Managing payment processing while trying to cut transaction costs and avoid account holds is a constant challenge for merchants with mixed or high risk sales. Most processors either require strict minimum transaction volumes, obscure true fee structures, or pass onboarding to third parties which increases setup friction and makes direct cost comparisons nearly impossible. This overview lays out contract terms, pricing transparency, and industry fit across three payment processing platforms so merchants can select one that matches their volume, risk profile, and reporting needs.

Table of Contents

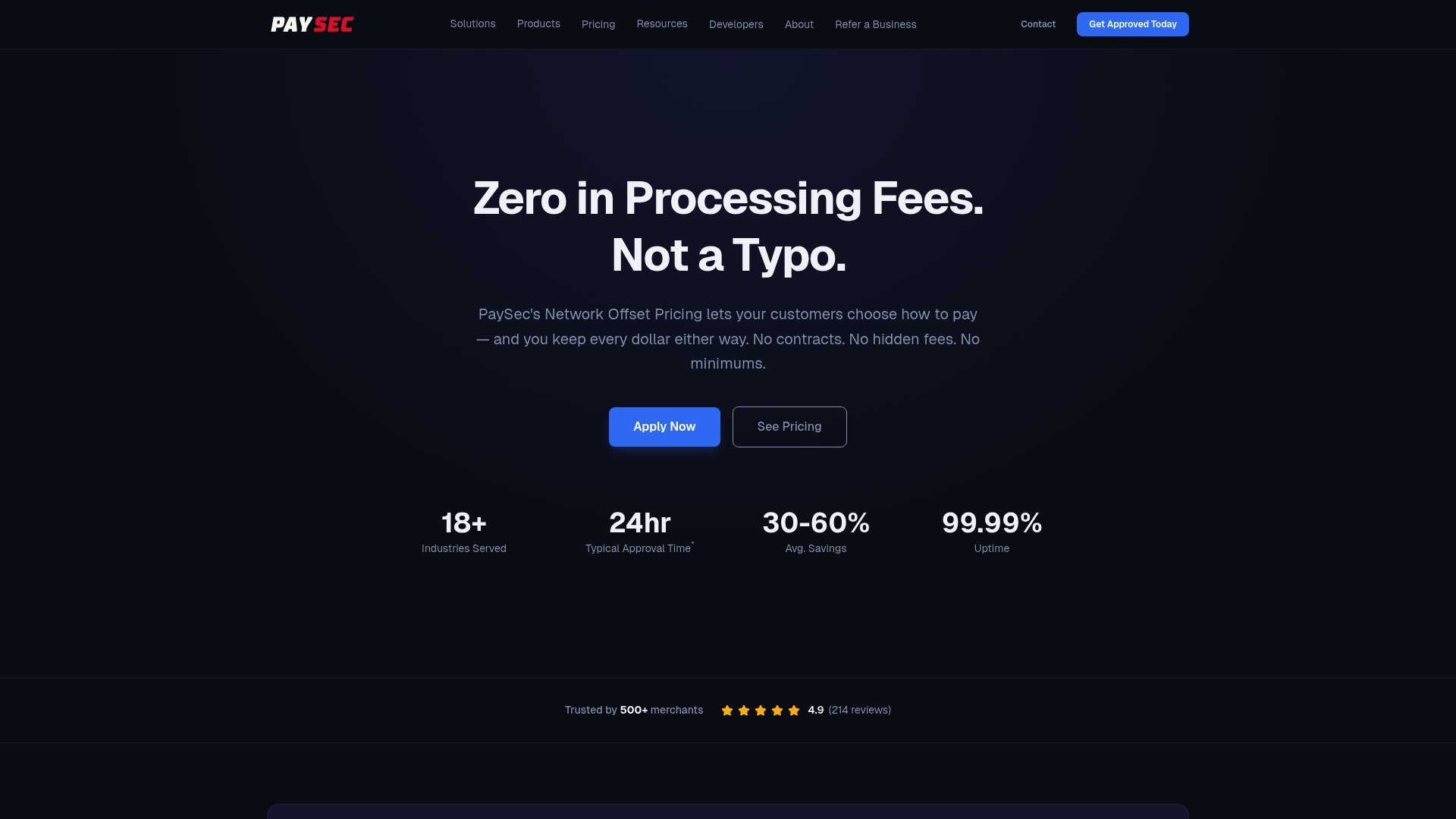

PaySec

At a Glance

Network Offset Pricing that passes wholesale interchange with a fixed margin — the vendor advertises typical savings of 30–60% versus flat-rate processors. PaySec pairs that pricing model with month-to-month contracts and dedicated merchant support, positioning cost transparency as the core offer.

Core Features

-

Network Offset Pricing with transparent fee disclosures and interchange analysis tools for line-by-line transaction visibility.

-

Multi-channel payment acceptance: in-store terminals, online gateways, and mobile acceptance with RESTful APIs and SDKs.

-

According to the vendor, PaySec meets PCI DSS Level 1, SOC 2, and P2PE encryption standards to protect cardholder data.

-

Real-time reporting and interchange analysis dashboards for daily reconciliation and performance checks.

Key Differentiator

PaySec’s one true differentiator is that pricing method: passing wholesale interchange rates with a fixed margin. That architecture shifts processing cost from opaque bundled fees to predictable margin math, which the vendor says drives the savings range noted above.

Pros

-

The vendor states approvals often happen within 48 hours, which helps merchants in high-risk verticals get live faster than many legacy processors.

-

Transparent pricing removes surprise markup by showing interchange and the fixed margin on each transaction, simplifying dispute or reconciliation conversations.

-

Dedicated account managers provide direct access to staff who understand underwriting for healthcare, CBD, and other complex verticals.

-

Wide vertical support: retail, eCommerce, restaurants, and high-risk categories are explicitly supported, reducing the chance of sudden account holds.

-

Strong compliance posture and reporting give finance teams the transaction-level detail they need for audits and cost analysis.

Cons

- Onboarding can take 1-2 days if there is a mismatch in business and principal information.

Who It’s For

Merchants that prioritize fee transparency and predictable processing economics, especially small and mid-size businesses in healthcare, retail, eCommerce, or high-risk categories. Finance teams that run interchange analysis will find the reporting useful.

Unique Value Proposition

Passing wholesale interchange with a fixed margin turns variable processing fees into a predictable cost line that finance teams can model. For merchants who run tight margin scenarios or who bill customers for card costs, that predictability can reduce reconciliation work and improve gross margin forecasts.

Real World Use Case

A healthcare practice moves patient billing to PaySec to reduce per-transaction markup and gain transaction-level reporting for insurance reconciliation. The vendor’s underwriting and PCI claims helped the practice migrate without long contract commitments.

Pricing

Pricing is bespoke and requires a consultation; the vendor advertises no-hidden-fee disclosures and month-to-month contracts rather than fixed long-term agreements. Expect a merchant-specific quote based on volume, average ticket, and vertical risk.

Website: https://paysec.ai

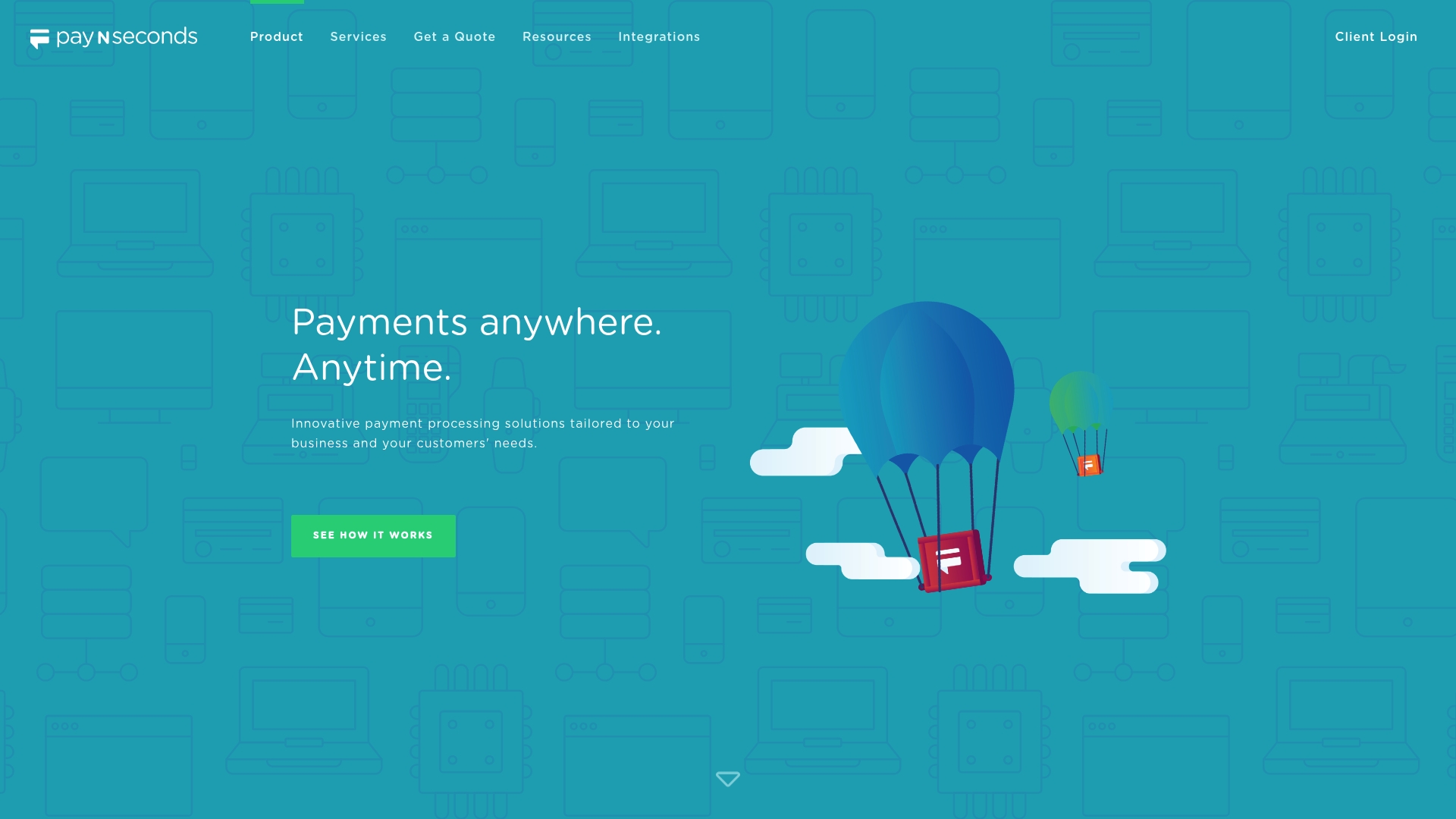

Pay N Seconds

At a Glance

Requires a minimum of 100 transactions per month and at least three years of financial history before Pay N Seconds will engage. That eligibility threshold makes this provider a practical option for established merchants rather than casual or very small sellers.

Core Features

-

Unified payment gateway that handles online, text, POS, telephone, and IVR payments from one dashboard.

-

Flexible pricing models that let you choose pass through, shared, or absorbent fee structures for specific channels.

-

Automation features including IVR billing, recurring billing, and electronic invoicing to cut manual reconciliation steps.

-

Real time access to payment data and consumer analytics for reporting and dispute handling.

-

Integrates easily with existing software or runs as a standalone processor.

Key Differentiator

Pay N Seconds centralizes every channel under a single login while letting merchants choose how processing costs are allocated. That mix of central control plus customizable pricing fits mid market operations that need both programmatic automation and direct fee management rather than tokenized low volume storefronts.

Pros

-

Manages phone, IVR, in store, and web payments from one interface which reduces context switching for billing teams.

-

Pricing flexibility lets businesses pass fees to customers or absorb costs selectively for promotions or specific payment methods.

-

Automation for recurring billing and electronic invoicing reduces manual posting and shortens collections cycles.

-

Security measures include PCI DSS compliance and SSL encryption which supports regulatory requirements for card handling.

-

A dedicated support team is available to assist with onboarding and troubleshooting for complex integrations.

Cons

-

No independent third party reviews are publicly available to verify day to day merchant experience.

-

The vendor discloses limited public detail on per transaction fees which makes direct cost comparisons difficult without a quote.

-

The 100 transaction minimum excludes very small merchants and many early stage startups from consideration.

When It May Not Fit

If you process fewer than 100 transactions per month this product will likely be a mismatch. If you require transparent, published fee schedules for quick vendor comparison, Pay N Seconds requires you to request a quote which slows procurement. Not ideal for single location micro merchants.

Notable Integrations

-

PDC Flow

-

Windebt

-

Lariat Software

-

Interprose

-

Aktos

-

Collect Software (Comtech)

-

Genesys

-

Collect One

Who It’s For

Medium to large merchants that need multi channel payment handling and have predictable transaction volumes. Teams that run telephone billing, in person sales, and recurring subscriptions under one finance team will get the most value. Not aimed at low volume or brand new businesses.

Real World Use Case

A regional service provider routes online card payments, IVR collections, and in store purchases through Pay N Seconds. Automation takes recurring billing off spreadsheets, real time reporting surfaces failed payments, and the finance team reduces manual reconciliation work across three sales channels.

Pricing

Pricing is quote based. The vendor asks prospects to request a quote and offers flexible fee models that can be set to pass fees to customers, split costs, or absorb them in house. Public per transaction rates are not listed.

Website: https://paynseconds.com

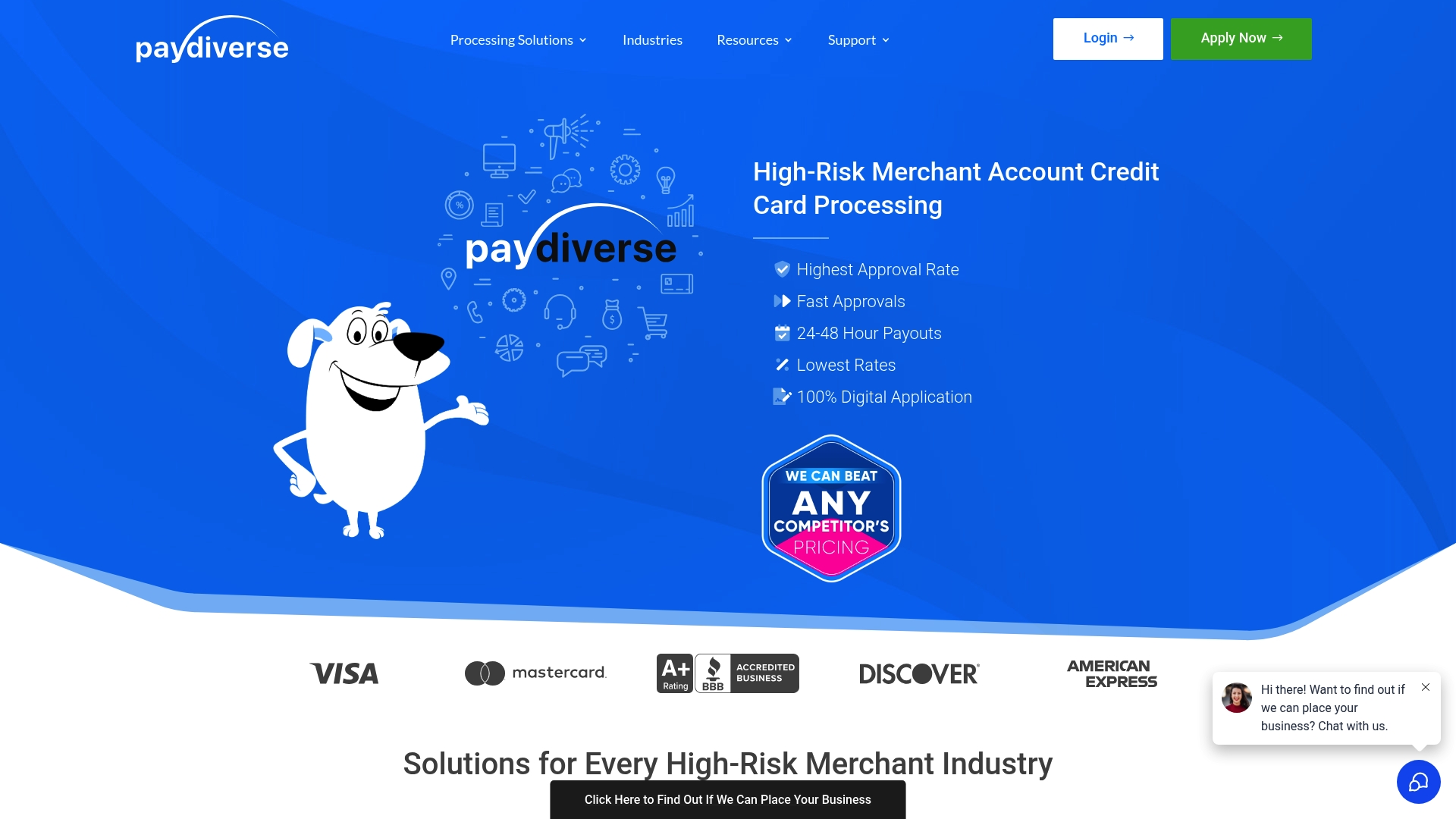

PayDiverse

At a Glance

According to the company, PayDiverse reports over 20 years of experience and claims the largest network of banks willing to underwrite high risk merchants. The brokerage emphasizes fast digital onboarding and multiple bank options for industries like CBD and nutraceuticals.

Core Features

PayDiverse acts as a merchant account broker focused on underwriting, gateway setup, and chargeback workflows.

-

Digital application process for merchant accounts that shortens paperwork and speeds underwriting.

-

Multiple bank relationships so accounts can be placed across processors to reduce single point failure risk.

-

Chargeback alerts and fraud prevention tools plus options for offshore processing and pinless debit support.

Key Differentiator

The vendor presents that broad banking network as its defining strength. Rather than routing every merchant to a single processor, PayDiverse positions clients across several acquiring partners to keep accounts active when one bank tightens rules. For merchants in higher risk verticals this network claim is the core selling point and frames how the brokerage manages declines and reserves.

Pros

-

Specialization in high risk merchant accounts reduces time spent educating underwriters compared with generalist brokers.

-

Fast approvals and digital onboarding shorten the path from application to processing for businesses that need quick access to payment rails.

-

Robust risk tools improve visibility on disputes and fraud with actionable alerts that protect revenue.

-

Supports a broad slate of verticals including CBD, nutraceuticals, coaching, and ecommerce which simplifies vendor selection for niche teams.

-

24/7 support availability positions the brokerage to handle time sensitive underwriting or chargeback escalations across time zones.

Cons

-

Public feedback is sparse which makes reputation assessment hard for new prospects evaluating long term reliability.

-

Some user reports flag inconsistent or brusque sales interactions which can complicate onboarding conversations.

-

As a broker, PayDiverse often places implementation with partner processors and offshore rails which adds coordination steps for internal finance teams.

When It May Not Fit

If your business is low risk and eligible for mainstream merchant rates, a direct relationship with a primary processor will likely be cheaper and simpler. If you require a single vendor to own every integration and all implementation work, a brokerage model that uses multiple acquiring partners may introduce extra handoffs you do not want.

Who It’s For

High risk merchants that need underwritten merchant accounts quickly. Best fit for CBD brands, nutraceutical sellers, adult content merchants, and coaching businesses that value diversified bank placement and active dispute monitoring.

Real World Use Case

A US CBD distributor uses PayDiverse’s online application to secure access to several acquiring banks. The broker places the account on a combination of domestic and offshore rails, integrates a gateway for ecommerce, and routes chargeback alerts to the merchant and their payment manager for immediate follow up.

Pricing

Not applicable — informational only. PayDiverse provides custom pricing and placement based on industry, risk profile, and bank terms rather than publishing standard rate cards.

Website: https://paydiverse.com

**Competitor eligibility:** - Excluded products (discontinued / inaccessible / under construction): none - Usable competitors remaining: Pay N Seconds, PayDiverse

Intro pre-write:

-

Does paysec.ai clearly outpace every usable competitor on a single dimension? YES

-

If YES: dimension where paysec.ai wins — Transparent pricing framework with interchange analysis

-

First sentence draft: Choosing the right payment processing provider can significantly impact a business’s operational efficiency and financial forecasting.

Competitor win pre-write:

-

Which competitor wins which dimension: PayDiverse wins high-risk merchant support because of their underwriting network and placement options

-

Does this dimension matter to the primary reader? YES

Best Fit uniqueness check:

-

List each bullet scenario in one clause: Businesses seeking detailed transparent pricing for predictable financial modeling / Companies needing diverse and flexible transaction channel support / Organizations in high-risk verticals requiring proficient underwriting services

-

Can any two be swapped without changing meaning? NO

Our Pick pre-write:

-

The ONE capability unique to paysec.ai in this set: Transparent pricing structure via Network Offset Pricing

-

Evidence from the reviews: “Transparent pricing removes surprise markup by showing interchange and the fixed margin on each transaction.”

-

Closing sentence draft: PaySec is particularly suited for businesses that value assured visibility into transaction processing and seek month-to-month contracts free of long-term commitments.

-

Substitution test: If replaced with PayDiverse or Pay N Seconds, it does not align with their key offerings such as high-risk underwriting networks or channel-specific flexibility.

-

Does the substituted version still work as a recommendation? NO

Comparative Analysis

Selecting an payment processing solution is a consequential decision for businesses, as it shapes cost structures and customer interactions while ensuring compliance and efficiency.

Pricing Transparency and Cost Control

PaySec sets itself apart with its Network Offset Pricing model, ensuring merchants gain precise insights into transaction costs by detailing wholesale interchange rates and associated margins. This approach is advantageous for companies requiring predictability in financial transactions. In contrast, while Pay N Seconds and PayDiverse also provide customized pricing, they do not emphasize transparency to the same extent, often requiring merchants to request direct quotes for details.

High-Risk Merchant Accommodation

When it comes to facilitating high-risk merchants, PayDiverse excels due to its extensive network of banking relationships that supports diverse underwriting requirements. Unlike competitors, this positioning allows for customized solutions to challenging circumstances, such as CBD or nutraceutical businesses requiring swift onboarding. This focus complements PaySec, which also serves high-risk verticals but using a direct approach rather than brokerage services.

Best Fit Recommendations

-

PaySec is ideal for businesses that prioritize transparent pricing structures and interchange analysis tools to model predictable cost dynamics.

-

Pay N Seconds suits medium to large firms requiring centralized management for multi-channel payment options, complemented by automation in recurring billing

-

PayDiverse is for businesses operating in high-risk sectors that depend on placement across multiple banking networks, ensuring operational resilience.

Our Pick

PaySec emerges as the choice for companies needing full visibility over transaction fees and cost structuring. Its Network Offset Pricing model provides clarity. However, organizations specifically requiring broad high-risk underwriting or extensively centralized multi-channel payment functions might find better alignment with PayDiverse or Pay N Seconds, respectively.

Payment Processing Software Comparison

Evaluate which solution best meets your payment processing needs based on distinctive features, pricing, and support for various business types.

| Product | Core Feature | Key Differentiator | Best For | Pricing | Notable Limitation |

|---|---|---|---|---|---|

| PaySec | Network Offset Pricing with transparency | Fixed margin pricing for cost predictability | SMBs in diverse verticals | Transparent and Tailored for merchants | Onboarding can take 102 days |

| Pay N Seconds | Unified payment gateway for omni-channel use | Single login for customizable processing costs | Medium to large merchants | Not disclosed | Minimum 100 monthly transactions |

| PayDiverse | Brokerage with diversified bank placements | Broad network of supporting acquiring banks | High-risk vertical merchants | Informational | Reliability depends on third-party partners |

Discover Transparent Savings with PaySec as a Top Alternative to Graziepayments.com

If you are seeking a Graziepayments.com alternative that truly addresses the pain point of high and unclear transaction fees PaySec offers a fresh approach called Network Offset Pricing. This pricing model passes on wholesale interchange fees with a fixed margin creating savings of 30–60% while providing detailed transaction reports for full financial visibility. PaySec eliminates long-term contracts and hidden fees which means your business gains control over processing costs without surprises.

Experience the difference for SaaS, healthcare, eCommerce, CBD retail and more. See exactly what you pay at the transaction level with dedicated support from specialists who understand complex verticals. Don’t let confusing pricing drain your margin. Visit PaySec now to review how their transparent pricing model can cut costs and increase your revenue retention. Book a consultation today and start reducing your transaction costs while accessing powerful interchange analysis dashboards.

Frequently Asked Questions

How does Paysec ensure cost transparency for merchants?

Paysec offers Network Offset Pricing, which provides a predictable cost model by passing wholesale interchange rates with a fixed margin. This allows merchants to see line-by-line transaction visibility, simplifying disputes or reconciliation discussions. You can expect clearer insights into your payment processing costs as a result.

What is the difference between Paysec and Pay N Seconds in terms of pricing transparency?

Pay N Seconds provides flexible pricing models, including options to pass fees onto customers and various channel fee structures, which can be advantageous for medium to large merchants with established payment practices. In contrast, Paysec’s transparent pricing shows both interchange and fixed margins, which is tailored for small and mid-size businesses seeking straightforward cost structures. If transparent pricing is essential for your financial planning, Paysec is the better fit for your needs.

Which platform offers better support for high-risk categories, Paysec or PayDiverse?

PayDiverse specializes in high-risk merchant accounts and claims access to the largest network of banks underwriters willing to work with such merchants. Although Paysec also supports high-risk verticals and offers dedicated account managers, PayDiverse’s focus on this area makes it particularly strong for those specific cases. Depending on your industry focus, you may find that PayDiverse better meets your high-risk processing needs.

Can I easily access real-time reporting with Paysec?

Yes, Paysec provides real-time reporting and interchange analysis dashboards that facilitate daily reconciliations and performance checks. This feature is critical for finance teams looking for detailed transaction-level information for audits and cost analysis. This capability can significantly streamline your payment processing oversight.

How do the onboarding processes differ between Paysec and Pay N Seconds?

Paysec typically allows approvals within 48 hours, which can expedite the onboarding process for new merchants. However, Pay N Seconds is known for requiring a minimum of 100 transactions monthly and three years of financial history before engaging, which could complicate onboarding for newer merchants. If fast onboarding is a priority for you, Paysec may be the better choice.