TL;DR:

- Contactless payment processing uses NFC technology for fast, secure transactions with encrypted tokens and cryptograms. Certification and proper hardware are essential to ensure security, efficiency, and compliance. Implementing contactless payments enhances customer experience, reduces fraud, and lowers operational costs for businesses.

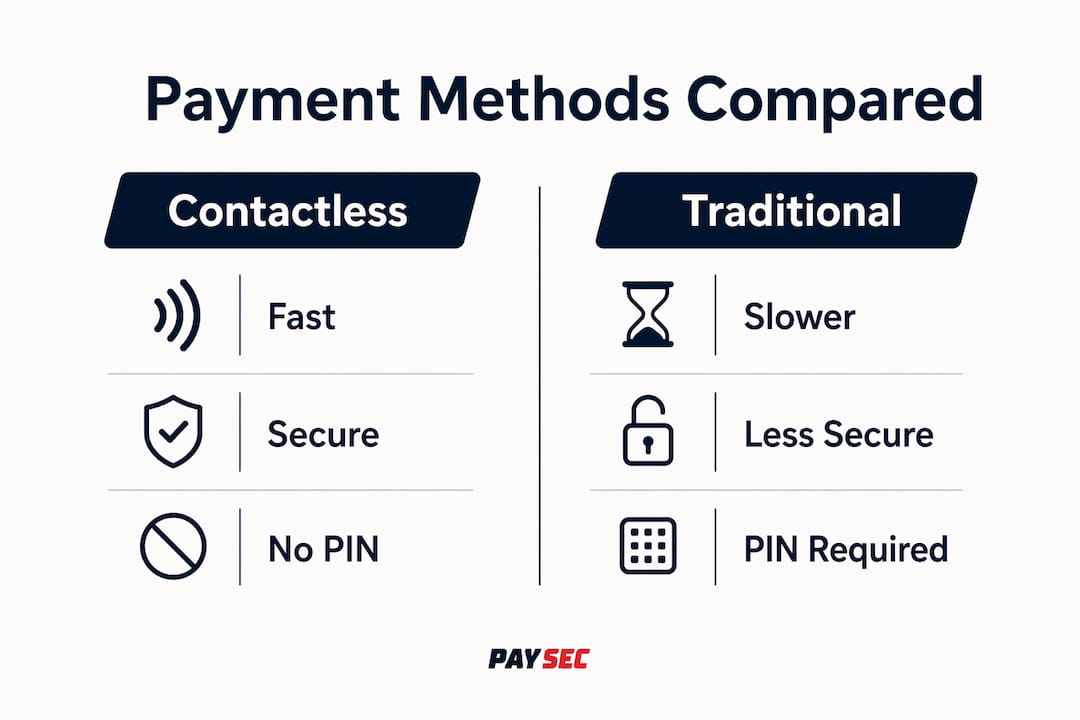

Contactless payment processing is defined as a transaction method where a customer taps an NFC-enabled card, smartphone, or wearable device near a compatible point-of-sale terminal to authorize payment without swiping, inserting, or entering a PIN. Apple Pay, Google Pay, Samsung Pay, Visa, and Mastercard all operate within this framework, making it one of the most widely supported payment technologies available to merchants today. For business owners and finance managers, understanding this technology is no longer optional. Customer demand for fast, frictionless checkout is growing, and the businesses that meet it gain a measurable edge in both transaction speed and customer satisfaction.

What is contactless payment processing and how does it work?

Contactless payment processing relies on Near Field Communication, or NFC, as its core technology. NFC is a short-range radio communication standard that exchanges encrypted credentials between a card or device and a POS terminal at a distance of roughly 2 inches. That short range is not a limitation. It is a deliberate security feature that makes remote interception nearly impossible.

When a customer taps their card or phone near the terminal, the exchange happens in under a second. The terminal reads the device, sends the transaction data to the payment network, and the card issuer authorizes the payment. The customer never hands over their card, and no physical contact is required at any point.

The process that protects this exchange is called tokenization. Tokenization replaces the card number with a device-specific token, so the merchant never sees the customer's actual primary account number. Mastercard describes this token as a stand-in number paired with a unique per-transaction cryptogram. Even if someone intercepted the data, the token would be useless outside that specific transaction.

Encryption adds another layer. Each tap generates dynamic data, meaning the authentication code changes with every transaction. This is a significant upgrade over magnetic stripe cards, which transmit the same static data every time. Mastercard, Adyen, and Square all emphasize unique encrypted codes as the foundation of tap-to-pay security.

How terminals get certified for contactless

Not every terminal can accept contactless payments out of the box. Terminals must carry certified contactless kernel software, which governs how the device handles each transaction. EMVCo guidelines require terminals to support specific contactless kernel functions that determine when a PIN is required, when it can be skipped, and when the transaction needs online authorization based on the amount and issuer rules. When you shop for a new terminal, EMVCo certification is a non-negotiable requirement.

Pro Tip: Ask your payment processor for the terminal's EMVCo certification documentation before purchasing. A certified terminal protects you from compliance gaps and failed transactions at the point of sale.

What are the benefits of contactless payments for businesses?

The advantages of contactless payment processing go well beyond customer convenience. They affect your operations, your fraud exposure, and your bottom line.

-

Faster checkout times. Tap-to-pay authorizes transactions almost instantly by eliminating card insertion and PIN entry. In high-volume environments like restaurants, retail stores, and healthcare front desks, shaving seconds off each transaction adds up to significantly shorter lines and higher throughput per hour.

-

Lower fraud risk. Because each transaction generates a unique encrypted code, stolen data from one transaction cannot be reused. Contactless payments reduce fraud risk by avoiding the transmission of static card data entirely. This protects merchants from chargebacks tied to card-present fraud.

-

Reduced cash handling. Every dollar handled in cash carries labor costs: counting, reconciling, transporting, and depositing. Shifting customers toward tap payments reduces that overhead directly. For businesses in sectors like food service or CBD retail, this operational gain compounds quickly.

-

Meeting customer expectations. Customers who use Apple Pay or Google Pay daily expect to use them everywhere. Businesses that cannot accept tap payments lose sales to competitors who can. This is not a future trend. It is the current baseline expectation in most urban and suburban markets.

-

Lower hardware costs through Tap on Phone. Tap on Phone technology allows merchants to accept contactless payments directly through a smartphone, without dedicated hardware. Active in 115+ markets, this option is built for small and micro-merchants who previously relied on cash or basic card readers.

On the cost side, consumers generally pay no additional fees for contactless transactions. Merchants pay processing fees comparable to other card transactions, so the cost structure is familiar. The key is reviewing your processor's terms to confirm the exact rate structure for tap transactions versus chip or swipe.

Contactless vs. traditional and mobile payment methods

Understanding the differences between payment types helps you make the right infrastructure decisions. The table below compares the most common methods across the factors that matter most to business operators.

| Payment Method | Authorization Speed | Security Level | Hardware Required | PIN Required |

|---|---|---|---|---|

| Magnetic stripe swipe | Moderate | Low (static data) | Card reader | Sometimes |

| Chip insert (EMV) | Slow | High (dynamic data) | Chip-capable terminal | Often |

| Contactless card tap | Very fast | High (token + cryptogram) | NFC-enabled terminal | Rarely |

| Mobile wallet (Apple Pay, Google Pay) | Very fast | Very high (biometric + token) | NFC-enabled terminal | No |

| Wearable (Samsung Pay, smartwatch) | Very fast | High (token + cryptogram) | NFC-enabled terminal | No |

The magnetic stripe is the weakest link in this group. It transmits the same card data on every swipe, making it the easiest target for skimming attacks. Chip insert cards improved on that with dynamic data, but the dip-and-wait process slows checkout noticeably.

Contactless cards and mobile wallets both use tokenization and dynamic cryptograms, putting them at the same security tier. Mobile wallets add biometric authentication, such as Face ID or a fingerprint, which makes them the strongest option for consumer-side protection. For merchants, the terminal requirement is identical: an NFC-enabled, EMVCo-certified reader handles all three contactless types.

Understanding transaction limits and fallback rules

Most contactless transactions below a set threshold, which varies by country and issuer, process without a PIN. Above that threshold, the terminal's certified kernel software triggers a PIN request or routes the transaction for online authorization. This is not a flaw in the system. It is a deliberate risk management rule built into the EMVCo terminal certification framework. Finance managers should confirm their processor's threshold settings to avoid unexpected friction at checkout for higher-value transactions.

One practical note: if a contactless transaction fails, most terminals fall back to chip insert automatically. This fallback is required under EMVCo guidelines, so customers are never left stranded at the register.

How to implement contactless payment processing in your business

Getting contactless payments live in your business is a straightforward process when you approach it in the right order. Here is what to prioritize.

-

Audit your current terminals. Check whether your existing POS hardware carries NFC capability and EMVCo contactless certification. Many terminals manufactured after 2018 include NFC hardware but may need a software update to activate it. Contact your current processor to confirm.

-

Select a compatible payment processor. Your processor must support contactless authorization through the card networks. Look for processors that offer transparent fee structures for tap transactions. Paysec's Network Offset Pricing is one model worth examining, as it gives merchants wholesale interchange rates with no hidden fees and no long-term contracts.

-

Upgrade or replace terminals as needed. If your hardware is not NFC-capable, invest in contactless-capable terminals that handle countertop, wireless, and mobile use cases. For field-based or mobile businesses, Tap on Phone solutions eliminate the need for dedicated hardware entirely.

-

Integrate with your reporting and reconciliation workflow. Contactless transactions generate the same authorization data as chip transactions, but your back-office systems need to be configured to capture and categorize them correctly. Finance teams should note that tokenization prevents sharing the PAN, so reconciliation processes must rely on token-based transaction records rather than raw card numbers. Design your workflow to avoid handling sensitive cardholder data unnecessarily.

-

Train your staff. Checkout staff should know how to prompt customers for tap payment, handle fallback scenarios, and recognize when a transaction has been authorized versus declined. A 15-minute training session covers the essentials.

-

Communicate the option to customers. Place the contactless symbol near your terminal and on your checkout signage. Customers who use Apple Pay or Google Pay regularly will look for that symbol before they even reach the counter.

Pro Tip: If you operate across multiple locations, standardize your terminal model and processor configuration across all sites. Inconsistent hardware creates inconsistent customer experiences and complicates centralized reporting.

For businesses in sectors with elevated compliance requirements, such as healthcare or CBD retail, reviewing payment processing best practices specific to your industry before deployment is worth the time. Compliance requirements vary, and your processor should be able to walk you through the relevant rules.

Key takeaways

Contactless payment processing is the most secure and operationally efficient card-present transaction method available to businesses in 2026, and adoption is now a baseline customer expectation rather than a competitive differentiator.

| Point | Details |

|---|---|

| NFC and tokenization are the core | Every tap payment uses short-range radio and a unique token to protect card data. |

| Terminals require EMVCo certification | Only certified hardware handles PIN thresholds and fallback rules correctly. |

| Mobile wallets add biometric security | Apple Pay and Google Pay layer biometric authentication on top of tokenization. |

| Tap on Phone lowers the entry barrier | Merchants can accept contactless payments via smartphone in 115+ markets. |

| Processor fee structures vary | Review your processor's terms to confirm tap transaction rates match your cost expectations. |

The contactless shift is permanent. here is what that means for your strategy.

By PaySec Marketing Team

Working with merchants across 18+ industries gives you a clear view of where payment friction actually lives. The businesses that treat contactless as a checkbox, buy a terminal, and move on, tend to miss the larger opportunity.

The real value of contactless payment technology is not just speed at the register. It is what that speed does to your entire operation. Shorter lines mean higher table turns in restaurants. Faster checkout means fewer abandoned carts in retail. Reduced cash handling means fewer reconciliation errors and lower labor costs at close. These are not marginal gains. They compound.

What we see most often is that businesses underestimate how quickly customer expectations shift. Two years ago, a customer who could not tap to pay would shrug and insert their chip card. Today, that same customer notices the missing option and remembers it. Brand perception is built in small moments, and the checkout experience is one of the most repeated moments in any customer relationship.

The other thing worth saying plainly: the security argument for contactless is not theoretical. Tokenization means your business never touches a real card number. That single fact reduces your PCI DSS scope, lowers your fraud exposure, and simplifies your compliance posture. Finance managers who have dealt with a data breach or a chargeback dispute understand exactly how much that is worth.

The businesses winning on payments right now are not the ones with the most complex systems. They are the ones with the clearest, most transparent fee structures and the most frictionless checkout experience. Those two things are achievable for any merchant willing to ask the right questions of their processor.

— PaySec Marketing Team

See how Paysec supports contactless payment adoption

Paysec gives merchants a direct path to contactless payment processing without the fee complexity that typically comes with it.

Through Network Offset Pricing, Paysec passes wholesale interchange rates directly to merchants, eliminating hidden fees, minimums, and long-term contracts. Clients across SaaS, restaurants, eCommerce, healthcare, and CBD retail have documented savings of 30–60% on processing costs. Paysec's merchant services include detailed transaction reporting that makes reconciliation straightforward, whether you are running NFC terminals at a single location or managing payments across multiple sites. If you are ready to upgrade your payment infrastructure, Paysec makes the process direct and transparent from day one.

FAQ

What is contactless payment processing in simple terms?

Contactless payment processing lets customers pay by tapping an NFC-enabled card, phone, or wearable near a POS terminal. The transaction authorizes in seconds without swiping, inserting, or entering a PIN.

How does contactless payment work technically?

The card or device transmits an encrypted token and a unique per-transaction cryptogram to the terminal via NFC. The terminal forwards this data to the card network, and the issuer authorizes the payment within seconds.

Is contactless payment safe for businesses?

Yes. Contactless payments generate a unique encrypted code for every transaction, so stolen data cannot be reused. Tokenization also means merchants never receive the customer's actual card number, which reduces PCI DSS scope.

What types of contactless payments can my business accept?

Businesses with an NFC-enabled, EMVCo-certified terminal can accept contactless cards, mobile wallets like Apple Pay and Google Pay, and wearables like Samsung Pay-enabled smartwatches, all through the same hardware.

Do contactless payments cost more than chip or swipe transactions?

Consumers pay no additional fees for tap transactions. Merchant processing fees for contactless payments are generally comparable to other card transaction types, though the exact rate depends on your processor agreement.