record | Seller | Seller | B2B platforms with established vendors |

| Third-party holding account | Payment processor | Shared | Complex multi-seller or global marketplaces |

| Split transfer model | Platform then seller | Platform | Gig economy and service marketplaces |

Platform as Merchant of Record

In this model, the marketplace collects all buyer payments, holds the funds, and pays sellers as a disbursement. The platform bears full chargeback liability and is responsible for all tax reporting. Amazon operates this way for its first-party sales. The advantage is complete control over the buyer experience and payment data. The tradeoff is that the platform absorbs financial risk directly.

Seller as Merchant of Record

Here, each seller processes payments independently, and the platform charges an application or subscription fee rather than a transaction commission. This model reduces the platform's financial liability but creates an inconsistent buyer experience, since each seller may use different payment methods or checkout flows. It works best for B2B platforms where sellers are established businesses with their own payment infrastructure.

Split transfer and third-party holding models

These models use the payment processor as an intermediary. The processor collects funds, holds them in a pooled or individual escrow account, and executes the split according to predefined rules. Stripe Connect's "destination charges" and "separate charges and transfers" features are the most widely used implementations of this architecture. Automated split settlements minimize errors and accelerate payout processes, contributing to greater seller trust and satisfaction.

Choosing the right model is not purely a technical decision. It shapes your platform's legal exposure, your sellers' cash flow experience, and your ability to offer features like instant payouts or multi-currency support.

How marketplace payment solutions benefit platform operators

Purpose-built payment processing for marketplaces delivers measurable operational advantages that generic payment gateways cannot replicate.

-

Automated seller onboarding. Integrated KYC and payout setup within the platform's sign-up flow means sellers can start receiving payments within minutes of joining. This reduces onboarding friction and accelerates time-to-revenue for new marketplace participants.

-

Real-time commission splits. Automated split payments eliminate the need for manual commission calculations or end-of-month reconciliation. Every transaction triggers an immediate split, reducing accounting overhead and the risk of payment errors.

-

Multi-currency and global payout support. Platforms serving international sellers need to disburse funds in local currencies. Modern marketplace payment gateways support payouts in 40 or more currencies, removing a major barrier to global seller acquisition.

-

Escrow and dispute management. Built-in escrow protects buyers and sellers during disputes. When a buyer files a claim, the platform can freeze the relevant funds without affecting other transactions, giving both parties time to resolve the issue.

-

Detailed financial reporting. Integrated reporting tools give platform operators a real-time view of gross transaction volume, commission revenue, pending payouts, and reserve balances. This level of visibility is critical for financial planning and investor reporting.

-

Emerging payment rails. Stablecoin and blockchain-based payment rails now enable near-instant settlement and atomic commission splits, reducing traditional settlement delays from days to seconds. Platforms evaluating best marketplace payment systems in 2026 should assess whether their provider supports programmable money features, as this technology is moving from experimental to production-ready.

The cumulative effect of these capabilities is a payment operation that scales with the platform rather than against it. A marketplace processing 10,000 transactions per month faces the same reconciliation complexity as one processing 10 million, if the underlying infrastructure is automated correctly. You can explore how ecommerce payment stacks are structured to understand how marketplace payment layers fit within a broader technology architecture.

Key takeaways

Marketplace payment processing is the non-negotiable infrastructure layer that determines whether a multi-seller platform scales efficiently or collapses under operational complexity.

| Point | Details |

|---|---|

| Core definition | Marketplace payment processing collects, holds, splits, and disburses funds across multiple parties in one transaction. |

| Standard gateways fall short | Generic payment gateways cannot handle escrow, split payments, or multi-party compliance requirements. |

| Model selection drives risk | The Merchant of Record model determines who absorbs chargeback liability and controls the buyer experience. |

| Compliance is non-negotiable | KYC, AML, and PCI DSS obligations apply to marketplace operators as financial intermediaries in most jurisdictions. |

| Automation creates scale | Automated split settlements and real-time reconciliation eliminate manual overhead and accelerate seller payouts. |

The payment layer most marketplace builders underestimate

Most marketplace founders I speak with spend months perfecting their product catalog, seller onboarding UX, and search algorithms. They treat payment processing as a commodity decision, something to bolt on at the end. That is the single most expensive mistake a marketplace operator can make.

The payment layer is not infrastructure. It is the product. When a seller on your platform waits three weeks for a payout, they do not blame their bank. They blame your platform. When a buyer disputes a charge and the resolution takes two weeks, they leave a negative review of your marketplace, not of the payment processor. Every friction point in the money flow becomes your brand problem.

What I have seen work consistently is treating the payment architecture decision with the same rigor as the core product architecture decision. That means evaluating providers not just on transaction fees but on payout speed, split payment flexibility, compliance tooling, and API documentation quality. Stripe Connect is the most widely adopted solution for a reason: its documentation is exceptional and its split transfer models cover most use cases. But it is not the only option, and for platforms with specific vertical needs, specialized providers often deliver better economics.

The emerging technology angle is worth watching closely. Programmable escrow and stablecoin rails are not science fiction in 2026. Several B2B marketplace platforms have already moved portions of their settlement infrastructure to blockchain-based rails to achieve same-day payouts without the cost of traditional wire transfers. This is not a reason to rebuild your stack today. It is a reason to choose a payment provider that is actively investing in these capabilities.

My recommendation for business owners evaluating marketplace payment providers: prioritize providers that offer transparent processing fee structures, automated compliance tooling, and flexible payout scheduling. The provider that costs slightly more per transaction but eliminates 20 hours of monthly reconciliation work is almost always the better economic choice.

— PaySec Marketing Team

How Paysec simplifies marketplace payment operations

Marketplace operators managing split payments, seller compliance, and multi-party reconciliation need a payment partner that removes cost and complexity simultaneously. Paysec's Network Offset Pricing delivers exactly that, with processing cost reductions of 30 to 60% compared to standard merchant accounts. There are no hidden fees, no minimums, and no long-term contracts.

Paysec supports marketplace operators across 18 or more industries with detailed transaction reporting, built-in compliance tools, and dedicated merchant accounts structured for multi-party payment flows. Whether you are running an eCommerce marketplace, a SaaS platform, or a service marketplace, Paysec gives you the financial transparency and payment flexibility your sellers and buyers expect. Explore what Paysec can do for your platform at paysec.ai.

FAQ

What is marketplace payment processing in simple terms?

Marketplace payment processing is the system that collects money from buyers, holds it centrally, deducts the platform's commission, and pays out the remainder to sellers. It replaces manual money management with automated, multi-party transaction routing.

How does marketplace payment processing differ from standard payment processing?

Standard payment processing routes funds from one buyer to one merchant. Marketplace payment processing routes funds through a holding account, splits them between the platform and one or more sellers, and disburses payouts on a schedule. Standard gateways cannot handle this multi-party flow.

What is the Merchant of Record in a marketplace?

The Merchant of Record is the entity legally responsible for the transaction, including chargeback liability and tax reporting. In most consumer marketplaces, the platform itself is the Merchant of Record, which gives it control over the buyer experience but also full financial liability.

Why do marketplaces hold seller funds before paying out?

Marketplaces hold funds temporarily to manage fraud risk, confirm delivery, and maintain a buffer against chargebacks and refunds. This holding period is standard practice and protects both the platform and the buyer.

What compliance requirements apply to marketplace payment processing?

Marketplace operators must meet KYC, KYB, AML, PCI DSS, and regional regulations like PSD2. These requirements apply because platforms act as financial intermediaries, and regulators treat them accordingly regardless of platform size.